Welcome to Episode 123 of Special Situation Investing.

Recently, my co-host asked one of our favorite investors why he avoided coal companies. Was it a conscious decision or just the way things had worked out given the opportunities available to him? His response was, in essence, that he wanted to avoid the hostile regulatory environment that surrounded the coal industry. He said that it was a fight he just didn’t want to engage in.

Hearing the legitimate concerns of a successful investor, who you have the utmost respect for, about an industry that you yourself are invested in, should give any intelligent person a moment of pause. I know it did for me.

One of the companies I like best these days is Natural Resource Partners (NRP). It’s a royalty company with extensive land ownership in the U.S. who’s primary source of revenue is coal. And while eliminating coal use tomorrow wouldn’t end the company, it would most certainly lower its return prospects for the foreseeable future. We wrote about NRP in Episodes 64 and 68 and we encourage you to review those write-ups if you aren’t already familiar with the business as it will make the rest of this discussion easier to understand.

As I wrestled with the future of coal question, I realized I was really concerned with the future prospects of NRP and not the coal industry itself. Whether or not global energy production is able to divorce itself from coal in the next decade, two decades, or ever, is a question that’s too big for me to tackle. I have my doubts about the decarbonization timeline proposed by ESG advocates (which I discussed in Episode 87 of the podcast)but those views may turn out to be wrong especially given my lack of energy sector expertise. No. In order to answer my question about NRP’s future, I needed to uncover whether or not it could sustain even the most rapid coal use drawdown proposed by climate advocates and still emerge as a great company to invest in. It was as simple as that: assume the best case for decarbonizing the world—which would be the worst case for NRP’s short term profitability—and see how the company’s stock returns would be effected.

Researching coal from this point of view led me to the International Energy Administration’s (IEA) Coal 2023 Analysis and Forecast to 2026. The IEA report advocates for the reduction of coal in support of global decarbonization efforts in a fact-based and balanced way. The report makes certain projections—which like all projections tell you more about the point of view of the person making the projection than they do about what will actually happen in the future—which could be useful in “stress testing” my NRP investing thesis.

Not All Coal is Equal

One of the first things you learn from even the most cursory investigation of the coal industry is that not all coal is equal. Coal comes in varying degrees of quality and energy density and those factors effect what the coal is used for. Broadly speaking, industry uses both thermal and metallurgical coal. Thermal coal is used for power generation and metallurgical, or “met,” coal is used in industrial processes like steel manufacturing.

On a per-ton-basis, met coal typically commands a higher price than does thermal coal. This means that a decline in the use of just one category will effect NRP’s profits disproportionally based on which type of coal it sells more of and what price that type commands in the market. The chart below displays the per ton price of met and thermal coal from 1990 through 2018.

Annual met and thermal coal production from NRP properties is split nearly 50/50 over the last several years with only slightly more thermal being produced than met. Given that met coal sells for a higher price than does thermal coal, NRP’s earnings are generated more by the met coal business even though thermal coal production is slightly higher than met production. NRP’s total coal tonnage split by met and thermal over the last three years can be seen in the following table that was sourced from its 2023 annual report.

Met and thermal coal use will, according to decarbonization advocates, experience separate decline curves over the next several decades and this, in addition to their price differential, is why it’s best to discuss them separately. Thermal coal should experience the quickest and the most rapid decline as the base load power that it provides is replaced by nuclear, natural gas, and renewables. This decline will be slowed to some extent as China, India and other developing nations continue to increase their coal use through 2030 but even with their added consumption, the move away from thermal coal is thought to be inevitable.

The future of met coal is not as clear as that of thermal. Met coal is a key ingredient in the steel and concrete manufacturing process and doesn’t have a promising substitute on the horizon. Add to that the renewable energy infrastructure projects set to begin in the United States, the European Union, and China and it becomes clear that the demand for met coal might actually increase over the near term as the world rebuilds its energy infrastructure in the coming decades.

