Welcome to Episode 122 of Special Situation Investing.

The book Good to Great explores why some businesses achieve greatness. Within its pages, the author, Jim Collins, popularized the concept of the Flywheel Effect. He draws a connection between turning a flywheel—a heavy disc-like structure that stores rotational energy—and successful companies in the following way:

The flywheel image captures the overall feel of what it was like inside the companies as they went from good to great. No matter how dramatic the end result, the good-to-great transformations never happened in one fell swoop. There was no single defining action, no grand program, no one killer innovation, no solitary lucky break, no wrenching revolution. Good to great comes about by a cumulative process-step by step, action by action, decision by decision, turn by turn of the flywheel-that adds up to sustained and spectacular results.A flywheel, and better yet, a frictionless one, comes to mind when we think of FRMO Corporation.

To be frank, we’ve owned this company for a while but avoided writing it up until now. This is not because we wanted to keep a good thing to ourselves but because it’s such a unique company with disparate parts and an odd history that creating a coherent write-up was challenging. But because we like the company, and because we do want to share a good thing, we have done our best to overcome the challenge.

The Company History

FRMO Corp (FRMO), which stands for Financial Risk Management Organization, is a low-volume, $325 million market cap investment holding company that trades on the OTC Pink Sheet market. It was founded by Murray Stahl and Steven Bregman of Horizon Kinetics along with a few partners in 2001.

The original thesis for the business was as a holding company which would buy revenue interests in investment products created at the then Horizon Asset Management, a company also run by Stahl and Bregman. Stahl explained the intent behind FRMO at the 2012 annual shareholder meeting:

We were founded as what we called at the time an “intellectual capital company.” The idea was that, given our positions in then-Horizon Asset Management, we would occasionally find an interesting investment idea that was at its inception stage and had virtually no revenue. Horizon would sell FRMO Corporation a revenue interest in that product and, if it was successful, the corporation would collect a certain amount of revenue from it with very little associated expenses.

During a conference call, a year later, he added further details:

You should not forget the objective of FRMO…The idea is to use our research capability and use our so-called intellectual capital…to create revenues without the requirement of commensurate large capital investments. The difference between the cost of the products we create and the revenues that we receive, if we’re right, should result in a reasonably robust return on equity. A lot of seedlings have been planted in the last year and in the next couple of months we will see whether or not they actually bear fruit.

The investment products of Horizon Asset Management proved successful and FRMO’s revenue streams materialized and grew. These in turn were reinvested, sometimes in more Horizon products, sometimes in separate investments.

In 2011, Horizon Asset Management LLC and Kinetics Asset Management LLC combined into Horizon Kinetics LLC. Along the way, the revenue streams from multiple separate investment products were sold back to Horizon Kinetics in exchange for an equity interest in the combined company and a gross revenue share. Today, FRMO owns a 4.95% equity stake and a 4.199% of gross revenue interest in Horizon Kinetics. Horizon Kinetics is one of FRMO’s most lucrative investments but is not its only one. Other top holdings will be discussed shortly.

At this point, it’s natural to ask, why FRMO was created in the first place and why couldn’t Stahl and Bregman do everything through Horizon Kinetics. It’s a great question, one the two gentlemen have been asked in numerous earnings calls.

One reason is the founders were looking ahead and building a vehicle through which their heirs could access liquidity, largely for charitable purposes. In 2012, Stahl said the following:

For me, the ultimate destiny of FRMO is that I don’t intend to sell my stock. I intend to build up the market value and place … all my shares [in] … a family foundation, and I want my kids to basically run the family foundation and give money to charity.

Because Horizon Kinetics is a private company, it is difficult to extract liquidity for any owner of substance. A liquid, publicly traded company would fix this issue.

