Welcome to Episode 129 of Special Situation Investing.

Our introductory piece on Keweenaw Land Association (KEWL) kicked off with Mark Twain’s quote: “buy land, they are making any it anymore.” While we didn’t recommend the stock—we don’t make recommendations…just report how we allocate capital—anyone who bought KEWL at the time of that report would be sitting on a 28% gain in just about three months. That said, the increase in the stock price is the least interesting change that occurred since our last write-up.

A Quick Refresher

Keweenaw Land Association owns mineral royalty rights in the state of Michigan’s Upper Peninsula. Until 2021, the company also owned 180,000 timberland surface acres but those were sold after new management took over following a proxy fight in 2018, led by Keweenaw’s largest shareholder, Cornwall Capital. Other actions taken by the new management included: selling non-core assets, reducing debt, initiating a share repurchase program, dramatically reducing overhead, and acquiring new income streams.

Despite these positive changes, KEWL’s revenue was a meager $292,000 in 2023, against a current $41 million market cap. The company trades at 243x its net income.

So why is the company interesting?

Number one, it’s an asset-light, hard-asset-based business, something we are fond of these days.

Secondly, and more importantly, some of the acres owned by KEWL are positioned under Highland Copper’s fully-permitted Copperwood Project mine. Begun in 2008, the project appears close to the construction phase and a couple years from production. When this occurs, KEWL will produce its current market cap over a three-year time period, based on estimates from our last report. But the question remains today—as it has for the last sixteen years—when will the mine reach production. We wish we knew.

In the meantime, Keweenaw’s new management reduced the company to a bare-bones operation and is running the company as if the Copperwood Project bonanza will never occur—a prudent choice. For more details on the company’s history, and our view on the its potential, check out our original piece. But now, here’s today’s update.

The Update

On July 9th, Keweenaw posted a press release with two announcements. The first was regarding a recent acquisition:

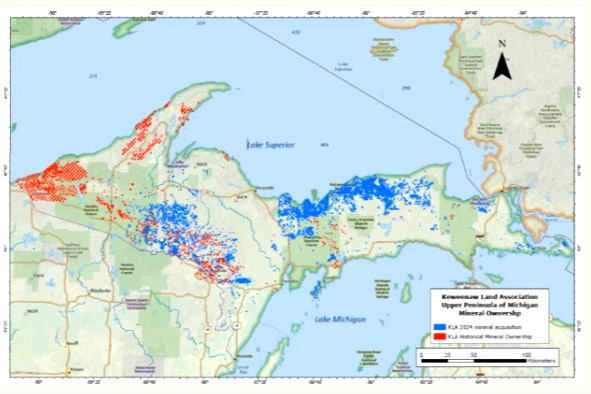

[The company] completed the purchase of 667,300 acres of unencumbered, severed mineral properties ranging across the Upper Peninsula of Michigan for a purchase price of $970,000…This transaction significantly expands Keweenaw’s mineral ownership, increasing mineral acres under management to over 1.1 million acres.

For a price of $1.45 per acre, Keweenaw grew its acreage from 439,274 to approximately 1.1 million. This dramatic increase is shown in the image below with previously owned acres displayed in red and new acres in blue.

The company’s CEO, Timothy Lynott, gave a peak behind the curtain regarding this acquisition, revealing extreme patience and objectivity on the part of management. He said:

To provide some background on how we got to this [acquisition], the opportunity came to Keweenaw in May of 2022, by way of a business vender. At the time, the seller was hoping for a transaction in the high seven figure to low eight figure range, which was a bridge too far for Keweenaw. But being in the mineral business, we were considered a qualified bidder and were granted access to the data room….

And while we were certainly aware of the situation, it took us almost a year before the situation progressed to a point where we felt confident the terms provided us with a margin of safety. We watched and waited as three bid deadlines came and went. With the quality and the organization of the information improving each time, largely due to feedback from Keweenaw. By the end of 2023, Keweenaw made its first bid and the transaction closed last month.

