Welcome to Episode 119 of Special Situation Investing.

The topic of today’s show, Armanino Foods, is outside of the royalty, exchange and spin-off investments universe that has come to typify the write-ups that my co-host and I produce each week. In fact, it’s a surprisingly normal little manufacturing company with capex, active management, and all the other things that I try to avoid these days. On the other hand, though, I do own it and have for many many years, so I thought it might be an interesting thematic change to cover it today.

Armanino Foods

According to Armanino Foods own website, their story goes something like this:

The Armanino story begins in Italy’s Liguria region, the birthplace of pesto. In the wave of Italian emigration to the U.S. between 1880 and 1920, Mary Picetti and Guglielmo Armanino arrived in San Francisco, California, where the latitude, terrain and mild coastal climate reflect that of their homeland in Liguria.

They didn’t know each other at the time, but Mary and Guglielmo would eventually fall in love and settle into the farming community on San Francisco’s south side. From Liguria, Guglielmo brought his skill as a row-cropper, and Mary brought her basil pesto recipe.

Mary and Guglielmo’s son, William J. “Bill” Armanino, was interested in the new technology behind mass-produced convenience foods. How could Armanino farming play a part in the modern food industry? To answer that question, he took a job at Kraft Foods, where Armanino chives were soon freeze-dried and incorporated into Kraft sour cream. By the end of the 1960s, Bill had transformed the family business from local farm to national herb supplier.

The next decade held similarly exciting growth, as Bill introduced his mother’s pesto to the U.S, making Armanino the first company to sell classic Genovese pesto on the retail market. In fact, it would become the nation’s leading pesto supplier, turning an obscure Italian sauce into one of America’s favorite flavors.

Throughout the following years, the company continued to grow, diversifying the product line to include globally-inspired sauces, pastas, meatballs and more. Armanino foods can be found in grocery stores across North America and around the world.

Bill Armanino passed away in 2009, but left a legacy of food innovation, heritage and the highest standards of quality to the next generation of Armaninos. It’s a legacy of bold, exciting flavor and innovation that still guides the company today—and still plays a part in shaping the way the world thinks about cooking and eating.

Why I bought the stock

So how did Mr. Six Bravo no-capex-royalty-company guy come to own this very conventional micro-cap packaged food business? The answer is simple, it seemed like a good idea at the time. Well, maybe it’s a bit more complicated than that. You see, I, like you, have learned and grown as an investor over the years and I started my journey by investing heavily in consumer monopoly brands, with little to no debt, and plenty of room to grow. It’s a strategy that works well and one that I still invest in to this day as is evidenced by the fact that I still own Armanino Foods all these years later.

My fascination with special situation investing came later in my investing life and was in full swing when I started this podcast back in 2022. Since starting the podcast, both my co-host and I have begun to see value in royalty, exchange, brokerage and other inflation-protected industries but I still hold stocks dating back decades to a time when my toolkit included far less tools and the majority of my investments were in consumer monopolies. It was only recently when I heard Armanino Foods mentioned on a podcast that I was inspired to revisit the company and see how my original thesis was holding up. Until listening to that podcast, I’d never heard the name Armanino Foods uttered by another investor and considered it to be one of my more eclectic and off-the-beaten-path finds.

To give you a better understanding of the company, let’s go back to my original and rather simplistic investment thesis from all those years ago and review it step by step. Once that’s complete we can look at what’s changed over the ensuing years and how those changes make the ownership case even stronger today. I’m not sure I would buy the stock now if I didn’t already own it but, as my co-host can attest to, I’m very slow to sell anything I already own as long as the original thesis remains intact.

In the case of Armanino Foods, my original thesis was that it was a consumer monopoly (albeit on a small scale), with little to no debt, that consistently grew earnings, and that didn’t dilute shareholders. While it may not have been a reasonable comparison, I thought of it as my own little See’s Candies. When Buffett and Munger purchased See’s it was a small, regional chocolate company, it earned high returns on capital, it had room to grow, and it was reasonably priced.

Buffett and Munger often waxed eloquent on the topic of consumer brands and flavors and this was on my mind when I first purchased Armanino Foods. This is because Armanino produces multiple distinct food products which it then distributes to wholesalers, restaurants, and limited numbers of stores, and to the extent that end customers enjoy and demand their products, the middle men like restaurants will ensure that they have the product stocked to meet demand. Because of this, Armanino benefits from end customers demand for their branded flavors but doesn’t incur the added overhead and risk that come with running a restaurant or retail store directly. This is similar to See’s Candies in that See’s wasn’t running a low margin grocery store or restaurant but rather focused exclusively on a distinct flavor with end customer demand and a relatively low fixed-cost business model.

