Welcome to Episode 126 of Special Situation Investing.

It’s been three months since our last Portfolio Update. As such, it’s time to check in on a few of our top names.

As a quick reminder: we use these pieces to summarize updates from quarterly reports and earnings calls of some of the highest conviction companies in our portfolios. The goal is to record highlights in a succinct format that acts as a journal, capturing our current thoughts for future reflection. We hope you find these updates valuable.

But before jumping into today’s piece, first a quick question and poll for our readers.

I recently listened to an interview with a high-profile value investor where he described what he looks for in a quality company. Here’s how he put it:

So there are different flavors of [quality] but our flavor is…1) a natural monopoly; 2) a rational duopoly; and 3) a low cost operator…We want those things because they have durable cash flows, if something is a good business, because of one of those three characteristics, you have a lot of confidence that when you forecast its cash flows out into the future, they’ll turn out within some band of uncertainty that’s not that wide.

After hearing that, I checked out this investor’s top holdings. One company in his portfolio surprised the heck out of me. So much, in fact, that it’ll be the subject of a future piece.

Now for the poll. Out of the categories of companies listed below, where would you be most surprised to find a “quality” company?

Thanks in advance for filling out the poll. With that, let’s dive into this quarter’s portfolio updates.

Natural Resource Partners

Today kicks off with one of our favorites, Natural Resource Partners. Over the last quarter, NRP continued its dogged pursuit of eliminating debt and freeing up cashflow for unit holders.

NRP’s CEO, Craig Nunez, provided a helpful summary of NRP’s current status in the company’s earnings press release:

NRP generated $72 million of free cash flow in the first quarter of 2024 and $312 million of free cash flow over the last twelve months. NRP has generated more free cash flow over the last two years than during any comparable period in the history of the partnership. This performance has allowed us to make considerable progress toward our goal of eliminating all our financial obligations. The sum of debt and preferred equity outstanding is down to approximately $260 million [note: I mistakenly said $206 million in today’s recording]. The partnership is warrant free and our financial position is solid and improving. While we expect lower prices for coal and soda ash to drive our free cash flow in the coming quarters below the record levels realized in recent years, we expect to continue making steady progress paying down debt and preferred equity. We continue to believe eliminating all our obligations while maintaining common unit distributions to help cover unitholder tax liabilities is the right strategy to maximize intrinsic value and maximize unitholder returns.

We also believe NRP will likely see free cash flow in 2024 retreat from its recent record highs. Not that it necessarily creates a trend, but cash flow over the trailing twelve months, as of Q1, is down $1 million from 2023’s $313 million.

The amount of cash flow will dictate how quickly total obligations get reduced to zero. The chart below shows the rate of the reduction slowed considerably in 2023 as well as so far in 2024.

In 2023, NRP prioritized paying off warrants and preferred equity and even increased its debt to do so. Additionally, in the first four months of 2024, 1.5 million warrants were paid off with $65.7 million in cash and by issuing 287,826 units. With warrants eliminated last quarter, we expect the company will now prioritize the elimination of preferred shares. We suspect the recent increase to its credit facility from $155 million to $200 million, is to provide management the ability to use that to pay off the 12% preferreds or higher interest debt.

Given management’s track record and open communication, we’re confident they will steadily and wisely get the partnership to the approaching greener pastures with higher dividends. We continue to increase our stake in this partnership.

Texas Pacific Land Corporation

There’s quite a bit happening with Texas Pacific Land. In its quarterly report press release and earnings call, three developments stood out:

There was the 3-for-1 stock split which was effective as of March 26, 2024

This was expected and the first use of the company’s new, and much litigated, share authorization. On a related note, the company also announced an acquisition committee. In our opinion, it would take an amazingly good deal to warrant diluting shareholders to acquire something. But who knows, stranger things have happened. Honestly, we hope the company uses its remaining authorized shares to enact another stock split.

It was reported that $10.3 million had been allocated to common stock repurchases over the last quarter.

This was encouraging. But from a company with no debt, high and steady free cash flow margins and almost a billion dollars in cash, these repurchases appear to be a small olive branch extended to shareholders who have been clamoring for buybacks. It was a small token but an encouraging one. More on shareholder returns in a bit.

Most surprising was the announcement that the company had developed a new method of water desalination and treatment for produced water.

Here’s the quote from the press release:

The company announces today the development of a new energy-efficient method of produced water desalination and treatment. The company has successfully conducted a technology pilot and is progressing towards the construction of a larger test facility with an initial capacity of 10,000 barrels of produced water per day.

