Welcome to Episode 140 of Special Situation Investing.

We use these pieces to summarize updates from quarterly reports and earnings calls of companies in our portfolios and occasional honorable mentions from our watchlist. The goal is to record highlights, succinctly capturing our current thoughts for future reflection. We hope you find these updates valuable.

But first, please have fun filling out the following poll.

Given bitcoin’s recent peak above $100K per coin, we thought it’d be interesting to capture our audience’s thoughts on the asset. Thanks in advance!

Texas Pacific Land (TPL)

It’s been a wild ride over the last three months for TPL shareholders with a number of interesting developments.

First, this was the second quarter in a row where the company acquired additional acreage, once again in an all-cash deal. It most recently spent $286 million on approximately seventy-five hundred net royalty acres.

These are the details from the company’s press release:

The interests span across approximately 7,490 net royalty acres (“NRA”) located primarily in the Midland Basin in Martin (~2,220 NRA), Midland (~2,080 NRA), and other counties, with over 80% of the acquired interests adjacent to or overlapping existing TPL surface and royalty acreage. Exxon Mobil Corporation (NYSE: XOM) and Diamondback Energy Inc (NYSE: FANG) operate approximately 66% of the acreage. The acquired assets have current production of approximately 1,300 barrels of oil equivalent per day (~78% liquids), with strong line of sight to near-term development and production growth.

Only time will tell how accretive these acquisitions will be. Odds are good that management and the board made a prudent purchase since they are largely buying acres adjacent to land they already own or simply increased the royalty percentage on surface where they already own royalties. Thus, they likely have excellent visibility on current and future cashflows. The CEO summarized the acquisitions the company completed over the last two quarters, saying, “aggregating [the] deals, we expect them to generate double-digit cash flow yield at a flat $70 oil price.” At a conservative 10% FCF yield, this could add $45.5 million to TPL’s approximate $420 million of FCF per year.

Third quarter results were fantastic. One highlight worth mentioning is the water side of the business. It continues to grow, collecting royalties on an estimated one billion barrels of water through the end of 2024. This segment of net income is set to match last year’s record (shown below) at about $100 million.

Last but not least, TPL exited the S&P 400 and joined the S&P 500 on the 26th of November. When we shared the announcement on Substack, some readers expressed concerns that, while inclusion in the index will expose the stock to passive tailwinds during bull markets, it will expose the company to the negative flipside of that coin. For us it’s a non-issue. If panicked withdrawals cause TPL’s price to drop, we couldn’t be happier.

Speaking of a price drop, basically since its graduation to the S&P500, TPL’s price has dropped approximately 33%. Is this simply due to its inclusion in the index? We think not. Is it solely related to lower oil prices? Unlikely. Is it due to technical reasons related to the actions of a similar company? We heard a convincing argument in that regard. None-the-less, have we bought more recently? Yes.

Landbridge (LB)

To date, our piece on Landbridge is our most popular. Its popularity is likely because the company recently IPO’d, more than tripled since, and because of its connection artificial intelligence. In a recent interview, the company’s chairman reiterated why Landbridge’s acreage in West Texas could house “large contiguous data center campuses,” namely:

No large population centers

Water from oil production and natural aquifers

Lowest cost gas in North America

Great fiber connectivity

Attractive regulatory regime in Texas

Great carbon sequestration options

We talked about all of those advantages in previous pieces, except for the last one. Regarding that point, he went on to say:

We Five Point Energy have a carbon sequestration portfolio company that gathers off-spent gas and high in CO2 suffer, separates it and sequesters it. We could very easily connect up our power plants and take all the CO2 emissions and sequester them as well.

While carbon sequestration options are part of what could attract hyper and exa-scaler data center companies to the Permian Basin, it’s also a potential source of revenue for LB as royalties could be collected on carbon injected on its acreage.

