Welcome to Episode 104 of Special Situation Investing.

The consensus says coal is dead. We, on the other hand, believe coal investments will outperform.

Our curiosity behind this conviction led to multiple coal company write-ups throughout 2023. In February, we published our first piece of many on Natural Resource Partners. In March, we did a short write-up on Teck Resources. In June, we put out a piece called The Cannibal Coal Company on CONSOL Energy and in August we wrote-up Alpha Metallurgical Resources in the piece A Buyback Monster. Most recently, we did a piece on the little-know coal company, Beaver Coal.

Interest in CONSOL Energy (CEIX) and Alpha Metallurgical Resources (AMR) specifically was peaked because of large positions initiated by two investors we respect—David Einhorn purchased of CONSOL and Mohnish Pabrai bought both CONSOL and Alpha. After digging in for ourselves, we argued both companies had upside potential based on the combo of high cash flows and aggressive share repurchases. For example, about CONSOL, we wrote:

[It] could buy back somewhere between 23% and 34% of the company’s market cap over the next year. This in turn…could lead to a return of 30% to 51%. So as we can see, CONSOL is set up to potentially literally force a solid return simply by allocating its strong FCF to share buybacks.

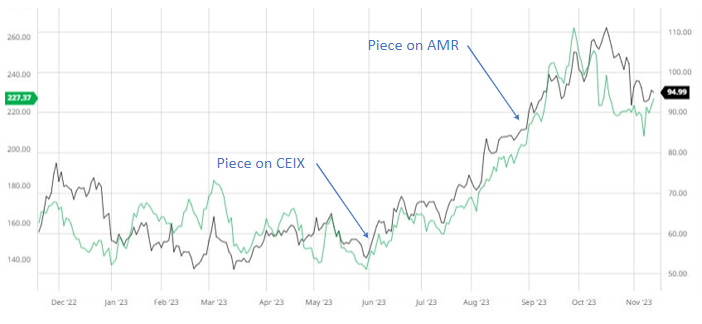

Both securities are up about 50% over the last six months after commencing their respective buyback plans as shown in the chart below.

In this piece we’ll provide an update on the buyback programs of the coal companies in Pabrai’s portfolio—two old and one new—and then share an insight into his decision to buy.

The Update

As 13F filings trickled in over the last couple weeks, we were curious to see how these two investors adjusted their coal positions in Q3. The results were mixed.

Possibly reacting to CONSOL’s price rise, Einhorn trimmed his position approximately 15%, but the company remains his second largest position at 14% with a value of $250 million.

On the other hand, Pabrai increased his stakes in CONSOL and Alpha and initiated a new position in Arch Resources (ARCH).

Note that even though Pabrai doubled his holdings in CONSOL and only increased his position in Alpha by 22%, the latter company remains his largest position at 68%. CONSOL takes second place at approximately 25% of his portfolio and his new position in ARCH is only 8%. Out of all the companies on the U.S. market, it still fascinates us that this savvy investor only found three coal companies worth taking a position in.

While 13F’s don’t necessarily represent current holdings, it is fascinating to see Pabrai buck the consensus now for two quarters. It appears he still believes these dirty coal companies represent an intriguing risk-to-reward probability. In our previous pieces on Alpha and CONSOL, we described them as uber cannibals—companies that are aggressively buying back their own shares. A review of the duo’s quarterly reports confirms they have lived up to the name.

Alpha Metallurgical Resources

Despite the negative impact over the last quarter of a mechanical failure at its loading terminal, Alpha made impressive progress on its repurchase program. It bought back 545,000 shares, or just over 4% of its market cap, at a cost of $102 million. This brings Alpha’s total repurchases since the inception of the program in March 2022 to $940 million. Something worth noting is that Alpha’s Q3 dividend will be its last and this should slightly add to the amount of cash flow available for buybacks in the future. The company’s repurchase program authorization was increased by $300 million to a total of $1.5 billion, of which approximately $560 million remains available for further repurchases.

If Alpha continues allocating $102 million per quarter to buybacks over the next year, it could repurchase $404 million worth or 13% of its current market cap. All else remaining constant, that would lead to a 15% return.

CONSOL Energy

CONSOL also had a solid quarter producing $120 million in free cash flow. With 77% of this free cash flow, the company repurchased 976,000 shares of its common stock for $93 million, totaling 3% of its market cap. Over the first three quarters of 2023, the company repurchased 4.1 million shares of its common stock for $292 million which equates to 13% of its current market cap (annualized).

CONSOL also paid down $24 million in debt in Q3 and, as a result, reached its goal of $200 million in gross debt. Year-to-date it had allocated $183 million to debt repayment. It’s now likely more free cash flow will be allocated to buybacks in the future. In fact, the CEO said as much in the quarterly conference call. As such, we expect buybacks to pick up steam in the next quarters.

If CONSOL continues to allocate what it put towards repurchases and debt repayment in Q3 ($93 million plus $24 million) over the next year, it could buyback 15% of its current market cap. All else remaining constant, that would lead to a 18% return.