Another reason is taxes. If you study Murray Stahl’s track record of investments over the decades, it’s impressive how much he thinks about minimizing the negative effect of taxes, and how effective he is at legally doing so. FRMO provided a more efficient vehicle for revenue streams. Stahl clarifies:

Now, for tax purposes, Horizon Kinetics is a Subchapter S corporation. If you’re a Subchapter S corporation based in the city of New York, they hit you with every tax you can possibly imagine. If you’re a C Corp, you’re advantaged in taxes, at least from that point of view. And you can judge the rest of it. It’s better to have more of your cash flow in a C Corp than it is an S Corp.

Another reason is FRMO provides a source of permanent capital. Stahl notes that the business of Horizon Kinetics is largely comprised of funds—closed funds, mutual funds, ETFs, and the like—and thus the flow of capital in and out is subject to the whims of those invested in the funds. Often flows come in at the worst times—after a large runup in NAV, for example—and often flow out at the worst times as well—during bear markets when assets are cheap. FRMO would not suffer the same drawback.

A final reason for FRMO’s existence is it provides a vehicle for raising capital through the issuance of shares, a task more tedious to accomplish within a private company.

With that summary of the how and why of FRMO’s creation out of the way, we’ll next look at details of the company as it exists today, before looking at what the company is becoming.

The Company Today

FRMO is unique. It has no debt, other than a small mortgage of less than one million. It has only three employees, Stahl and Bregman, and the company’s secretary. Neither Stahl nor Bregman take any compensation, either cash or stock for their work in FRMO. It has an odd name, one that when typed will likely autocorrect to the word “from.” It has a confusing interconnectedness with its founders’ other businesses and investment vehicles, one that reminds us of Buffett and Munger’s early spaghetti-like network of investments prior to consolidating everything within Berkshire. And finally, it has a $325 million market cap, but still lists on the OTC Pink Sheet market.

But unlike many pink sheet companies, FRMO provides detailed disclosure including: annual letters, annual shareholder meeting transcripts, quarterly reports and quarterly conference call transcripts. All of these can be found at the company’s website frmocorp.com.

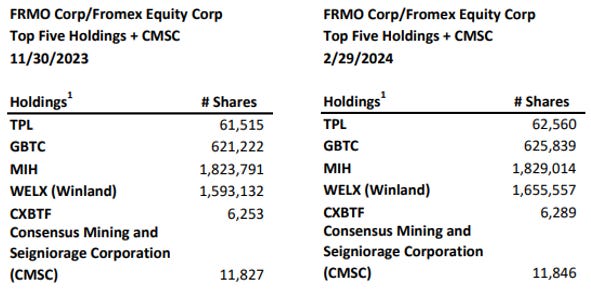

In addition, the company provides a quarterly summary of its top five holdings and its crypto holdings.

These summaries give a good feel for the current makeup of FRMO.

The first holding should come as no surprise to anyone familiar with Murray Stahl. Texas Pacific Land Corporation has been discussed in depth by us in previous pieces. A couple of comments about the TPL shares owned by FRMO listed above. First, it’s worth noting that FRMO is acquiring shares even after Stahl recently lost a court battle with the company. And secondly, the number of shares listed in the image above does not take into account the recent 3-for-1 split. Next quarter, these numbers should increase by three times.

The second top holding is Greyscale Bitcoin Trust, GBTC. We wrote a piece on GBTC back in November, when it was still a trust trading as a considerable discount to NAV. Stahl and Horizon Kinetics have been large holders of GBTC for years. They made their first bitcoin investments back in 2015. At the time the amounts invested were extremely small to mitigate the uncertainty of the bitcoin experiment. Since then, it has appreciated so much that it rivals TPL as Horizon Kinetics’ largest position. As shown above, FRMO holds 625,839 units of GBTC, worth over $34 million, and it is still buying more shares.

MIAX Options Exchange is FRMO’s third major holding. This investment is the result of long-term holdings of separate stock exchanges that were merged into MIAX, specifically investments in the Minneapolis Grain Exchange and the Bermuda Stock Exchange. Today, MIAX is privately held, but is in the process of pursuing a public listing.

