Welcome to Episode 82 of Special Situation Investing.

In what could now be considered old news, on June 3rd, the President of the United States signed legislation raising the country’s debt limit and, according to media and political pundits, averting national calamity.

Included in the legislation was a directive clearing the way for the completion of the long delayed Mountain Valley Pipeline (MPV). Starting in Northwest West Virginia, the three hundred and three mile long pipeline is projected to transport two billion cubic feet per day of natural gas from the Utica and Marcellus shale basins to the markets in the mid and south Atlantic US regions. Despite its potential benefits, the project was plagued by delays from policy makers and environmentalists since its first application for construction was filed in 2015. Most recently, it languished for months, ninety-four percent complete, while activists fought over its fate. But finally, with the stroke of a pen, all remaining obstacles were removed. The text of the recent legislation directs the Secretary of the Army to:

issue all permits or verifications necessary to complete the construction of MVP across the waters of the United States, and to allow for the operation and maintenance MPV.

While environmentalists fail to contain their outrage, the government now claims the completion of MVP is a national priority. As we believe it probably should be.

While we applaud the greenlighting of the MVP project, our attention has been thousands of miles away on the other side of the continent, watching another pipeline near completion.

We’re interested in Canada’s soon-to-be-completed Trans Mountain Pipeline Expansion.

The Pipeline of Interest

The Trans Mountain Pipeline (TMPL) begins in Edmonton, the capitol city of the Canadian province of Alberta. Since Alberta is the heart of Canada’s oil production, there are dozens of pipelines leading in and out of the province. But TMPL is unique as it’s the only pipeline to link the Canadian oil sands to the West Coast of North America. We’ll get into why we think it’s so important later, but first, a little history.

The Trans Mountain Pipeline Company was granted a charter by the Canadian government in 1951 and construction on TMPL began a year later.

As its name suggests, the Trans Mountain Pipeline crosses the Rocky Mountains traversing some of the most rugged terrain on the continent. In spite of the challenges, the project’s planning and construction was completed in only two and a half years and in 1953 the first oil was delivered to the Burnaby Terminal in British Columbia.

By 1956, the pipeline was flowing at a capacity of 250,000 barrels per day. Also that year, the Trans Mountain Puget Sound Pipeline was finished which connected TMPL to multiple delivery points south of the Canadian border in Washington State.

Ownership of the pipeline has changed hands multiple times over the years. In 1994, the Trans Mountain Pipeline Company was acquired by BC Gas, which later changed its name to Terasen Pipelines. Kinder Morgan later acquired Terasen in 2005, and remained the owner until it sold out to the Canadian government in 2018.

The pipeline’s first expansion, which took place under Kinder Morgan’s watch, was the Anchor Loop Project. It was completed in 2008 and increased the flow capacity to 300,000 barrels per day which remains its current capacity.

With one expansion complete, Kinder Morgan proposed the Trans Mountain Expansion in 2012. This project, which is the focus of today’s episode, received commitments from 13 customers who signed long-term agreements supporting the planned increase in capacity up to 890,000 barrels per day. After multiple review processes aimed at restoring public trust and garnering support, the Canadian government gave its initial approval for the project in 2016.

In 2018, a trade dispute broke out between the provincial governments of Alberta and British Columbia (BC). The BC government proposed a temporary ban on increased shipments of oil from Alberta. In a classic tit for tat, Alberta called the ban unconstitutional and threatened its own ban of wine coming from BC and then escalated by threating to cut off all oil going into BC.

Caught in the middle of a political dispute, Kinder Morgan threatened to abandon the expansion project if no resolution was reached by the end of May, 2018. As a result, Prime Minister Trudeau cut short an international trip to broker a deal between the two provinces, which ultimately concluded with the Canadian Federal government announcing it would buy TMPL from Kinder Morgan for $4.5 billion.

Fast forward to May 30th of this year, the Trans Mountain Corporation (still owned by the Canadian government) released its latest quarterly report which estimated that, as of 31 March, the TMPL Expansion Project was eighty-two percent complete. Full completion is expected by the end of 2023 and first product delivery is expected in the first quarter of 2024. After which time, the Canadian Federal government plans to sell the pipeline.

The Situation

This brings us to the current day and the current opportunity. If the project remains on track, the amount of oil Canada will be able to export to the world will nearly triple next year from 300,000 to 890,000 barrels per day. We believe there are three reasons this development could prove a major boon for Canadian oil producers.

Increased export capability will increase the price of Canadian crude.

Remember that TMPL is the only Canadian pipeline to reach the West Coast. The majority of Canadian oil is exported through pipelines that flow south into the United States, most of which terminate at the Gulf of Mexico. This is logical for a couple reasons, namely, the US is a large, coinvent customer, and building greater export capacity via West Coast ports would require building more pipelines through the Rocky Mountains. It’s therefore understandable that most Canadian oil is sold into the United States.

But picture the situation this creates for Canadian oil producers: they have one main customer, that one customer is one of the world’s largest oil producers, and the oil that customer produces is a higher quality product. That setup doesn’t leave the Canadian producers much pull at the bargaining table.

