Listen to the Special Situation Investing Podcast on Fountain, on Apple Podcasts, on the website, or wherever you listen.

Welcome to Episode 56 of Special Situation Investing. Today we are looking at a company that’s been on our watchlist since we ran across it in a VIC write-up posted by VIC user ARR on June 12, 2020. The company is OneSoft Solutions Inc, listed on the TSX under ticker OSS, and on the OTCQB under ticker OSSIF.

The Business: history and current state

OneSoft Solutions is a software-as-a-service (SaaS) small-cap company that provides software for the midstream oil and gas sector. OneSoft’s management is fond of saying they sell a revolutionary technology that replaces an archaic, time-consuming, and expensive process within oil and gas pipeline integrity management.

It goes without saying that the integrity of oil and gas pipelines is of huge importance. No one wants oil and gas leaking, or exploding, from pipelines into the environment, not you, not me, and least of all, not pipeline owners. Unfortunately, the majority of US pipelines were built prior to 1970 and the latest stats show that an average 1.7 incidents occur per day on pipelines in the United States. As you can imagine, because of the damage these incidents can cause, pipeline owners are subject to massive amounts of regulations regarding pipeline safety, integrity and management. The junction of maintaining safety and abiding by regulation is where OneSoft’s product comes into play.

It becomes clear why OneSoft’s tech could be considered revolutionary, when its compared against the process for integrity management among midstream operators today. Currently, a device called a pipeline integrity gauge (or pig) is inserted into pipelines and forced downstream by the gas or oil pressure. This pig contains instrumentation that records data as it travels through the pipe, including temperature, pressure, wall thickness, cracks, pipe diameter, bends, corrosion, metal loss, and curvature. When the pig is retrieved at the end of its journey, its data is downloaded into hundreds of Excel files which are then painstakingly analyzed by teams of company employees. Of the colossal amount of data gathered, barely 5% is analyzed with only the largest discrepancies getting attention. Because of the combined limitations of humans and Excel, the current discrepancies are usually only compared against the last inspection data, even though companies often have years, if not decades of inspections’ data. This painstaking process takes months to complete.

This is the legacy process that OneSoft Solutions aims to eliminate.

To do so, the company leverages Microsoft Azure Cloud, data science and machine learning, and predictive analytics into a simple, software-as-a-service solution that they termed Cognitive Integrity Management (CIM for short). CIM can process 100% of the data from pig inline inspections at a fraction of the cost, with minimal human effort, and within minutes to hours, not months. Honestly, put that way, it does sounds pretty revolutionary.

OneSoft in its current business form, began back in 2017 with the launch of its subsidiary OneBridge. Prior to 2017, the company’s management team, who’s worked together since 2004, had launched multiple other software tech companies that they built up and ultimately sold.

Today, OneSoft is still in growth mode. As they’ve added more customers and made a couple small acquisitions, the compounded annual revenue growth rate has been an impressive 75.7% over the last 23 quarters. Even with its impressive revenue growth, the company operates at a loss as it seeks to grow and expand the solution it offers. In the first half of 2022, revenue was $4.7 million and the net loss was slightly more than $2 million. While that is the case, predictive financial models show that the company can expect 50%+ EBITDA margins once past the $10 million revenue mark. The company is powering ahead with the goal of CIM becoming the industry standard. To that end, the it continues to add functions to the CIM package which currently includes: assessment planning, dig management, threat monitoring, GIS data correlation, logistical system and process management and extensive reporting and data visualization.

The company’s management has two main strategies to build stakeholders value: first, focusing on signing up new customers, and second, to the maximum extent possible, reinvesting company resources into R&D to bolster the company’s competitive moat.

Long-term Economics: moat and runway

Given its use of cloud technology, data science, machine learning, and predictive analytics, OneSoft currently holds a substantial lead over its competition. In fact, most competitors are still selling legacy processes that utilize Excel. And the majority of the companies OneSoft is hoping to convert to customers are still using legacy systems and processes, mainly the labor-intensive Excel-based process explained earlier. In its latest investor presentation, management stated that they still know of zero competitors offering a solution even close to CIM.

Even so, the focus remains on securing new customers in order to cement CIM as the industry standard. This means the company has a lot of work ahead of them, but it also means there is the potential for a lot of growth ahead.

Consider that in the US alone there are about 660,000 miles of piggable and 2.1 million miles of non-piggable pipeline. By law, pipeline inspections are required every five years for oil and every seven years for gas. OneSoft’s management estimates that roughly 6,500 PIG inline inspections (ILI) are conducted by US oil and gas pipeline companies each year.

