Welcome to Episode 133 of Special Situation Investing.

It’s been three months since our last Portfolio Update.

We use these pieces to summarize updates from quarterly reports and earnings calls of companies in our portfolios and occasional honorable mentions from our watchlist. The goal is to record highlights in a succinct format, capturing our current thoughts for future reflection. We hope you find these updates valuable.

Garrett Motion

We purchased Garrett Motion (GTX) in 2020 when it was going through bankruptcy and it’s the largest “special situation” in our portfolios. While we don’t intend to hold GTX longterm, it does have characteristics we like to see in quality companies, namely: plenty of free chase flow and shareholder-friendly management. Consider the following quote from the company’s conference call:

This quarter, we repurchased $65 million of common stock, bringing our total repurchases in the first-half of 2024 to $174 million….Since the successful conversion of our preferred stock last year, we have reduced our debt by $394 million. At the same time, we have also repurchased $958 million in stock or 34% of shares outstanding.

Annualizing Garrett’s second quarter free cash flow of $62 million, the company trades at a yield of 14% on a $1.8 billion market cap. Management is vocal about its intention to continue returning cash to shareholders through debt repayment and share repurchases:

We will continue to use our strong cash generation to acquire more shares in the second-half. All the actions taken are driven towards making Garrett a highly attractive investment with potential for significant additional upside.

Part of making Garrett “highly attractive,” in our opinion, includes obtaining an debt rating of at least BBB. The company’s progress in that direction over the last quarter was mentioned by the CFO:

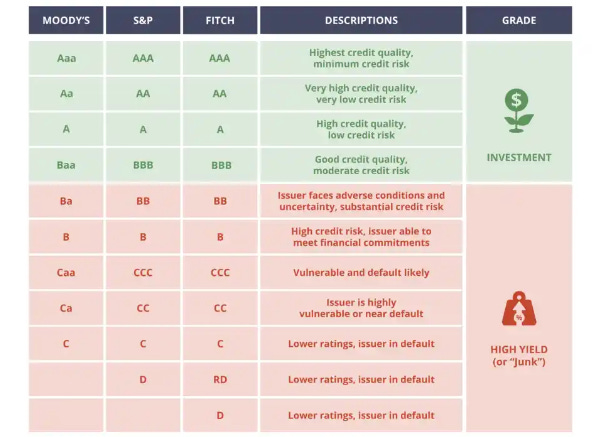

These actions [paying down and refinancing debt] that [the CEO] mentioned are expected to generate annual interest savings of approximately $15 million. Importantly, these changes contributed to upgrades of our credit ratings of our secured debt from both S&P and Moody's to BB+ and Ba1 respectively.

Checking the chart below of S&P and Moody ratings, one can see that Garrett, at BB+ and Ba1, is only one level below investment grade.

We are looking forward to watching what happens when this high-cash-flowing company becomes available to more institutional investors.

Mesabi Trust

In a press release on September 10th, Mesabi Trust (MSB) announced the end of its litigation against Cleveland Cliffs. The ruling was in favor of the trust, concluding that the trust had been under paid to the tune of approximately $60 million. Here are the details from the press release:

The Trust received the final award on September 6, 2024, which unanimously awarded the Trust damages in the amount of $59,799,977 for underpaid royalties in 2020, 2021 and the first four months of 2022, plus pre-award interest in the amount of $11,288,269, calculated at the rate of 10% simple interest per annum from the date of the initial demand through September 1, 2024, and continuing to accrue until paid. Pursuant to the award, Cliffs and Northshore must pay the Trust the amounts specified in the Award by no later than October 6, 2024.

At the time of the announcement, $71 million was about 30% of the company’s market cap. The following day, the stock jumped more than 20% and has drifted upwards since. But, even after this rise, the market is not fully pricing in what this announcement means for Mesabi.

Consider that $71 million is worth $5.42 per unit (13.1 million units). Since Mesabi is a trust and simply passes all its earnings to its unit holders, we except this large payout to be distributed within the next few months. Hypothetically, if one bought the stock at its current price of $21.57 and subtracted out the upcoming distribution, it’s as if one is paying $16.15 for the stock.

Mesabi’s current dividend is $0.30, yielding about 6%. While we haven’t checked this number ourselves, Murray Stahl recently said Mesabi’s legal fees for this lawsuit were about $0.20 per unit per quarter. If those fees are no longer required, the quarterly divided could increase to approximately $0.50. That would be a 9.2% yield on the current price and a 12.4% yield on the cost basis after subtracting out the one-time distribution.

While we’re not actively allocating to Mesabi, let’s just say we’re happy we kept the dividend reinvest going.

FRMO Corp

Earlier this month, my cohost and I traveled to New York City and attended FRMO’s annual shareholder meeting. Highlights from the trip included iconic sight-seeing, lunch with two friends from Horizon Kinetics, and meeting Murray Stahl.

In contrast to the shareholder meetings of Berkshire Hathaway and, recently, Nvidia, this meeting was intimate, with fewer than two dozen attendees. It continues to confound us how few investors appreciate the unique wisdom of Murray Stahl and ignore what he and his team are building at Horizon Kinetics and FRMO.

