Welcome to Episode 84 of Special Situation Investing.

Two weeks ago, we wrote a piece titled A Tale of Two Pipelines. In it, we argued Canadian oil producers are poised to benefit from an expansion of the only oil pipeline to reach the West Coast of North America—the Trans Mountain Pipeline.

The expansion project is set to be operational in Q1 of 2024 and will benefit oil producers in three ways:

Increased export capacity could increase the price of Canadian heavy crude by reducing the Western Canadian Select (WCS) discount to other oil benchmarks.

More pipeline infrastructure will allow Canadian producers to sell more oil because current pipelines operated at or near full capacity.

Greater competition among pipelines is already decreasing toll costs to producers.

We recommend you read, or reread, A Tale of Two Pipelines to get the full details behind these points and better understand the background of today’s piece.

While arguing the increased capacity of the Trans Mountain Pipeline will be a tailwind for Canadian oil producers, we threw a curve ball hinting our preferred way to play the evolving situation isn’t an oil producer at all but instead an oil and gas royalty company.

That company is PrairieSky Royalty Ltd (TSX: PSK, OTC: PREKF).

The company’s history

PrairieSky traces its origin to 1881 when in exchange for building a railroad East to West across the country, the Canadian Pacific Railway company (CPR) was granted 25 million acres of land by the Canadian government. CPR was allowed to select land from the odd numbered one-mile squares of a checker board pattern out twenty-four miles on either side of its railroad. These grants included the ownership of the water, oil and gas mineral rights.

When CPR began drilling for water in 1883, it discovered natural gas and it quickly focused on drilling for both natural gas and oil. In 1958, CPR created a separate company, Canadian Pacific Oil and Gas Limited, to hold its mineral rights. In the following years, these mineral rights were sold off, acquired and merged in and out of multiple entities. For example, in 1971, Canadian Pacific Oil and Gas merged with Central-Del Rio Oils to form PanCanadian Petroleum Limited which later became PanCanadian Energy Corp. Then in 2002, PanCanadian Energy merged with Alberta Energy and was renamed Encana.

PrairieSky entered the stage and IPO’d when it purchased mineral rights from Encana in 2014. It went on to acquire more rights across Western Canada from Northeast British Columbia to Western Manitoba. Two acquisitions of note were Range Royalty in December of 2014 with 3.5 million royalty acres giving PrairieSky exposure to the prolific light oil Viking play in Western Saskatchewan. The second was the purchase of nearly all of Canadian Natural Resources Limited royalty assets in 2015.

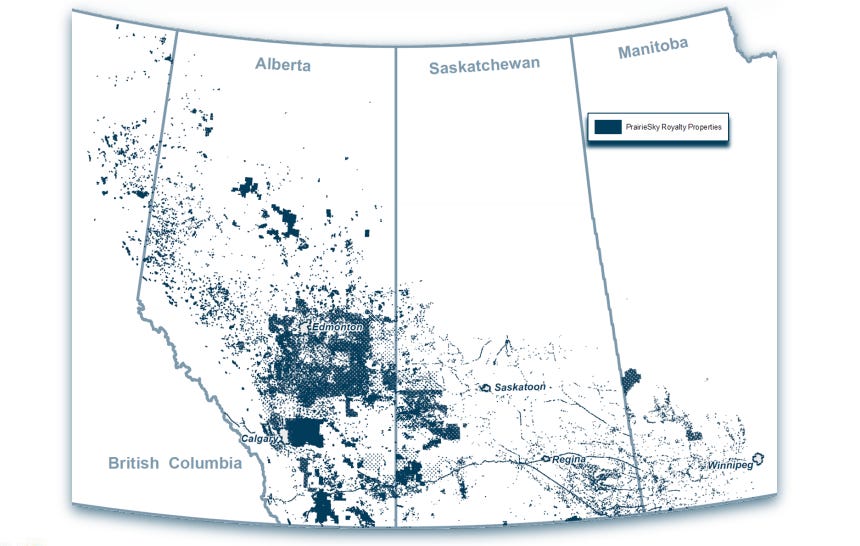

Today, PrairieSky owns a portfolio of 18.3 million royalty acres.