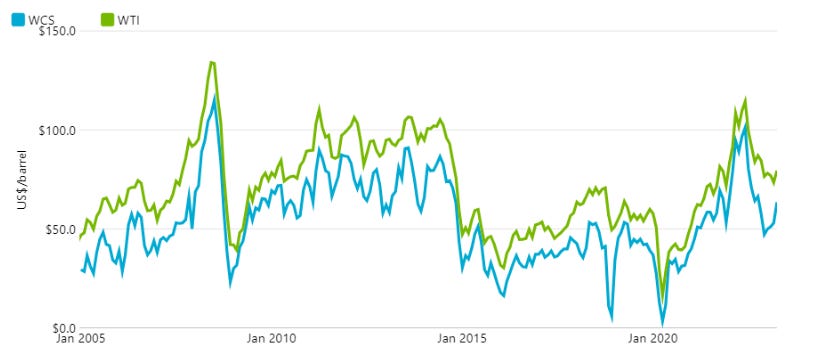

This disadvantageous setup is the main reason Canada’s crude oil benchmark, Western Canadian Select (WCS), constantly trades at a discount to other benchmarks such as WTI and Brent. For sure, there are other factors such as the lower quality of the oil extracted from the Canadian oil sands, but it’s commonly believed the lack of a multiplicity of customers for Canadian crude plays a dominate role. The chart below illustrates how the discount of WCS to WTI, currently at 28%, has persisted for decades.

We believe if more Canadian oil were to reach the West Coast, and therefore more customers, particularly in East Asia, it’s likely the price discount would lessen if not disappear.

More pipeline infrastructure will allow Canadian producers to sell more oil.

With its current pipeline infrastructure, Canada operates at or near its full capacity. In 2022 numbers, Canada totaled a pipeline export capacity of approximately 4 million barrels per day. While in the same year, in excess of 4.2 million barrels per day of oil were available for export via pipelines.

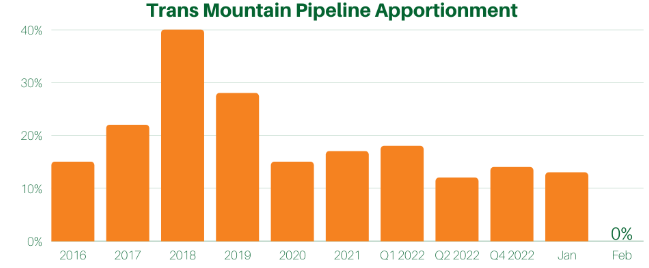

Take TMPL as an example. For at least the last six years there has always been excess demand for its available capacity. We know because this data is captured in what’s called pipeline apportionment. It works this way. Each month, customers wishing to ship product through the pipeline submit request to the Trans Mountain Corporation. Based on those requests, and taking into account the type of product, pipeline maintenance, and carry-over flows from the prior month, a monthly capacity is calculated. Requests in excess of this calculated capacity is called apportionment.

As the chart above shows, TMPL apportionment has averaged between 15% and 40% on an annual basis since 2016. Clearly, shippers want to transport more product through TMPL than its current capacity allows. When the TMPL expansion is completed there will be excess pipeline capacity allowing producers to ship more oil adding to their revenues. Without a doubt, the economics of transporting Canadian crude will change.

Greater competition among pipelines will decrease toll costs to producers.

Operating at or near full pipeline infrastructure capacity has allowed pipeline companies to not worry that a competing pipeline may undercut their toll prices. With capacity from the TMPL expansion coming online next year, pipeline operators will likely be forced to compete for customers by lowering prices. In fact, they already have.

Earlier this month, Trans Mountain Corp applied to regulators for the rights to levee tolls on its expansion pipeline. In the application, the company indicated a target toll price of $8 to $9 which is slightly lower than the current average toll. And Trans Mountain Corp is not the only company lowering prices. A month ago, Enbridge, the operator of Canada’s largest pipeline, signed a new deal with shippers that decreased its toll rate.

So we’ll have to see how supply and demand level out, but it appears that an increase in pipeline capacity has the potential to spark greater competition among pipeline companies, leading to lower costs for producers. That is, at least while surplus pipeline capacity persists.

So to recap, the three reasons we believe the completion of the Trans Mountain Expansion Project could be a boon for Canadian oil producers are: 1) an increase in the price of Canadian crude, 2) the ability to sell more oil, and 3) lower shipping costs.

How to Play It

We believe this positive, developing situation will act as an increased tailwind in the sails of Canadian oil producers. To date we haven’t singled out one producer over any others that we believe it will benefit more. In fact, and here’s where we thrown a curve ball, we believe possibly best way to play the situation is through a royalty company, because what’s good for oil producers will also be good for the owners of the underlying royalties. For those subscribers and listeners who have been with us for a while, that comment will be come as no surprise as we are very vocal about our affinity for hard asset, asset-light business models such as royalties.

While we don’t have time to dive into it today, just to whet your appetite, there is a royalty company with millions of royalty acres in Alberta and it stands to benefit greatly from any increase in revenues that accrue to producers. Perhaps we’ll write a deeper dive on that company for a follow-on episode.

But with that, we’ll wrap up today’s show.

Thanks to all of you who have been commenting, sharing, and liking our content. Your engagement is the most encouraging way you can support the time and effort we put into these pieces each and every week. We hope you are enjoying the content and learning as much by listening as we are through creating them.

We’ll see you all next Saturday on the next episode.

A must-watch from the past week

Share this post