That brings up another point. A number of our readers have asked the following question: What happens to the investment thesis of LB if data centers don’t come to the Permian Basin? In response we point out that Landbridge is already in the process of finalizing a data center land lease agreement. We also highlight Landbridge’s numerous revenue sources even without data centers. Royalties from mineral rights and water come immediately to mind. In addition to potential carbon sequestration, Capobianco mentions royalties on caliche (a concrete like substance used for construction) and sand (used for fracking). So with or without data centers, Landbridge has a future.

Out of the entire interview, here’s the quote from Capobianco that I found most eye-opening. He said:

What we've done which gives us a little bit of an advantage, and I think strengthens the business model for Landbridge, is we have Waterbridge that builds out water infrastructure on our land. We have a creatively named powered land company, called Powered Land, that builds out data center infrastructure. And we ourselves are working very hard to build infrastructure on that land.

But that said, we are open for business and there's no better solution for Landbridge than to have my portfolio companies building out infrastructure on their land, others building out infrastructure on their land, and particularly data center infrastructure because the more data center capacity you have in a given location the greater value that data center capacity becomes. You know Langley Virginia is a both a cloud and an inference location because of the amount of data center capacity that's collocated. At first in a place like West Texas we'll be talking about only large language model learning and inference, but over time you can get the cloud computing and real-time connectivity as you get greater and greater capacity that's collocated in a market.

Two things stood out to me.

This was the first time I had heard of the private company Powered Land. It doesn’t show up in the list of other companies underneath Five Point Energy listed on its website. But a quick google search reveals Five Point Energy submitted a trade mark application for “Powered Land” at the end of last August. A list categorizing the “good and services” Powered Land will provide includes: construction and design of data centers; leasing of space in data centers; leasing of space for construction of data centers, generation of solar power, wind-generated power, and electricity, distribution and transmission of natural gas, solar power, wind-generated power; and electricity, and leasing of data center facilities, and rental of data center facilities.

It appears Five Point Energy is not just hoping companies will come and build on Landbridge’s land, it is literally paving the way by creating the infrastructure itself that it intends to rent out to hyperscalers. This is fantastic news.

The second thing that stood out in the highlights paragraph above was when Capobianco says:

At first in a place like West Texas we'll be talking about only large language model learning and inference, but over time you can get the cloud computing and real-time connectivity…

It’s clear the distant reaches of West Texas are well suited to house data centers where inference isn’t a factor, aka those for large language learning models. But exactly why data centers housing real-time computing could also be built in the basin after capacity reaches a certain scale, leaves me scratching my head as to why. While if true, this is bullish and exciting, I clearly don’t understand the technology well enough yet. More research is needed. If any readers have insights on this matter, please expound in the comments.

The last note on Landbridge is that the lockup period for insiders after IPO appears to be over. On 12 December, Capobianco sold roughly 2.5 million shares for $60.03 each. After this transaction, the chairman still owns 53.2 million shares. While I don’t like seeing insiders sell, this is not unexpected. If I successfully IPO’d a company and had the opportunity to cash out $150 million, by selling only 4.5% of my shares, I probably would too. A lot of further selling would be something to pay attention to. While some see Capobianco’s 73% ownership of the company as a risk, my cohost and I rather look at it as an opportunity to invest alongside a talented operator.