The company’s business model

Long-time readers and listeners well know our affinity for commodity royalty companies. This affinity stems from the hard asset, asset-light nature of the business model which we believe provides exposure to the inflation-beneficiary characteristics of hard assets while avoiding the boom, bust cyclicality common in the commodity sector. A business model like PrairieSky Royalty’s is the perfect sweet spot.

The core of that business model is land. In fact, that’s basically all there is to it.

Grasping the scale of 18.3 million acres can be difficult. So if you can, imagine a plot of land a bit bigger than the US state of West Virginia and a bit smaller than South Carolina, and you’ll have an approximation for just how many royalty acres PrairieSky owns. For those interested in the breakdown, 9.7 million acres are fee simple lands and 8.6 million acres are gross overriding royalty (GORR) lands. By far this makes PrairieSky Canada’s largest private owner of mineral rights.

Simply owning land is a hard asset-based, inflation-resistant business model in its own right, and one successfully employed by many private and public companies. But PrairieSky’s main business is cashing checks from its massive royalty portfolio.

In 2022, revenues amounted to $643 million, $615 million of which was royalty production revenue.

As of year end 2022, these revenues were produced off of 43,000 wells with an average royalty rate of 6%. The wells are operated by 315 companies, half of which are private and half public. Seventy-five percent of PrairieSky’s revenues come from the 31 largest lessees.

But here’s where it gets interesting. Despite all this activity occurring on it’s land, PrairieSky runs a lean operation that produces loads of cash and high margins.

Consider that against royalty revenues of $615 million, the company only incurred $32 million of operating expenses, maintaining a royalty operating margin of 95% and an overall operating margin of 84%. This is due in large part to the fact that PrairieSky has only 65 employees. A small employee base is one of our favorite characteristics of royalty companies because one of the fastest rising costs during periods of high inflation is salaries.

Additionally, unlike companies with non-operator-based business models (we wrote up one such company, Vitesse Energy), a pure-play royalty company like PrairieSky takes no part in the exploration for or production of oil or natural gas on its land. It simply owns the land and/or mineral rights, let’s third parties explore and extract the commodities, and it simply collects royalties.

The preceding few paragraphs discussed the benefit of PrairieSky not participating in the production of the minerals on its properties, evidenced by its stellar operating margin. The benefit of not participating in exploration is equally staggering

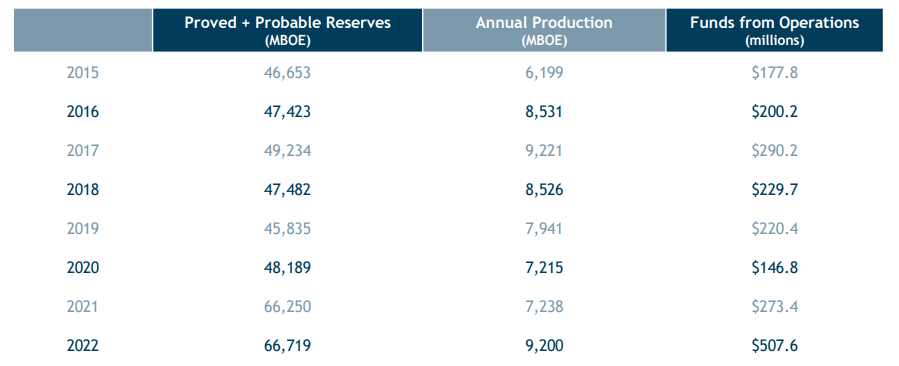

The table below lists PrairieSky’s proved and probable reserves and annual royalty production. What is immediately clear is, in 2015 PrairieSky had a proved and probable reserves of 46,653 MBOE and seven years later its reserves are 66,719 MBOE. So not only didn’t its reserves decrease over time, they increased. And the costs to maintain and grow those reserves were fully born by the operating companies.

