Welcome to Episode 124 of Special Situation Investing.

Mark Twain was a terrible investor. The 19th Century American author who penned the likes of The Adventures of Tom Sawyer and The Prince and the Pauper passed on an opportunity to invest in a new invention—the telephone—and instead lost his fortune backing bad business ventures. All this from the man who gave what is perhaps the best investing advice ever:

“Buy land, they aren’t making it anymore.”

During Horizon Kinetics’ 2023 Q1 commentary, Steven Bregman explains why Twain was right in the money, stating:

Land is the longest-lived business asset. It is probably the only perpetuity business asset, at least until another planetary body is colonized…Land also has a rising scarcity function, since the world population increases over time. Globally, the arable land per capita is always decreasing.

My co-host and I study a lot of hard asset-based companies with asset-light business models and land companies often take center stage. Texas Pacific Land Corporation, Beaver Coal Ltd, and St. Joe Company are three examples. A closely related, and often overlapping, subset of companies are those that own royalties and mineral rights, including: PrairieSky Royalty, PHX Minerals, Permian Basin Royalty Trust and San Juan Basin Royalty Trust. While only half of these names made it into our portfolios, a few are meaningful positions. We believe land is one of the best assets to own in any period but particularly against an inflationary backdrop.

While we own a few amazing land companies, we are always on the hunt for more.

So over the last month, while my co-host responsibly researched the potential risks behind one of our largest holdings, I, like a kid in a candy store, dove into the OTC (over-the-counter) market in search of under-followed land companies.

A dive into the OTC market is always a wild ride. Over-the-counter companies can range from dodgy quality to first-class, from microcap to large cap, and can provide full disclosure or none at all. Consider, for example, two companies we’ve discussed in the past: Beaver Coal Ltd and FRMO Corp. The first is an $80 million dollar limited partnership that only discloses a simple annual report to partners. FRMO Corp, on the other hand, is a $325 million corporation, run by one of today’s most respected investors, that offers more disclosure than a lot of bluechip companies. Both are OTC listed companies.

But because the OTC market is home to many less-followed companies it is excellent hunting ground for small investors such as yours truly. While a handful of companies caught my eye, one got me interested.

The Company

Keweenaw Land Association, Ltd (KEWL) is the owner of over 400,000 mineral acres in the state of Michigan’s Upper Peninsula. Keweenaw was founded in the 1800s as the result of a land grant by the U.S. government. Here’s how Keweenaw’s annual report tells its story:

Keweenaw traces its origins to 1865, when Congress granted approximately 400,000 acres of public land to finance the construction of a shipping canal across the base of the Keweenaw Peninsula in Northern Michigan. The same year, Michigan’s legislature authorized the Portage Lake & Lake Superior Ship-Canal Company (the “Portage Lake Company”) to build the canal. Keweenaw’s direct lineage traces to 1891, when a successor entity to the Portage Lake Company sold the completed canal to the United States government and contributed its other assets (primarily 400,000 acres of land and mineral rights) to the Keweenaw Association, Limited. That Company was reorganized in 1908, and Keweenaw Land Association, Limited came into existence as a Michigan partnership association. Keweenaw was reorganized again in 1999 as a Michigan corporation.

Until the early 1950s, Keweenaw was managed with the primary objective of monetizing its assets through liquidating timber, exploiting mineral assets, and selling property. During this period, the Company reduced its surface rights from approximately 400,000 acres to 120,000 acres, through a combination of land sales and intentional land forfeitures to extinguish tax liabilities. After clear-cutting most of its harvestable timber acreage during World War II, the Company decided in 1951 to modify its land management strategy. The Company chose to cease land dispositions and allow for the forest to fully regenerate. At the time, the Company expected that the forest would reach maturity by 2010. The Company operated in this mode for the next 40 years, with its primary sources of income being mineral royalties and stumpage income from selective harvests as the timber assets matured.

In the early 1990s, the Company began investing in resources to allow for active management of its forestry operations. From that time until December 27, 2021, the Company harvested, produced, and sold timber as its primary source of business income. On December 27, 2021, the Company closed on the sale of all remaining timberland assets which consisted of approximately 178,479 acres of land as well as the Company’s remaining capital assets. The Company retained ownership of its mineral interests.

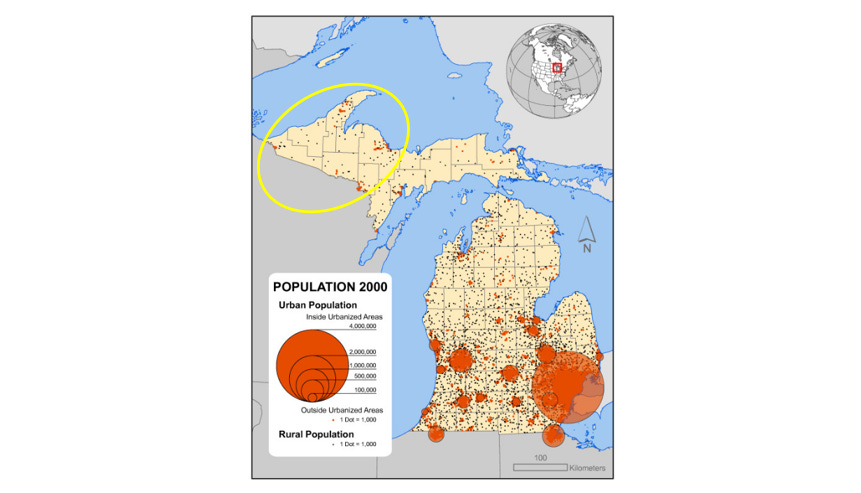

As a reminder, the state of Michigan has two geographically separated sections. The one to the north—called The Upper Peninsula—is where Keweenaw’s mineral rights are located. The area is highlighted by the yellow circle in the image below.