Next on the list is Winland Holdings (WELX). On the surface, the company is a small manufacturer of a portfolio of environmental sensors. But over the last few years, while keeping its sensor business intact, under the surface, Winland transformed itself into a crypto mining business. As we understand it, a while back, one of Horizon Kinetics’ employees, Matthew Houk, bought a large stake in Winland with the intent of turning the business around and creating value. Stahl took notice of the company and realized it was a good platform on which to build a crypto business. He approached Houk and the transformation began with FRMO assisting Winland. In the process, FRMO bought a large, and soon-to-be controlling, stake in the company.

The fifth place on FRMO’s top five list is CXBTF which is a bitcoin tracker ETF.

Although not in the top five, Consensus Mining and Seigniorage Company is also listed in the quarterly summary because of how often investors ask for details on FRMO’s stake in this company. In short, this is a private crypto mining company that Stahl and Horizon Kinetics have built from the ground up and are in the process of bringing public.

The top five list captures the big hitters but not the totality of FRMO’s investments. Others of note include: the afore mentioned equity interest and revenue share in Horizon Kinetics, $38 million of cash and cash equivalents, a position in the Canadian Stock Exchange Markets, and small positions in a private crypto mining equipment repair business and Digital Currency Group. FRMO also owns its own crypto mining equipment—valued at $1.3 million in its latest report—with which it directly mines crypto currencies.

Below is a list of cryptocurrencies held by FRMO both directly and indirectly.

If this seems to you like a disparate and eclectic collection of investments, you’re not alone. It’s apparent from the questions Stahl and Bregman get on earnings calls that many investors struggle to understand what FRMO does and where it’s going. One major reason for the current confusion is because FRMO is transitioning to becoming an operating company. In fact, that was Stahl and Bregman’s intent from the start.

The Company Future

Since its founding, the intention for FRMO was for it to become an operating company. Initially Stahl and Bregman thought they would purchase another operating company but they failed to find a company that met their strict criteria. As a result, the team decided to build their own. What type of business to build became the question. Enter cryptocurrency. Stahl explains:

So, what do we do in FRMO? We want to establish a business, and we wanted to buy something. There are certain opportunities that we looked at. They were interesting. We just don’t know enough about those businesses. Other businesses, you could argue, we knew a lot about those, but interest rates were very low, and they were unduly expensive—not because the businesses themselves were expensive, it’s that the ultra-low interest rates make them expensive, and we could never have earned a justifiable return on capital. Then, lo and behold, some years ago, cryptocurrency makes an appearance. Cryptocurrency is interesting. Of course, we had no experience in cryptocurrency, and no expertise in it. But neither did anybody else, so we were all starting at the same level. One of the benefits of cryptocurrency was that we didn’t have to buy a business, because no one had a business to sell. We just gradually expanded.

Stahl got involved with bitcoin in 2015. With an extensive background in computer science and cryptography, he immediately recognized the merits of the bitcoin network and soon invested $700,000 of his personal money in bitcoin. He followed that with buying his own mining equipment to learn about that aspect of the industry.

Over the ensuing nine years, Stahl, Horizon Kinetics and FRMO have employed a step-wise approach to building positions in cryptocurrencies and a network of mining operations. These efforts resulted in Horizon Kinetics developing crypto mining-based funds, immense holdings of GBTC, the creation of Consensus Mining, direct mining in both HK and FRMO, and FRMO’s growing position in Winland Holdings, among other crypto investments.

Stahl recently stated:

So far, the crypto is getting to be pretty considerable, and we keep buying crypto-related assets. Eventually, it’s all going to coalesce, and some day you are going to see regular operating earnings from it when the cryptocurrency business is something that’s really much better understood by the public. Right now, I don’t think it’s very well understood by the public. Eventually, people will get it. In the meantime, we’re just going to keep growing it.

The first step in the coalesce appears to be buying 51% or more of Winland Holdings. At that point FRMO would have reportable earnings for the first time. As of the latest quarter, FRMO owned 35% of Winland, and Stahl said the company plans to continue buying more starting May 1st.