Over those same years, 64,071 MBOE of royalty production were extracted from the land netting PrairieSky about $2 billion.

So because of its pure-play royalty model, PrairieSky has no direct exposure to the negatives of capital costs, maintenance capital expenditures, environmental liabilities, or operation costs. On the flip side, it is positively exposed to the upside of new reserve discoveries, and advances in oil and gas recovery technology—all at no expense to itself.

On top of all that, PrairieSky has a lot of future optionality in its 11 million leasable but still undeveloped acres.

But by far our favorite aspect of a royalty company is its hard asset, asset-light nature and how that relates to inflation. Consider for example, as inflation, or monetary debasement, increases, the price of commodities and thus the revenues for a royalty company should also increase. At the same time, because it is asset-light, expenses will likely increase at a much slower rate. This dynamic leads to margin expansion and overall greater profitability.

The company’s strategy

But while a royalty-based business model is an advantage, it’s still necessary for the company to be run well. From our research, it appears PrairieSky is run exceptionally well. Its strategy as laid out on its website as the following:

PrairieSky’s objective is to generate significant cash flow and growth for shareholders through indirect crude oil and natural gas investment at relatively low risk and low cost to the company.

Because there’s not too many details there, let’s take a quick look at specific steps the company is taking to achieve its goal.

The first step is “focusing on leasing activity and organic growth of royalty production revenue from the royalty properties.” For PrairieSky, organic growth comes out of the pocketbooks of the companies leasing its land. But the company has to a good job of purchasing high quality royalty assets with high probabilities of being developed by producers.

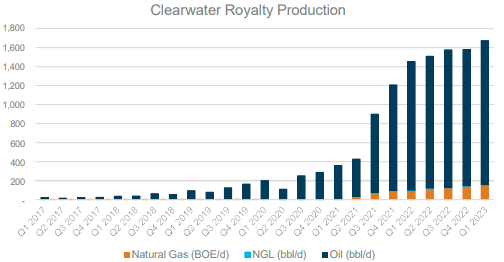

One encouraging example, is the investment made of assets in the Canadian Clearwater trend back in 2017. This was before Clearwater became the largest conventional play in Canada. Take a look at the organic growth in royalty production from this one investment in the chart below. It shows royalty production increasing from practically zero to over 1,600 bbl/d in just six years.

Secondly the company focuses on “proactively monitoring and managing the portfolio of royalty properties to ensure third-party adherence to lease terms and contracts.” This part of the strategy is where PrairieSky makes sure all of its lessees pay their dues. We can only imagine this is a very tedious and not very enjoyable aspect of the job, but it’s a profitable one and necessary for maintaining a good working relationship with all of the lessees.

The third focus is “managing controllable costs.” Much of this goal is taken care of through its asset-light business model. And enough has been said on that already.

The fourth focus is “selectively pursuing strategic business development opportunities that are relatively low risk to the company and accretive to shareholders.” This is where we become very critical. It is very easy for managements to make unwise acquisitions. It is better to do nothing than to make a bad purchase.

Thankfully, PrairieSky’s management seems level-headed and aims to make purchases that are accretive on an acres-per-share basis. As can be seen on the right side of the image below, since IPO, even though shares have been issued to finance acquisitions, the acres per million shares has increased 92%.

The left side of the image shows that on a production-per-million-shares basis, the results have been flat to down. While this trend is less than encouraging to date, we believe that with 60% of its leasable land still undeveloped the graph on the left should move up and to the right over time.

The last part of the company’s strategy is to “distribute the majority of cash flow in the form of dividends and share repurchases and cancellations over time.” Even accounting for a conservative dividend payout ratio, which the company maintains to build up cash for acquisitions, the vast majority of funds from operations since IPO have been distributed to shareholders. As illustrated in the chart below, since its IPO to the end of Q1 2023, PrairieSky returned $1.4 billion in dividends and $246 million in share buybacks.