To date, fifteen total customers have signed contracts for CIM. One of its earliest and largest customers is Philips 66 which signed up in 2018. Today the list of customers includes Alaska Pipeline, Sinclair, Dow, Energy Transfer, to list a few with well known names, as well as two unnamed super majors. These fifteen customers have subscriptions covering 180,000 miles of pipeline of which 115,000 miles are piggable. But clearly there’s room to grow as there are are an additional 545,000 piggable miles of pipeline in the US alone.

Looking a couple steps into the future, OneSoft has asperations to capture market share internationally and on pipelines that are not piggable. While focused on its core of US-based, piggable pipelines, the company has taken small steps into both of these areas of expansion. Just this last October, a subscription was signed with OneSoft’s first foreign customer, a company based in Australia. Also, part of the company’s R&D is focused on developing algorithms that will interpret external data sets such as type of soil, metal type, coating, temperatures, seismic, and so on. Adding these features will allow CIM to be used for non-piggable pipeline, giving OneSoft access to an additional 2.1 million pipeline miles.

Additionally, while to date OneSoft has focused on major industry players, it recently initiated a sales strategy geared toward smaller pipeline companies; specifically the 1,800 US companies that operate fewer than a thousand miles of pipeline. On September 12th of this year, the company announced the release of its Corrosion Growth Analysis product, which the first phase of its Pipeline Integrity as a Service offering. This product will allow companies to submit PIG inspection data directly to OneSoft and have OneSoft run comparison analysis with CIM to identify defects and threats to their pipeline. This is a “pay‐as‐you‐go” deal which OneSoft hopes will appeal to these smaller companies that may not yet willing, or able, to fully adopt CIM.

Given the industry-wide recognition it is now receiving, and the types of customers it is now onboarding, management believes that early adopter customers have proven the value of OneSoft’s products, and the company has transitioned to a new stage where more hesitant customers will seek out the advantages of CIM’s now proven technology. And the pace that new customers are being announced does seem to support the argument that OneSoft’s flywheel is gaining momentum. Additionally, as more customers witness the time and money savings of using CIM, they will likely act as unpaid advertisers causing additional pipeline companies to seek out OneSoft for themselves. Another, less concrete accelerant, is that as younger individuals take over managements of these pipeline companies, they will be more comfortable with cloud-based, machine-learning products, likely accelerating the industry’s adoption of CIM.

Management: history and ownership

A few quick words about the management of the company.

First, the current management team has worked together since 2004 and on many different projects and companies.

Initially, the fact that the management team has built up and sold multiple software tech businesses in the past seemed to be a negative. It made us wonder if their plan was to quickly build up OneSoft only to make a profit by selling it. Whether that happens in the future or not, shareholders along for the ride will probably make out just fine. This is because management is closely aligned with shareholders as the directors and management combined currently own about 30% of the company’s stock.

And on further thought, and after much reading through company documents and listening to many interviews with the management, the initial negative slant on the management’s history seems a bit ill founded. Rather than a history of pumping and dumping multiple companies, the management’s track record appears to be one of building companies, learning from each creation, taking parts of what they built and moving on to create something bigger and better. For example, in 2014, management sold off its legacy operating business called Serenic. But that was only after, through Serenic’s partnership with Microsoft, management saw the opportunity to take what they learned and pivot it into what later evolved into CIM.

Valuation:

Given that OneSoft has yet to consistently make a profit, many common valuation methods are impracticable or impossible. What is possible is making educated guesses about the total addressable market that the company has a chance of capturing and estimating what revenues would then result.

To set a baseline: OneSoft currently has a market cap of $40 million and its revenue for the last three months was approximately $2 million of which 90% or more comes from recurring subscriptions.

So, in rough numbers, the company brought in $7.2 million of recurring revenue stemming from the 115,000 miles of piggable pipeline it currently has under subscription. Some simple division would lead us to estimate that the company brings in about $63 per piggable mile per year. (Note: VIC user ARR claimed the company average $100 per mile per year. We were unable to find that figure in any company documents. But, regardless, our estimate is likely very conservative.) Taking this to the hypothetical conclusion of OneSoft capturing 100% of all piggable pipeline miles in the US, its revenue could rise to $42 million.

Let’s look at the numbers from another, hypothetical situation. Remember that approximately 6,500 PIG inline inspections occur in the US per year. What if OneSoft was able to capture all of those inspections through its pay-as-you-go, integrity-as-a-service product it recently announced? OneSoft’s pricing for this product is $4,950 for analyzing the data from the latest inspection and comparing it to the data from one previous inspection. If the customer wants to compare the current data to more than one past inspection, there is a charge of $500 per additional data set.