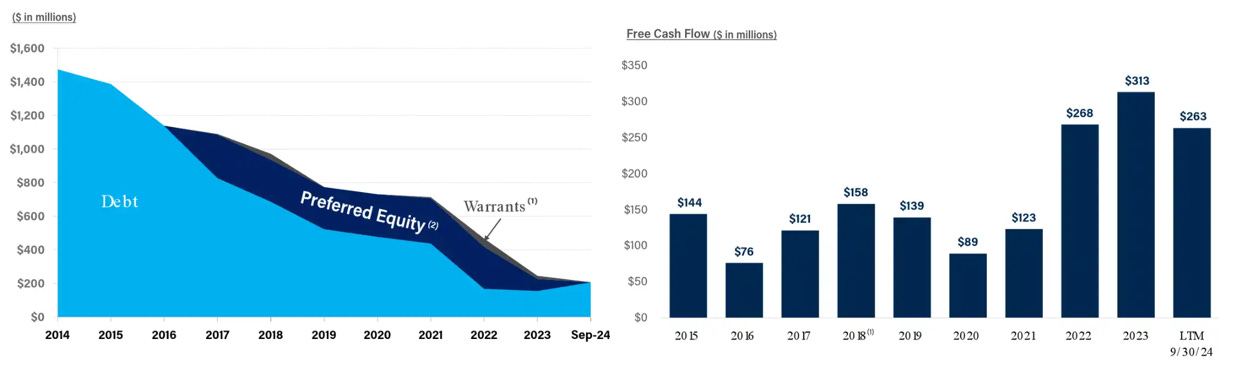

Natural Resource Partners (NRP)

There are no large updates to report for Natural Resource Partners. The payoff of debt continues with preferred equity and warrants being recently eliminated and only $181 million of debt remaining.

Annualizing last quarter’s $55 million in cashflow would suggest debt could be reduced to zero in less than a year. But, in an interview on the Stock Picker’s Corner, coal expert, Matt Warder, estimated NRP’s 2025 cashflow (at his projected prices for met and thermal coal) at $150 million. If that plays out, debt repayment may remain the company’s priority for another year yet. Balance that with comments during the earnings made by NRP’s CEO indicating debt may not need to be brought to exactly zero, and cashflow could be allocated to other uses if debt is reduced to a near-zero target the management is comfortable with. Like I said in our recent interview on The ROI Club, things usually take longer than you think. All in all, with NRP trading at a TTM free cashflow rate of 18%, I continue to believe it’s a bargain.

Mesabi Trust (MSB)

Last September’s Portfolio Update highlighted Mesabi Trust winning its litigation against Cleveland Cliffs and being awarded $71 million dollars. IN that piece, I commented that, even after a jump of 30%, the market hadn’t yet fully priced in the good news. With MSB up a further 31% since then, let’s take a look at the numbers as they stand today.

First, the chart below shows Mesabi’s cash balance at year end going back to 2011. It shows the Trust historically maintained cash of around $10 million. In 2022, the balance was increased substantially to hedge the uncertainty of Cleveland Cliffs idling the mine and the litigation that followed. The balance as of last October was $96 million after the addition of the awarded cash.

With the mine now producing at full capacity and the litigation concluded, I expect the cash balance to normalize. A workable estimate is the historical $10 million which theoretically would free up $86 million.

Another factor to consider is the normalization of Mesabi’s regular distribution.

The chart above plots Mesabi’s distributions along with the tons of iron ore produced on its land. While production has reached the pre-shutdown average of roughly 1 million tons per quarter, Mesabi’s most recent distribution of $0.39 is well below its quarterly average of $0.67.

Although the process is slow, I expect Mesabi to continue normalizing over the coming quarters. This could mean approximately $86 million of extraordinary distributions in addition to $35 million in annual distributions. The annual distribution alone would be a 9.3% yield on today’s market cap and the extraordinary distribution would be 23% of today’s market cap. While not the screaming deal it was a few months ago, Mesabi is still set to provide health returns for the foreseeable future.

Garrett Motion (GTX)

As we approach the end of today’s update, Garrett Motion again receives an honorable mention.

A press release on December 5th announced a changed in the company’s capital allocation. Moving forward, Garrett plans to return 75% of free cashflow to shareholders. Specifically, it’s targeting a $50 million regular dividend, which works out to $0.06 per quarter, as well as $250 million of common stock repurchases. This combines to 15.3% retuned to shareholders on the current market cap.

While we expected GTX to continue aggressively paying down debt for a while longer, we were nonetheless happy with the update.

Conclusion

With that, another episode and another year wraps up. It’s hard to believe we have been plugging away at this podcast/Substack thing for almost three years now. Thank you for making worth our while and we hope you get as much out of these posts as we get out of making them. See you all next year and in two weeks time.

Share this post