We knew TPL’s water business was operating successfully. In the last quarter, TPL’s water segment brought in a near record quarterly revenue of $37 million. We recognized the Permian Basin’s need for water for fracking as well as locations to dispose of produced water. Murray Stahl has talked at length about the millions of barrels of produced water per day coming out of Permian Basin oil wells. We didn’t know TPL was experimenting with a novel solution.

Here’s a few highlights direct from the company’s special presentation:

TPL has developed desalination technology that leverages the differing water freeze points across salinity levels.

The project is being done in close collaboration with a top-tier technology partner in the industrial freezing industry.

Fractional freezing, as the process is called, is more energy efficient than alternative desalination techniques.

The company is continuing to make equipment and process optimizations.

There has been a successful R&D trial at a TPL facility in Midland; procuring equipment for a larger test facility with capacity of ~10,000 barrels of water per day.

The treated water product has been safe for irrigation thus far and meets most quality requirements for various methods of discharge Granted Land.

So a hat tip to the TPL team if they can pull off a novel solution to the Permian Basin’s (and all US shale basins’ for that matter) produced water problem. We highly recommend you listen to TPL’s entire earnings call. The CEO and President of TPL’s water business go in-depth on this announcement.

Because one of TPL’s strengths is its asset-light business model, if its water business proves too capital intensive, we would likely be in favor of spinning it off, with TPL maintaining a revenue share. But we will see how this plays out first before passing our very unimportant verdict.

Two other developments for TPL hit the tapes in the last week.

On June 7th, TPL was included in a list of companies set to join the S&P Mid Cap 400. This could be a result of the resent 3-for-1 stock split increasing trading volumes. Regardless, the stock traded up 24% on the following day and is up 30% to-date.

And lastly, on June 13th, TPL announced a $10 special dividend to be distributed on July 15th to shareholders of record on July 1st. This was in conjunction to announcing a cash and cash equivalent goal of $700 million with cash above this level being allocated to shareholder returns.

In the words of TPL’s CEO:

With tailwinds of excellent business execution, supportive fundamentals, and a fortress balance sheet, we’re pleased to announce a special dividend, which is the largest in TPL’s history and represents a 50% increase compared to the most recent prior split-adjusted special dividend. As we evaluate our current capital structure, capital allocation priorities, business fundamentals, and investment opportunities, we have set a target cash and cash equivalents balance of approximately $700 million. Above this targeted level, TPL will seek to deploy the majority of its free cash flow towards share repurchases and dividends.

In summary, with the cloud of litigation no longer shrouding TPL, we are cautiously optimistic about its short-term prospects. As always, on the long-term prospects, we couldn’t be more optimistic.

PrairieSky Royalty

After PrairieSky Royalty’s Q1 earnings call, we posted a Note on Substack, stating: “Debt repayment, cool-headed capital allocation, and buybacks in the works…couldn’t ask for more from PrairieSky Royalty.” We also attached the following comment from the company’s CEO regarding future use of cashflow currently allocated to debt repayment. He said:

I think on the return of capital piece, we obviously have the dividend which is $239 million annually. So any excess cash flow right now is just going towards paying off the debt.

I think if you look at how we did it historically, we weren't seeing good M&A opportunities in 2017 and 2019. For the most part, we saw a better value in buying back stock, better long-term returns for shareholders in buying a PrairieSky share. And we're unique in that we always have that option. So we bought back about $40 million of stock each consecutive year. And then during COVID, when things got dislocated, we bought back $100 million in August of 2020. And right now, our cost of debt has gone up materially.

We borrowed to execute on the Heritage acquisition which we closed December 2021. We borrowed $728 million and that's been repaid for the most part. Well, as you mentioned, it will be somewhere in the middle of next year where it's completely repaid. And so as we're moving towards that, we've got to start thinking about the excess cash.

And I think there is an opportunity to even build some cash in this environment. I think you just want to have those options going forward to either make a great acquisition which has a high return on invested capital or conversely buy back more shares.

And I think if you look at where the business sits today for the next ten years versus the last ten, we IPO’d with 5.2 million acres and 130 million shares. Today, we have 239 million shares and we have 18.3 million acres and some of the highest quality acreage in some of the faster growing parts of the basin.

You don't want to dilute that great asset base. So, I think it will definitely be a return to shareholders. We won't have a defined plan. We'll just do it. We'll do what makes the most sense when we sit as a board and discuss it. But the buybacks will start to come into play sometime in the next year or so.

Such clear thinking and everyday-language is what we like to see from management of our companies.