So with that summary of PrairieSky under our belts, let’s take a look at the situation we hinted at two weeks ago.

The situation

If you put a gun to our head, we’d say for us, PrairieSky is more of a “general” than a “workout” type investment. For those who need a refresher, generals and workouts are terms Warren Buffett used to delineate between investments in long-term, solid companies, and those in special situations. That said, we do believe the completion of the Trans Mountain Pipeline Expansion will have a material and noticeable positive impact on the company’s revenues. In fact, PrairieSky’s management believes so as well.

In the latest investor presentation, management stated the following:

Looking ahead, output is expected to remain at or close to this robust level in coming months and to get a boost toward the end of 2023 after the completion of the Trans Mountain Expansion pipeline project.

The map of PrairieSky’s royalty acreage, shown earlier in this piece, reveals a large percentage of its royalties are in Alberta and that the densest royalty ownership is around Albert’s capital city, Edmonton, precisely where the Trans Mountain Pipeline begins. We believe many of PrairieSky’s top lessees such as Cenovus Energy, Canadian Natural Resources, and Whitecap Resources will be some of the biggest beneficiaries of the project’s completion. PrairieSky should benefit in turn.

Of the three benefits we identified for Canadian oil producers, we believe two will benefit PrairieSky: greater transportation capacity and a decrease in the Western Canadian Select (WCS) discount.

In A Tale of Two Pipelines we discussed how in nearly every month since 2017 the amount of oil available to transport via the Trans Mountain Pipeline exceeded the 300,000 barrels per day capacity. And the situation is similar across Canada as oil transportation infrastructure is operated at or near full capacity. With the completion of the pipeline expansion, transportation capacity will increase by 500,000 more barrels per day. Since total production in Alberta in 2022 was 3.75 million barrels per day, a rough calculation tells us the expansion could potentially allow about 12% more product to be shipped out of Alberta, indirectly increasing PrairieSky royalty revenue.

The other benefit is a potential closing of the WCS price discount. Currently, WCS (the benchmark price of Canadian heavy crude) trades at a steep discount to WTI and other benchmarks around the globe. One of the main factors is the majority of Canadian oil is sold into the United States because current Canadian infrastructure allows only a small fraction of crude to be exported outside of North America. The Trans Mountain Pipeline expansion will increase Canada’s export capacity. To be sure, there are more factors that play into this discount, for example, refinery capacity and availability, oil quality, and the great distance Canadian crude is transported.

But, since “the extremes inform the means,” let’s consider a situation where the WCS were to trade at the price of WTI. How would PrairieSky’s revenues be effected?

In the latest quarter, the average WCS discount to WTI was $25 per barrel and PrairieSky averaged 12,166 barrels per day of royalty production. That means, if the discount were to close, PrairieSky’s revenue per day could have been $304,150 per day higher. On a by-quarter-basis, this would have increased revenues by $27.3 million or 18%.

Obviously, because of our simplification and assumptions, this is the high range of potential impact. But if both greater product is shipped and the WCS discount is decreased, the potential positive impact on PrairieSky’s revenues could be substantial. If nothing else, the company’s management expects it to be noticeable.

Perpetual call option

As we conclude this episode, a disclosure is necessary as one of the hosts owns a stake in PrairieSky Royalty. Also, to reiterate, while we believe a near-term catalyst for higher revenues is approaching, we consider this investment a long-term general not a short-term workout.

Because of its advantageous set up with immense upside and limited downside optionality, invested and prudent management, and the massive hard asset, asset-light portfolio, we look at PrairieSky Royalty as a perpetual call option on inflation, oil, and land—one that might just lead our grandchildren to realize there really was something going on between the ears of their old pops.

With that, we’ll wrap up this latest episode of Special Situation Investing. Thank you for supporting our work by sharing this and other pieces with your friends, family, second cousins, coworkers and random acquaintances. We’ll see you all next Saturday on another episode.

PrairieSky Royalty (PREKF)