How the rest of the crypto assets get consolidated, or not, is yet to be seen. But the trajectory is clear: FRMO is becoming a crypto mining company.

For those wary of investments in crypto because of the messy history of the industry, we don’t have the space or time here to impress upon you just how differently Stahl has approached the sector. Because of certain peculiarities of bitcoin economics, specifically the four-year halving and mining equipment pricing, Stahl has taken a measured, conservative, step-wise, and uniquely successful approach. This has allowed his investments to weather the multiple “crypto winters” that bankrupted so many other mining companies.

For more information on Stahl’s approach to crypto, check out the piece by

titled: FRMO Corp: The 2022 Crypto Winter and FRMO's vertically modular crypto conglomerate.The Flywheel

As we prepare to wrap up this episode, let’s circle back to the concept of the flywheel with another quote from Jim Collins.

Each turn [of the flywheel] builds upon previous work as you make a series of good decisions, supremely well executed, that compound one upon another. This is how you build greatness.This describes how we feel about FRMO, its history and its future.

Take a look at the first sentence in FRMO’s earliest disclosure listed on its website. The sentence—written while the world was still reeling from the Great Financial Crisis— reads:

During the past year, much has occurred in the financial markets. Fortunately, none of this has occurred at our firm. FRMO has undertaken no debt. It has not accumulated liabilities. It has merely continued to develop its own resources internally, albeit from a very low base.

FRMO’s approach in 2002 is still its approach today—the slow, conservative, step-wise creation of shareholder value. What has changed is that FRMO is no longer starting from “a very low base.” Shareholder equity, that was approximately $10,000 in 2002, is now north of $350 million. The chart below shows shareholder equity growth starting in 2009 to the present.

This increase came from, as Collins puts it, “no single defining action, no grand program, no killer innovation, no solitary lucky break, no wrenching revolution” but instead “a cumulative process, step by step, action by action, decision by decision.”

That said, we believe FRMO is approaching an infection point for two reasons.

Firstly, as FRMO becomes a crypto mining company the confusion investors currently suffer about whether the company is a portfolio of investments or an operating company will vanish. FRMO will likely then trade at a premium to its NAV based on its operating performance.

The second reason is because a number of private holdings within FRMO’s portfolio are in the process of coming public. These holdings include: Horizon Kinetics, MIAX, and Consensus Mining. (Canadian Stock Exchange is another likely candidate but is not yet in the process.)

Horizon Kinetics has a planned IPO for sometime this summer and it provides an example of how a private holding going public can affect FRMO shareholder equity. Running some numbers that Stahl laid out in the latest earnings call, we calculated that FRMO’s equity stake in Horizon Kinetics should be worth $30 million, not the $10 million at which it’s currently held on the books. While not earth-shattering, this will be yet another step-wise increase in shareholder value.

The magnitude of the effect of each entity coming public will vary but we expect each to have a positive effect on FRMO’s shareholder value.

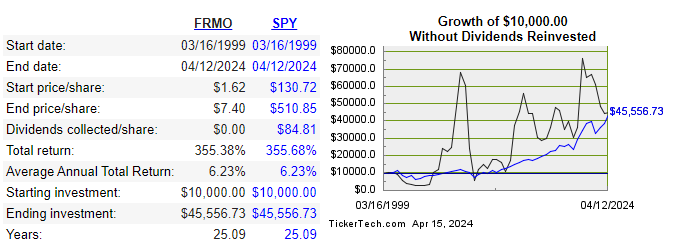

As these catalysts take place, we expect FRMO’s share price—which to date has largely kept up with the S&P 500 since inception—to begin to outperform.

As we patiently watch this flywheel spin ever faster, we’re in good company, as FRMO’s directors and executives own 75% of the company. They aren’t selling. We think we’ll sit tight too.

Conclusion

As always, thanks for reading and listening! The best way to support is to become a free subscriber and share our work with a friend. Thank you! We’ll see you all in two weeks with our next piece.

Share this post