An audio (soon to be a transcript) of Stahl’s talk at the meeting is posted on FRMO’s website. Here’s my main learning point.

The first is that Texas is unique in regard to its water regulations. Stahl said:

Texas, in the world of water, is probably unique in the world. The reason it’s unique in the world is, Texas has what’s called the [Rule] of Capture. Meaning, if the water runs through your property, you can do, within reason, more or less, whatever you want with the water. Everywhere else in the world you really can’t do that. There’s also the El Capitan reef, this huge under ground river that basically runs underneath the Delaware Basin. So it’s a unique geological structure as well.

If you own the land you can’t do that in Canada. You can’t even do it in most places in the United States. You could never provide the amount of water that is needed. So that’s why if you look at the other hydrocarbon basins in the United Sates, the Eagle Ford, Haynesville, the Niobrara, etc, what you’ll find is, the limiting factor is water. Can’t get the water. So if you can’t get the water, you can’t do the fracking. If you can’t get the water, you can’t do the data centers.

You might say, California is the American center of technology, so you’d wonder why we wouldn’t build a lot of data centers there. There are a lot of data centers there, but the modern data centers are going to need a lot of water, and what is California short of, water. So obviously there’s a limit to how many data centers you can build in the state of California. So data centers have to go where the water is, fortunately or unfortunately, depending on your point of view.

Therefore, in addition to cheap energy, abundant produced water, an unregulated energy grid, and vast open spaces, our two Permian Basin land companies—Landbridge and Texas Pacific—also have favorable regulations supporting their water investments. The number of tailwinds behind these two companies just keeps growing.

Regarding Landbridge specifically, yours truly asked Stahl what regulations or economic incentives cause produced water to flow out of New Mexico across Landgbridge property in Texas and then back into New Mexico. Here’s Stahl’s reply:

Landbridge talks about the investment opportunity of water that’s coming from or going to NM. What is the regulation in NM? So unlike TX, NM does not allow you to dispose of water in the ground.

So this refers to produced water. There’s two kinds of water…there’s sourced water and produced water. Sourced water is what you pump into the well to frac. Produced water is the water that comes out of the well. In primordial times, in addition to carbon-based life forms that basically decayed inside sandstone, water got in there as well. When you fracture the sandstone, the water is released and comes to the surface as well. It’s not a big problem, separating oil from water, but you now can’t take that water and pump it back into the ground. The water must be transported to TX. Landbridge doesn’t transport that water, a sister company to Landbridge known as Waterbridge which is owned by the same people, Five Point Energy, they do the water transport. And [Landbridge] gets a tariff from that and could further benefit from that because you could, in theory, dispose of that water on Landbridge property.

What’s the other Landbridge opportunity? You need sourced water. TX has a lot more water than NM. And there’s also restrictions on using source water in NM. NM is much stricter. By the way it’s not just state, it’s also federal. A lot of the exploration occurs on federal lands [generally subject to] a set of laws called the Lands and Waters of the United Sates that covers what you can do with water in a lot of places in the country. But TX property is grandfathered in by the TX constitution even though it hasn’t been its own country for a while. So you can do things with water in TX you can’t really do in the rest of the country. So in principle, the Landbridge could take sourced water from its property and transport it to NM for use in fracking and once that water turns into produced water it can go right back and be disposed of.

Walking away from FRMO’s meeting, my cohost and I have increased respect for the Horizon Kinetics team and are more bullish on TPL, Landbridge and FRMO.

Texas Pacific Land

Over the last quarter TPL announced an acquisition. Here’s the pertinent text from the press release:

TPL acquired mineral interests across approximately 4,106 net royalty acres located in Culberson County, Texas. The acquired mineral interests overlap existing TPL royalty acreage in current and anticipated Drilling and Spacing Units, enhancing TPL’s net revenue interests in existing and future oil and gas wells…In addition, the acquired mineral interests overlap with TPL surface acreage.

The acquired surface asset spans approximately 4,120 acres in Martin County, Texas and is strategically located in the core of the Midland Basin. The asset generates numerous revenue streams across water supply, produced water disposal, and multiple other surface-related activities, including royalties from a solids waste landfill…and possesses significant additional commercial growth opportunities.

A chart depicting the acquired rights and acres, shown with TPL’s legacy acres, is displayed below.

The press release also had the following quote from TPL’s CEO:

Acquiring high-quality mineral interests in the northern Delaware Basin and strategic surface acreage in the Midland Basin will immediately contribute to TPL’s free cash flow. The combined asset purchase price implies a greater than 13% 2025 free cash flow yield at current strip prices giving credit to only existing production and line-of-sight wells and opportunities.

If the CEO’s estimates prove accurate, then this could prove excellent capital allocation. Over the longterm, we think these estimates will prove conservative.

Conclusion

With that we’ve wrapped up another episode of the show. Thanks for joining us in our investing journey. Let us know where we got something wrong or what we’re missing in the comments section. Thanks for your participation! We’ll see you all in two weeks with another write-up.

Share this post