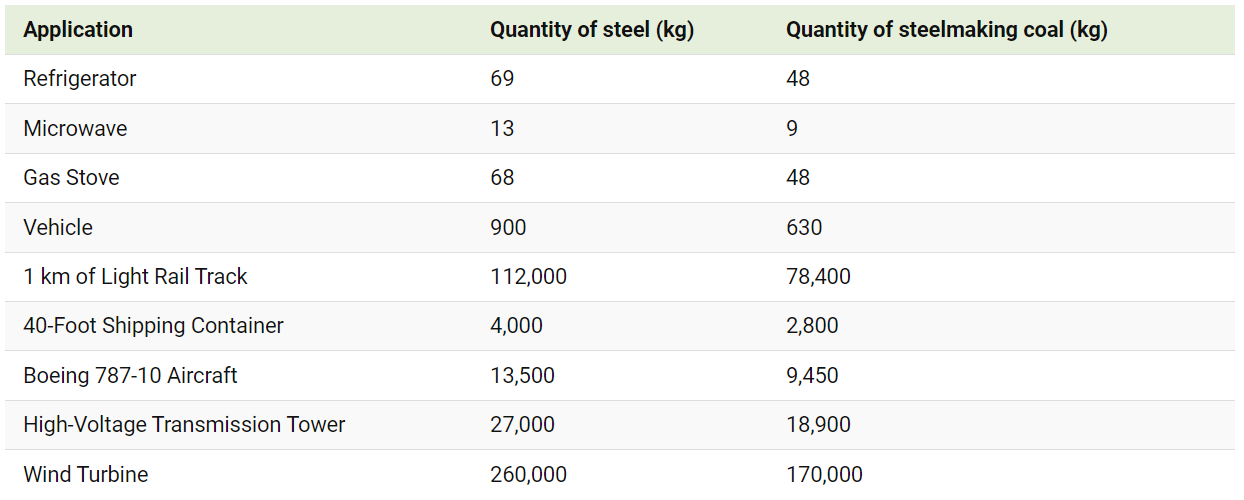

According to visualcapitalist.com Understanding Global Demand for Steel Making Coal:

Steel is the most commonly used metal and fulfills a variety of structural and construction needs, along with being an essential material for the production of vehicles, mechanical equipment, and domestic appliances. Clean and renewable technologies also require steel to build wind turbines, solar panels, tidal power systems and bioenergy infrastructure. While some kinds of steel can be made using recycled metal, roughly 72% of global steel production relies on steelmaking coal and certain higher grades of steel can only be made using the ingredient.

The following chart from the same article lists the steel required for a variety of end products along with the coal required to manufacture that steel.

Understanding coal types, uses, and future prospects allows us to understand the data depicted in the previously mentioned International Energy Administration’s (IEA) Coal 2023 Analysis and Forecast to 2026 report. The report projects a -5.6% CAGR for thermal coal exports globally and a -6.8% CAGR for the U, S. market specifically between now and 2026. Met coal exports are projected to grow globally by 0.5% annually and -0.6% for the US market over the same period.

The decline in thermal coal and the steady market for met make sense given the factors already discussed but even if we assume that the IEA projections are accurate they’re likely to have a negligible impact on NRP’s profitability over the next three years. This is because NRP’s largest source of revenue, met coal, is slated for nearly flat production levels while thermal coal, its second largest source of mineral rights revenue, is only forecast to decline at a -6.8% CAGR.

In fact, even though production of thermal and met coal are nearly even by weight thermal coal only accounts for 25% of NRP mineral rights revenue with 50% coming from met coal and the remaining 25% sourced from smaller royalty streams such as oil and gas, aggregates, carbon neutral initiatives and others. Given all of the variables involved in the company’s final profitability from the price of coal, to production levels on its properties, to the strength of the U.S. dollar, the near-term coal use forecast is hardly cause for alarm.

In fact, the short-term driver of NRP-s returns is its debt repayment schedule and not the future of the coal industry. This is because, as of December 2023, the company has only $156 million of total debt remaining of the original $1.5 billion that it set out to repay in 2015. Because debt repayment has been the priority over the last 8 years, the company has deliberately limited its dividend payout. The idea behind the dividend policy was to offer a dividend that was just high enough for common unit holders to pay any tax obligation generated by the partnership while using any excess cash flow for debt repayment.

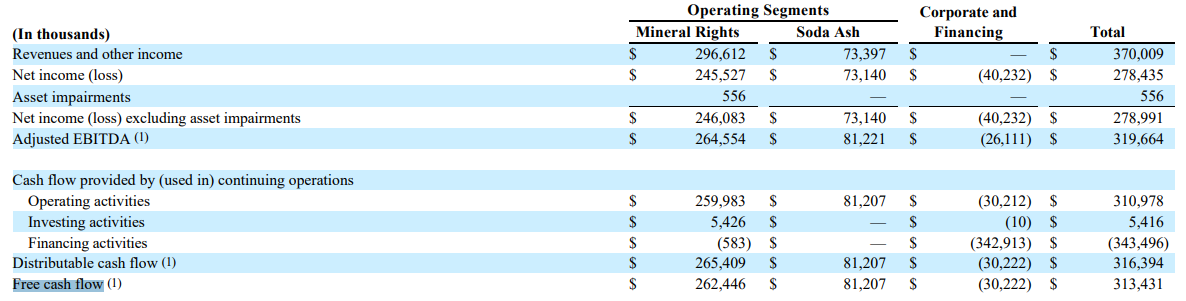

This can be seen in NRP’s 2023 annual report. NRP reported $313 million in free cash flow but paid a distribution to common unit holders of just $69 million. Once NRP completes its debt repayment plan, it will have little use for the free cash flow from its royalty properties other than share buybacks or increased distributions to unit holders, both of which should benefit owners of the company. In essence, NRP over the next 12 to 36 months is more of a special situation investment than a bet on the future of coal.

We have established that global coal use is projected to remain steady through 2026 but, if ESG advocate projections are accurate, then coal use will rapidly decline from 2026 through 2050. Because met and thermal coal have separate end markets, demand profiles, and technological alternatives we will analyze their 2026-2050 projections independently.