Arch Resources

The new company in Pabrai’s portfolio is Arch Resources. It’s a coal producer based in the United States with a setup and investment thesis similar to the two other companies. As of this quarter, Arch is following a new capital allocation plan which targets returning 25% of the prior quarter’s discretionary cash flow via a dividend and directing the remaining discretionary cash flow to share repurchases or capital preservation. The company had this to say about its capital allocation in its latest 10Q:

During the quarter just ended [Q3], the company deployed $28.2 million to repurchase 215,551 shares at an average price of $130.83 per share. In total, Arch has now used common stock and convertible notes repurchases to manage and reduce potential dilution by approximately 4.3 million shares. Arch ended Q3 with 18.8 million shares outstanding on a fully diluted basis.

In keeping with its capital return formula, the board has declared a total quarterly cash dividend of $21.6 million, or $1.13 per share, which is equivalent to 25 percent of Arch’s third quarter discretionary cash flow. The December dividend—which includes a fixed component of $0.25 per share and a variable component of $0.88 per share—is payable on December 15, 2023, to stockholders of record on November 30, 2023.

Arch has now deployed a total of $1,208.2 million under its capital return program since its relaunch 20 months ago—inclusive of the just‐declared December dividend—including $661.8 million, or $35.77 per share, in dividends and $546.4 million in common stock and convertible notes repurchases. Since the second quarter of 2017…Arch has now deployed a total of more than $2.1 billion under its capital return program. As of September 30, 2023, Arch had $220.7 million of remaining authorization under its existing $500 million share repurchase program.

This excerpt reveals Arch is pivoting to buybacks as its preferred method of shareholder returns. This is logical for a company trading at a low single digit PE ratio. But the company also appears to be an outlier among the three as it plans to maintain a dividend payout of 25% of discretionary cash flow.

To provide a comparison to Alpha and CONSOL, if all of Arch’s discretionary cash flow had been applied to share repurchases, and the Q3 number was annualized, the company could buyback 12% of its current market cap. All else remaining constant, this would lead to a 14% return.

While these hypothetical returns through brute force of buybacks alone are solid, they aren’t as impressive as they once were. Back when we wrote out first piece on CONSOL, a similar calculation projected the company could repurchase 23% to 34% of its market cap. But these companies would still meet the criteria to be on the uber cannibal list Pabrai maintains on his website. But as we recently found out, the companies uber cannibal status is not precisely why he’s buying them. For him, it’s all about the cash flows.

Why Pabrai is Buying

Ever since Pabrai’s Q2 13F revealed his positions in Alpha and CONSOL, we’ve listened to every interview he’s done since hoping to hear him explain his rationale behind his purchases. It took a while but we found it.

When a guest on the Meb Faber Show podcast, Pabrai explains, through a lengthy but educational story, why he liked these coal companies. He compares the setup in these stocks to a similar situation years ago. The precise information we are interested in is at the very end, but we included the entire story for its entertainment and educational content. Pabrai explained:

The thing is that what I have always found interesting is the anomalies. For example, I remember in 2004, there was a steel company based in Canada called IPSCO. IPSCO had no debt. It had $15 a share in cash, and it had given guidance that the next two years' earnings were going to be $15 a share each for the next two years. There were $30 earnings coming in, and the stock was at $42.

The reason they gave the guidance was that they used to make these tubular steel pipes where they had contracts with these pipelines where they wanted to deliver. The pipelines had given them purchase orders, and so they were going to deliver these pipes, and the cash flows were guaranteed. It's not like they were giving guidance based on future sales to be made. These were sales that had already been made. I said, “Okay, I don't know what will happen after two years, but I know that after two years, there'll be $45 of cash on the balance sheet, no debt, and the stock price currently is $42.” I said, “I just want to see what the stock price is two years from now. I want to see what Mr. Market does with this.” I just bought it based on that notion.

A year later, the company announced that we had one more year of visibility, and we had another $15 a share in earnings for one more year. Now the stock is at about $70 or $80. It's gone up a bit, It's a steel company, it's a very cyclical business. Then it starts drifting close to $90, and I'm thinking of taking it off. As I said, double in 15 months is good, so let's move on. I woke up one morning and the stock was at $157 and some Swedish company offered to buy them at $160. About five minutes after that, I downloaded the stock. I said, “We don't need to wait for the last $3. We're done.”

Recently, the two stocks I found in the US, which I got very excited about, are like that. I never thought I'd find that again, where it's this kind of anomaly where the guaranteed cash flows are exceeding the market cap and all of that.

There we have it. Since he made this remark in regard to CONSOL and Alpha, we can confidently say he bought at least these two on the basis that their guaranteed cash flows were so large compared to, and even greater than, their market caps. To figure this out, one can look at each company’s contracted sales and the agreed on price for those sales and make the calculation. So there’s some homework for ourselves, and you, if you’re interested. Maybe it’ll be the topic of a future write-up.

For us, we’re content playing this exciting situation in the coal sector though our position in Natural Resource Partners. As a royalty company, NRP essentially collects rent payments from the coal producers who operator on its land. NRP’s largest lessee is Alpha Metallurgical Resources. So Alpha’s success is NRP’s success as well. If you want to know why we’re bullish on NRP, check out the links to the four pieces below.

A Coal Royalty Company—Natural Resource Partners (link)

Another Look at Natural Resource Partners (link)

Coal’s Resilient Future (link)

Portfolio Update (NRP & MSB) (link)

With that, we’ve wrapped up another episode of Special Situation Investing. Thank you for reading and listening. We’ll see you all next Saturday with our next piece!

Cannibal Monsters