Next up in my original thesis was Armanino Foods limited use of debt. At the time of my initial investment the company was essentially debt free and had maintained a similar position for years. In my opinion, a debt free company is worth extra investor attention because its more robust and better equipped to weather the inevitable financial storms that come its way. I understand the positive effect that leverage can have on earnings and am willing to consider indebted companies under some circumstances but, by and large, I like the company to be debt free if possible.

In 2017, years after I made my initial investment in Armanino Foods, the company took on a relatively small loan of $3,500,000 to pay for a plant expansion and equipment modernization project. The project aimed at doubling the manufacturing capacity of the company in preparation for future demand. The loan was set to mature in 2022 but was paid off early in 2020. The project was completed on time and within the original budget and looks prescient in hindsight as new demand did materialize and the company secured the loans at historically low rates of 3.35% and 4.28%. The company’s aversion to debt, and responsible use of it when required, was and remains an appealing part of my original investment thesis.

The next part of my original thesis was the company’s ability to grow profits consistently year after year. While growth never exploded upward in any one year, it has been consistent, seeing operating income grow from $1 to $7 million between 2007 and 2021. Interestingly, the company’s revenue only grew from $19 million to $44 million over the same period, which demonstrates Armanino Food’s ability to consistently drive costs down and increase the efficiency of their operations. AltaRocks January 3, 2022 Value Investors Club write-up captures the company’s increasing efficiency in a different way by looking at revenue per full time employee which has also grown steadily over the years from below $800k in 2012 to nearly $1.2 million in 2021.

The last item included in my original thesis was the company’s commitment not to dilute shareholders. The company repurchases shares in 2011 and 2012 bringing the total shares outstanding down from 34,000,000 to 32,065,645 where the share count remains today. It would seem that internal growth and a steadily increasing dividend is the priority of management over stock buybacks but keeping the share count steady remains one of the key attributes that drew me into the investment in the first place.

Recent Developments

Moving from my original thesis to developments that have transpired since then, the phantom stock incentive plan further supports management’s commitment to avoid shareholder dilution. The Phantom Stock Incentive Plan was approved by the board of directors in March of 2019 and it allows for the issuance of up to 1,000,000 shares of phantom stock which expire ten years after the date of grant. The key benefit to shareholders is that the phantom stock acts as a tracker or proxy of the company’s actual stock but pays out as cash rather than shares making it non-dilutive.

Further aligning management and shareholders is the fact that phantom stock issuance is recorded as an expense, unlike traditional stock options, which are not. Because options are a form of compensation, they should be carried as an expense just like wages and bonuses are, but Armanino Foods phantom stock incentive plan is the first time I’ve seen it done. I’m sure that similar plans exist at other companies, but in my broad reading of corporate reports I’ve never come across a similar plan and I admire the company’s leadership for implementing it.

Another new development since my original purchase is CEO Timothy Anderson. Tim took the reigns from CEO Edmond Pera in 2020. Mr. Pera was the company’s second CEO who assumed the position following the passing of Armanino Foods founding CEO Bill Armanino in 2009. That the company has continued to achieve record results after switching CEOs in 2020 is a testament to Tim Anderson’s leadership. 2020 was a tumultuous year to run a company let alone take on a new CEO position and leadership changeovers that year didn’t fair well in several other public companies that I can think of. Disney comes to mind as a prime example where the 2020 CEO swap was too much change for the company to process during an already challenging time.

When Mr. Anderson began his CEO tenure at Armanino Foods he brought with him an extensive track record in growing branded packaged food companies. Most notably, he’s reported to have more than doubled the size of Challenge Dairy’s butter brand leading it to become the number two national brand that is available in all 50 states. His ability to grow an already successful brand may be the most important skill that he brings to the table as the new CEO and it would seem that he’s already pursuing a similar strategy in his new position.