According to Global Energy Transformation: A Roadmap to 2050 coal’s share of global electricity generation per terawatt hour will shrink from present levels to a greatly reduced but not quite zero number by 2050. Because thermal coal used for power generation makes up just 25% of NRP’s mineral rights revenue then we can conservatively assume that thermal coal will contribute almost nothing to NRP’s free cash flow 25 years from now.

Reduction of met coal use, however, is a more challenging prospect for net zero advocates than is thermal coal because the proposed replacement technologies aren’t fully proven or deployed at this point. Steel produced from hydrogen rather than coal is one of the proposed replacement technologies but it has yet to be fully implemented or scaled even though it is often included as a viable replacement technology in net zero projections.

According to a Coal to Clean Energy Policy Report by EMBER:

The latest IEA World Energy Outlook’s 1.5-degree compliant Net Zero Emissions (NZE) scenario requires drops in coking coal usage of 26% by 2030 and 83% by 2050 versus today’s level. If climate ambition falls short, metallurgical coal use might not fall as quickly. The IEA’s assessment of governments’ announced pledges forecasts a moderate 11% fall in coking coal use by 2030 and a 56% drop by 2050. How much coking coal will be used in 2030 will be critically important for the steel industry’s climate goals and the Global Methane Pledge.

Given that met coal revenue accounts for 50% of NRP’s mineral rights cash flow, we can safely assume that under current projections met coal’s share of mineral rights cash flow will fall by 25% from current levels through 2050. It’s worth reiterating that NRP’s total cash flow is sourced from both the soda ash segment, which constitutes about 25% of the companies total free cash flow and the mineral rights segment which accounts for the remaining 75%. The reduction in coal revenues mentioned above represent a portion of the mineral rights 75% of earnings.

If the coal reductions just covered took place this year it would reduce NRP’s total cash flow by approximately 40%. This is because NRP would still have 50% of the met coal revenue, all of the “other” mineral rights royalties revenue, and the soda ash revenue all still producing cash flow for the company.

The Potential of Carbon Sequestration

This reduction in earnings, however, doesn’t include the potential growth in earnings of NRP’s carbon capture utilization and storage (CCUS) segment. Significant global growth in CCUS is included in almost all net zero 2050 projections and is particularly critical to carbon neutrality in the steel business where capture may be the only way to achieve net zero emissions.

According to the World Economic Forum:

While innovative, breakthrough technologies may drastically cut steel production emissions, carbon capture, utilization and storage (CCUS) technology allows residual emissions and emissions from traditional blast furnace processes to be captured, particularly while deeply decarbonizing solutions remain unavailable at scale due to high-cost premiums. CCUS is also a key decarbonization lever in other sectors, such as cement and aluminum production.

On the topic of carbon capture technologies, NRP’s most recent investor presentation had the following to say:

Given that reduction of CO2 emissions is the primary reason for the world to move away from coal, and that CCUS is a central part of that strategy, it may be the case that CCUS revenue will eventually replace much of the lost coal royalty revenue. In this scenario, NRP’s royalty revenue may not be overly effected by decreased coal use.

In fact, NRP’s primary revenue drivers will continue to be commodity prices themselves rather than the volume of material produced. The last few years have shown this to be true as revenue sky rocketed during the historic 2021-2023 commodity price rally. No similar spike in revenue could be generated by increases in product volume alone due to physical limits on production capacity. The price of coal, soda ash, sequestered carbon, and other commodities will have more impact on NRP’s free cash flow in the decades to come than will the forecasted decreases in coal volumes over the same time period.

Given the current regulatory hostility toward coal and its anticipated decline in the coming decades, I would not put my money into a pure play coal business. Putting all of your eggs in one basket is never advisable even if you watch that basket very closely. In the case of NRP, however, the company is diversified over the soda ash, coal, and several other small scale commodity businesses and is not a pure coal company. Additionally, the primary business that its management team is trying to grow, carbon sequestration, is one that it’s uniquely set up to profit from and one that must expand if the world is to decarbonize.

NRP is uniquely set up for carbon sequestration because it owns large contiguous tracts of land with the correct geology and without a split mineral or water interest on the property. Carbon capture is best implemented on large plots of land because it can then be carried out without generating noise complaints or other disputes between neighboring property owners. Owning the land fee simple is also best as approval for sequestration can be granted from a single owner without requiring the consent of mineral, water, and other interest owners.

Conclusion

While coal does bring in most of NRP’s revenue today, the company has at least two drivers in its favor that could allow it to grow long into the future. Both drivers have already been covered but to recap as we summarize they are the near-term debt payoff and carbon sequestration. The debt payoff will dramatically increase the capital available to shareholders for buybacks and dividends, while carbon sequestration will ramp up just as the coal business declines allowing the company to maintain a steady stream of royalty payments post coal. While I cannot predict the future of the coal industry, and won’t be betting the farm on my own forecasts, I am willing to put some of my capital into NRP for all of the reasons discussed in today’s write-up.

With that we wrap up another edition of the show. We hope you found it interesting and learned something alongside us. We’ll be back in two weeks with another investing write-up. Thanks again.

Share this post