Circling back to the potential share repurchases next year. While exciting they won’t be earth shattering. Consider that PrairieSky allocated $93 million toward debt repayment in 2023. If it has instead applied that amount to repurchases, only 1.5% of its current $6.2 billion market cap could have been retired. That said, any increase in cash returned to shareholders will be well received.

But in order to begin retiring shares, debt will be eliminated first. At year end 2023, bank debt stood at $188 million and that was decreased in Q1 by $14 million to $174 million. Here’s how the company allocated it funds from operations in Q1:

During Q1 2024, the company generated funds from operations of $83.0 million, declared dividends of $59.7 million, and made royalty acquisitions for cash consideration of $8.8 million. The company had net debt of $208.3 million at March 31, 2024, down from $222.1 million at December 31, 2023, as funds from operations in excess of dividends paid of $57.3 million and acquisitions of $8.8 million were primarily used to decrease net debt during the quarter. Bank debt at March 31, 2024, net of unamortized debt issuance costs of $0.4 million, was $174.6 million.

Lastly, PrairieSky maintains slow and stead growth. The company’s most recent presentation provided data showing growth across a number of metrics. The graph below shows, in terms of both production per million shares and share of industry capital, PrairieSky is moving up and to the right.

Honorable Mentions: Permian Basin Royalty Trust and Bitcoin/Greyscale Bitcoin Trust

Two of our other investments warrant a quick mention.

The first is Permian Basin Royalty Trust which continues to chill at 52-week lows. Two reasons appear culpable.

First, the operator on the Trust’s Waddell Ranch property, Blackbeard Operating, continues to plow capital expenditures into the property and has given no indication as to when the amount of expenditures will decrease. Secondly, the Trust’s trustee initiated a lawsuit against Blackbeard to recover what it believes is approximately $15 million in illegitimate charges. Surprisingly—and whether its in response to the suit or not we don’t know—Blackbeard failed to send May’s monthly royalty information by the normal deadline. This led to no royalties from Waddell Ranch being included to May’s distribution.

In short, there’s a mess between royalty owner and property operator that unfortunately must be sorted out in court. But we’ve been along for the ride is a couple lawsuits before—see previous pieces on Texas Pacific Land and Mesabi Trust—so we remain undisturbed by these proceedings.

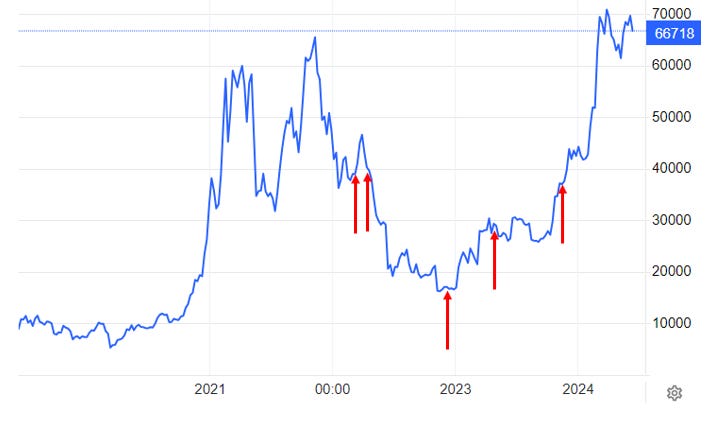

The second honorable mention is Bitcoin. It makes us laugh that our pieces with the fewest listens/reads are all our pieces related to Bitcoin. Clearly, if we were doing this for stats, we wouldn’t write about Bitcoin.

We continue to do so because we believe it has potential we don’t want to miss.

Just for fun, I recently reviewed our previous Bitcoin pieces and built a price chart with arrows indicating the days our pieces on Bitcoin were published. I hope for the first two pieces you all thought we were just bat-crap-crazy and then for some reason, after our third piece, it clicked and you fell in love with Bitcoin. Of course we had no idea the third piece—titled Eight Ways to Value Bitcoin—would correspond almost exactly to the recent bear market bottom. But seeing that made me chuckle. And just incase you’re curious, yes, we remain bullish on Bitcoin even today.

Conclusion

As always, thanks for reading and listening. If you enjoy our work, we would appreciate if you shared this piece. If you have a Substack of your own, a recommendation would make our day. Thank you to everyone who chimes in with comments as those are where the both of us get the highest return on the time we invest in sending these pieces into the ether. Thanks for joining us in our investing journey. We hope we are a benefit to yours. See you all in two weeks.

Share this post