It appears management patiently watched this opportunity for over a year, passed on three bidding cycles, and waited until the price dropped from low eight figures to six figures, and when they had a margin of safety they acted. That’s impressive capital allocation.

Not only did the acquisition more than double Keweenaw’s mineral right ownership, it increased the value of its previous acreage. This was accomplished by growing the number of Keweenaw’s contiguous acres. Note that large plots of contiguous acreage ownership is more valuable because they make it easier for prospective lessees to permit and complete projects (e.g. mines) because of the reduced number of parties required to approve it. Importantly, one area where the number of contiguous acres increased was under the Copperwood Project where Keweenaw now owns nearly 100% of the minerals rights, whereas it owned about 80% previously.

The second announcement made by the company in its July 9th press released was regarding share repurchases. Here’s a quote from the release:

Keweenaw also announced today that it completed the repurchase of 51,633 shares at a price of $27 per share on June 4, 2024. The repurchase was privately negotiated with a significant Keweenaw shareholder.

This repurchase represents 4.3% of the shares outstanding prior to the close of this deal. This is by far the largest single repurchase deal management has brokered, but they have been steadily reducing the shares outstanding since 2019. Over that time frame, the shares outstanding has fallen by 14.1%.

The management’s continued support for share repurchases is encouraging. It displays a belief that the company is undervalued in their opinion.

Back-of-the-Napkin Thoughts

With the changes over the last few months, how was KEWL’s value affected?

A simple calculation of dollars per acre is one quick check. Based on its market cap of $41 million, the company is now priced at $37.27 per acre. When we last wrote it up, when it owned only 439,274 acres, it was priced at $72.85 per acre.

Another way to look at it, is through its potential royalties when the Copperwood Project comes online. In our last piece, we used Keweenaw’s 2-4% sliding royalty (4% at $4/lb copper and above), 30k tons of projected annual production, a copper price of $4/lb, and the fact that Keweenaw owned 80% of the mineral rights below Copperwood. At that time, we estimated, on a $32 million market cap, the company traded at a potential FCF yield of 24%.

A similar calculation done today, with the change of Keweenaw now owning 100% of the mineral rights below the Copperwood Project, produces a slightly lower potential FCF yield of 23.4%. Although this potential yield decreased slightly, one must also consider the optionality of the hundreds of thousand of new mineral acres, and the value created by increasing contiguous land holdings. This is in addition to a 4.3% decrease in shares outstanding, which, all else being equal, would increase a single shares value by 4.5%.

In our estimation, Keweenaw trades at a better value today than it did three months ago, when its stock price was 28% lower.

Thoughts on Management

Not only does the company appear to be a better value, recent events also increased our respect for Keweenaw’s management and board. Their patience and capital allocation skill were touched on earlier. Additionally, the more we’ve read about how they led the company since the proxy fight, shows a team with no ego and willingness to take extreme measures to preserve and grow shareholder value.

A question that’s rattled around in my brain since my initial research on this company is the following: Why is Jamie Mai of Cornwall Capital chairman of a little, no-name microcap? Famous for his role in foreseeing, and profiting from, the Great Financial Crisis, Mai’s investing style has largely been about making massively asymmetrical investments, often using options as a leveraged vehicle. Is Keweenaw a similar situation with massive asymmetrical upside potential?

Conclusion

We still find Keweenaw a fascinating company and believe it has impressive potential upside, particularly over a period of years. But, similar to the conclusion after our introductory piece, although the potential upside is similar to our other top investments, the certainty of when that upside will occur (aka: Copperwood coming online or another similar royalty stream) is much less clear.

Compare this to Natural Resource Partners (NRP), for example. NRP trades at about a TTM FCF yield of 25%. This cash will be available to unit holders when the company is done getting its debt to zero, which should take about 12 months.

With that we’ve wrapped up this latest edition of Special Situation Investing. Thanks for your feedback and insights you all continue to generously shared with us via comments and directly at specialsituationinvesting@protonmail.com. Both my cohost and I have learned so much from everything you share with us. Please keep reaching out! We’ll see you all again in two weeks.

Share this post