So in our hypothetical example, OneSoft captures all 6,500 annual US PIG inspections, and let’s say the customers on average want the current data compared to the past two inspection data sets, for a total charge of $5,450. Simple multiplication gives us a hypothetical revenue of $35 million.

Yes, these thought experiments are horribly simplified. For one they assume that OneSoft is able to take 100% of the market share, in the first, of piggable US pipeline miles, and in the second, of annual US PIG inspections. This is highly unlikely. But it also doesn’t take into account any inroads that OneSoft makes into capturing part of the 2.1 million miles of US non-piggable pipelines, or any expansion into the 40% of global pipeline miles that are outside the US, or even any price increases the company may make as the company gains market share and adds functions to its products. If anything, these thought experiment estimates are likely conservative.

Sticking with its current revenue-to-market cap ratio of 5.5 (which is also a conservative call), our hypothetical scenarios project a market cap in the ballpark of $193 million to $231 million. Which, assuming no share dilution, would suggest roughly 300-500% upside potential.

Risks

While OneSoft Solution appears to be at an inflection point in their quest to become the industry standard pipeline integrity management, before any capital is put into its stock, its important to think through possible risks. Here are a few for thought:

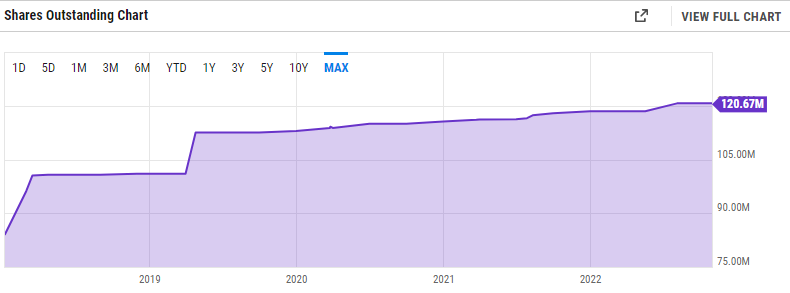

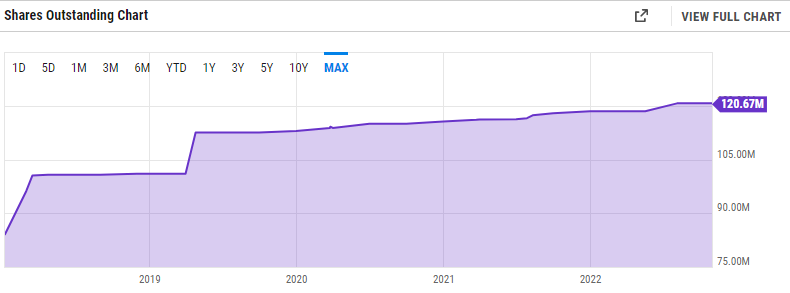

Like many companies in a growth stage, OneSoft has a track record of funding its R&D with cashflow its but also by selling new shares. The company also has a share-based incentive program for employees. The increase in share count since 2018 is show in the chart below. The shares outstanding have increased from 84 million to 124 million. So there is a risk of further dilution.

Even though OneSoft appears to hold a commanding lead over any potential competitors, that could quickly change. This is especially true of companies in the tech space.

Because CIM is hosted on Microsoft Azure Cloud, OneSoft pays a recurring fee to Microsoft. This fee is currently about 10% of revenues but that percentage is expected to drop as OneSoft continues to add more customers. A couple risks connected with this partnership are an increase in the fee; a failure of the cloud services altogether, such as a cyber attack; or a disagreement between Microsoft and OneSoft.

And lastly, OneSoft currently is committed to pay minimum royalties totaling $2.25 million through December 20, 2027 to Philips 66 for intellectual property Philips gave to OneSoft to jumpstart their product. This is less a risk and more just a known liability. As of September 30, 2022, royalties of $953,759 have been expensed and $802,279 has been paid since contract inception.

Conclusion

In conclusion, while at the time of this episode neither host of this show have invested capital in OneSoft, we do think the company has a lot of potential as a growth play. It appears to have a strong and growing moat, a product that is needed product, a long runway in terms of potential market cap growth and total addressable market, and a management team that are focused and have considerable skin-in-the-game.

Alright, that does it for another episode of Special Situation Investing. Hopefully you got something out of seeing our thought process on this company. We encourage you to take a deeper look at OneSoft if you found it interesting. And of course, always do you own research.

A quick thank you to those of you listening to the show via the Fountain app. We appreciate the support and sats you are sending our way via that platform. And remember, you can get paid in sats yourself for just listening to an hour per day of any podcast on Fountain.

Alright, we hope you enjoyed the episode and found it educational. We’ll see you soon on the next episode.

OneSoft Solutions (OSSIF)