Welcome to episode 142 of Special Situation Investing.

Vitalik Buterin launched Ethereum in July of 2015 intending to create a crypto currency that was more than just a payments network. On June 17th, 2016, a hacker attacked a Decentralized Autonomous Organization (DAO) on the Ethereum network and stole $50 million worth of Ethereum. Ethereum itself was not hacked, but rather poorly written code on the part of the DAO was responsible for the vulnerability. In any case, controversy resulting from the hack led to a fork in the blockchain. Ethereum developers altered the Ethereum block chain to undo the theft and Ethereum Classic was created to perpetuate the original Ethereum blockchain, including the theft, unaltered.

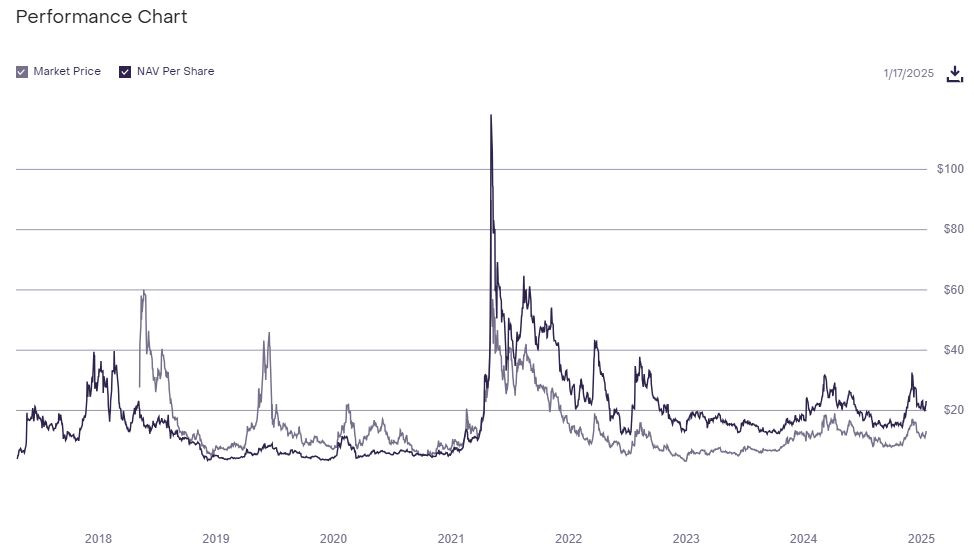

On April 24th, 2017, Grayscale launched the Grayscale Ethereum Classic Investment Trust (ETCG). The trust sought to provide investors exposure to Ethereum Classic (ETC) in the form of a security while avoiding the challenges of buying, storing, and safekeeping ETC, directly. The fund charges a 2.5% management fee, and, being a closed end fund, trades both above and below NAV at various times.

On September 15th, 2022, developers once again modified Ethereum. In an event known as “The Merge,” Ethereum switched from a proof of work network to a proof of stake network. Ethereum Classic, again, continued unaltered and remains a proof of work network to this day.

Hashrate

Proof of work blockchains allow investors unique insight into the production cost of the underlying cryptocurrency. In the self interested pursuit of transaction fees and block rewards, miners devote ever increasing amounts of capital, in the form of compute power, to block validation. The aggregate compute power dedicated to any given proof of work blockchain is expressed as the networks hashrate. As the networks hashrate increases, so, too, does the cost to mine that cryptocurrency. In the same way that higher cost of goods sold lead a business owner to sell products at a higher price, an increased hashrate leads to higher coin prices.

Overlaying the hashrate and spot price of a crypto currency over time reveals a high degree of correlation between the two metrics. While spot price occasionally rises well above hashrate, signifying extreme market tops, it rarely dips very far below hashrate, and over time the two metrics are correlated. This is not a chartist approach to crypto investing, but rather, a graphical depiction of the cost of goods sold and its effect on spot price.

For much of its history, ETC’s spot price led the hashrate, but from September 2022, through today, hashrate has significantly led the spot price. The flip is logical given that Ethereum miners were forced to either shut down or shift to mining ETC following Ethereum’s transition from proof of work to proof of stake. This transition caused a surge in ETC’s hashrate, but not a corresponding surge in the price. If the economics of crypto mining play out, however, the price will eventually rise to a more normalized level and trade in line with what is still a rising hashrate.

(ETCG) Discount to NAV

As of this writing, Grayscale’s ETCG fund trades at a 43% discount to NAV, giving ETCG investors a margin of safety over those who purchase ETC directly. A cursory review of ETCG’s price to NAV history reveals multiple past opportunities to sell shares at a premium to NAV, and it’s reasonable to expect similar opportunities in the future.

Exactly which catalyst will eliminate ETCG’s price to NAV discount can’t be known in advance, but there are several possibilities. In one scenario, ETC’s spot price might rise and trade inline with the networks hash rate. A rising ETC price and the ensuing bullish sentiment around the asset could lead to an increase in ETCG’s price per share, along with the elimination of the funds current discount to NAV. In another scenario, approval of an Ethereum Classic ETF and conversion of ETCG from a closed end fund to an ETF, would eliminate the price to NAV discount. Regardless of the specific catalyst, buying a dollar bill for 50 cents isn’t a bad starting place for any investment thesis.

Bullish Sentiment

While I never recommend investing based on sentiment, investor enthusiasm is a nice tailwind to have, and sentiment for crypto has never been higher than it is today. From crypto’s beginning to only the very recent past, claims of crypto crackdowns and government bans where commonplace. The mood around crypto ranged from euphoria to impending doom, depending on the moment, but full on acceptance of the asset, among legitimate investors, was guarded at best.

Currently, however, with talks of a strategic bitcoin reserve and a presidential crypto advisory council in the works, crypto appears to have turned a page. That the turning of a page came early in bitcoins most recent halving cycle, when both bitcoin and alt coins typically run up in price, is an added bonus. In past cycles, bitcoin and altcoins managed to stage bull runs despite resistance from the establishment, and will likely do so again as entities that once apposed crypto turn to embrace it.

Conclusion.

My investment in ETCG fits into the category of a small asymmetric bet. In other words, I haven’t put any more into the idea than I’d be willing to loose gambling over the weekend in Las Vegas. Actually, it’s more than that amount, because I wouldn’t be willing to gamble any money away in Las Vegas, but you get the idea. This might seem contradictory given last weeks reminder to maintain a focused portfolio, but I do believe in the benefits of placing small asymmetric bets to augment my larger positions. I keep these bets small enough that if they go to zero I won’t notice, but if they appreciate dramatically, I’ll still reap the benefits.

Share this post