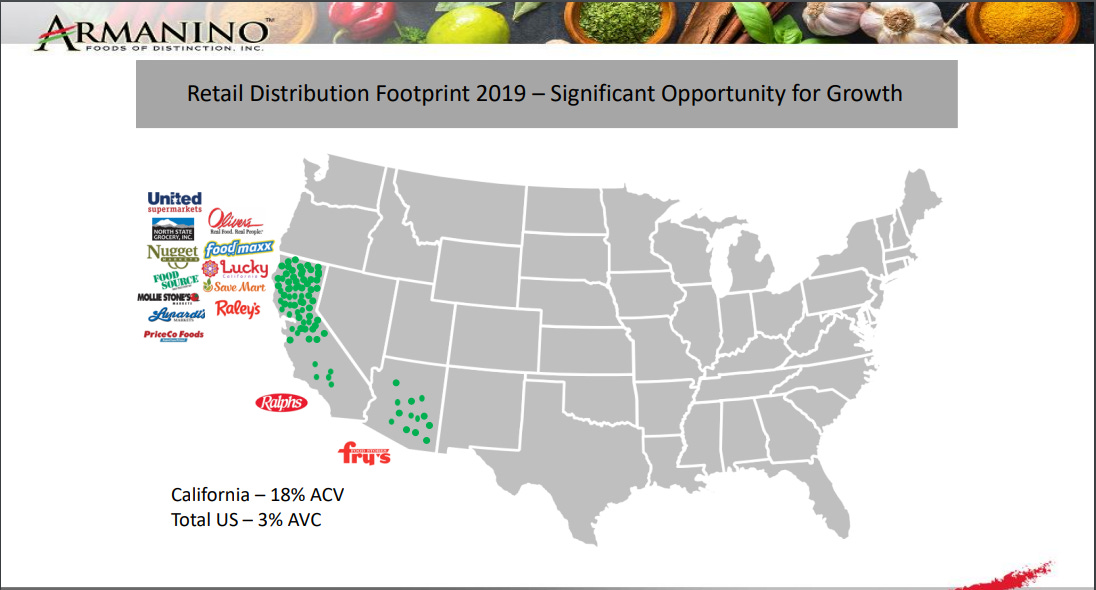

Prior to Anderson’s time as CEO Armanino Foods was essentially a regional brand focused on the southwestern United states with limited availability in grocery stores outside of California. Since taking over, however, he’s rapidly expanded the number of stores which carry their products and appears to be growing the brand in the same way he grew the butter brand at Challenge Dairy. The following slides from a recent investor presentation show the increased availability in grocery stores that has taken place since Mr. Anderson took over in 2020.

Future Prospects

With that overview of the company complete, we’re left to ask ourselves where Armanino Foods is headed in the years to come? The bear case would suggest shrinking profit margins from inflation-induced rising fixed costs that eat into the profits of a packaged food that only has so much pricing power in the end market. If management can’t bring in new customers or increase prices faster than costs increase then Amanino’s margins will shrink and investors will suffer.

If on the other hand, Armanino can grow the brand through increased exposure in national grocery stores, as it’s already working to do, then the company may continue to thrive. On top of brand growth, the company must also continue to increase the efficiency of its operations so that fixed costs do not erode profit margins. Assuming Armanino Foods can accomplish both of these tasks then returns for investors could come in one or more of the following ways.

Dividends - Increased dividends could push the stock price up while simultaneously increasing returns to shareholders.

Share buybacks - While the company hasn’t engaged in buyback in over a decade, the practice did significantly boost shareholder returns at the time and could be implemented again if management has enough cash available.

Buyout - The brand could grow to the point where it’s an appealing buyout target for a larger branded products company. Many small private brands have been scooped up by the Kellogs and Kraft Heinz of the world in recent years as those companies look to purchase growth that is difficult to generate internally at the massive scale of their operations.

Over the last two decades Armanino Food’s has outperformed the S&P 500 compounding at more the a 16% CAGR compared to just over 7% for the index with dividends reinvested. Whether the company can continue to out perform in the coming decades, however, remains to be seen. Personally, I’m not selling so long as the original thesis remains intact and to date the thesis has not only held up but improved in a several key ways.

Conclusion

In conclusion, Armanino Foods is a solid company to own if you imagine that your family wholly owned the business and depended on it for their livelihood. This is a construct I often use in my own investing. Would I feel comfortable if my family’s fortune were completely tied up in this one business and I was no longer around to advise them? The perfect company doesn’t exist and so you can’t be overly critical of any one investment but that question will reveal a company’s weak points if you examine it through the lens of long-term and total ownership. While Armanino Foods certainly has some weak points I wouldn’t be overly concerned if it were the family business either and I’m comfortable retaining it in the portfolio for now. As always, we welcome your thoughts and insights on the company and its prospects in the comments.

One more thing before we wrap up for the week. For more than a year now my co-host and I have posted a write-up each week and we’ve learned a great deal in the process. For the foreseeable future, however, we’re going to slow down to one post every other week. We think this will give us more time to do indepth research into new ideas without the pressure that comes with putting something out every Saturday morning. This is a trial run and we can always switch back to once a week if the quality of our research in not markedly improved by the change. As always, we thank you all for your support and we will be back again in two weeks time with another short and actionable investment write-up.

Share this post