The Upper Peninsula has been the birth place and burial ground for many copper and iron mining projects. Maps of this part of Michigan are littered with “iron” and “copper” in the names of towns, cities, landmarks, etc, indicating how deeply those industries shaped the area. In the 19th and 20th centuries, Michigan, but particularly The Upper Peninsula, produced nearly half of the United States’ iron and copper.

The colorful history of Keweenaw Land Association was broadly covered in the annual report quotation above, but to understand Keweenaw today requires a deeper look at the years 2018 to the present.

Pertinent History: 2018-Present

Starting in the early 1990s, after forty years of passive management, Keweenaw began to actively manage its assets—at the time, 178,000 timberland surface acres and 429,000 mineral acres. Suffice it to say, the results were poor. The value-stifling situation led to a proxy fight between the company and Cornwall Capital, one of Keweenaw’s major shareholders.

Made famous in The Big Short for being one of the few firms to foresee and benefit from the Great Financial Crisis, Cornwall Capital owns approximately 26% of Keweenaw shares. The proxy fight concluded in April of 2018 and was successful in replacing a number of board members and executive management and promoting Cornwall Capital’s chief investment officer, James Mai, already a Keweenaw board member, to chairman.

The new management and board quickly started to right the ship. Early efforts included:

Increasing disclosure.

Reducing debt.

Creating non-timber related income streams such as easement leases.

Systematically cataloging geological data from previous exploration and production activities on its properties.

Conducting outreach to exploration companies who could become potential customers.

Initiating a share repurchase program.

These efforts reached a climax in December of 2021 when the company successfully closed a deal to sell its 177,770 timberland surface acres. The transaction was structured such that shareholders would received about $100 in special dividends in two tranches. The first of $92 was pay immediately. The remaining $8 was to be distributed when released from escrow, but ultimately, management opted to use those funds for tender offer instead. They believed a tender offer would allow shareholders to opt in or out of the “new Keweenaw,” a company substantially different after the timberland sales.

The Company Today

With the timberland sale completed, Keweenaw became a 100% minerals-focused company. Its portfolio of 439,274 mineral acres is represented in the map below.

Because timber sales were the largest contributor to the company’s revenues, Keweenaw is now much smaller—sporting a meager $32 million market cap—and it looks very different from a financial perspective.

Since the timberland sale, the company has been operating at a loss. Operating income burn rate was approximately $350,000 in 2022, $200,000 in 2023, and the company expects it to be around $100,000 in 2024.

The company has covered these losses with the cash left over from the timberland sale but management and the board are focused on getting to the point where steady cashflows allow the company to operate in the green. To achieve this, they have acquired new income new streams and aggressively cut costs.

Increased Income

The table above shows a few things. First, the bulk of the company’s income is lease income. Of its total 439,274 mineral acres, 5,607 are under lease. Since the mine for which those acres are leased is not yet in production, Keweenaw receives only a lease payment and no royalty payments. The lease payment was $266,625 in 2023 and will increase to $354,700 in 2024.

The table also shows that Keweenaw was successful in adding new income streams in 2023. These included:

A working capital and copper recycling royalty agreement with a regional copper recycling company. Keweenaw will earn interest on the working capital line as well as on a per pound of copper that the recycling company produces. Revenue from these royalties was $790 in 2023.

Keweenaw entered into a 4-year option agreement with a solar energy company which allows the company build a project on some surface acerage Keweenaw kept after the timberland transaction. This agreement provided $20,000 in revenue in 2023.

An easement with an undisclosed partner that produced $5,000 in revenue for 2023.

Reduced Costs

More impressive than Keweenaw’s ability to add revenue has been its ability to cut costs. Measures taken on this front have included: reducing the board size from five members to three, eliminating the chairman’s salary, reducing the employee count down to three, closing the company headquarters and operating remotely, downgrading to a cheaper tier on the OTC market, and hiring a new auditing firm. In short, the company now operates at what board chairman Mai calls a “bare-bones” operation.

After attacking the cashflow problem from both the income and cost directions, management believes it’s close to operating in the green. Mai said the following in the company’s 2023 Annual Letter:

For 2023, the cash burn before discretionary spending was around $200 thousand. We expect this amount will drop by up to 50% for 2024, due to contractual step-ups in existing leases and modest expansion in the working capital facility. While it is too early to claim victory, we are pleased this pro forma cash burn level reflects a reduction of about 75 percent relative to only 2 years ago.

It’s worth noting that these cashflow calculations don’t take into account the $410,000 of interest the company received on its cash pile of $8.4 million. Clearly, the rise in interest rates is helping the company cover its costs, but since this is not sustainable income, management is focused on getting the company in the green without it.

They appear to be well on their way to doing so.

The Situation

If Keweenaw only had 400,000 mineral acres and a few meager income streams it wouldn’t have caught my attention. What had me digging deeper is the existence of a high-payout situation that may play out in the near future.

This situation was hinted at earlier when I mentioned that a miner pays Keweenaw an annual lease payment. The lessee is Highland Copper (HDRSF) and the lease is on the property beneath its Copperwood Project.

Copperwood is a fully permitted mine. Listening to a few interviews with Highland’s CEO, they are at the stage of acquiring the requisite capital to commence construction.

But timing is everything with building mines. Case in point, the Copperwood Project has been in the works since 2008. And even after beginning construction, it would likely be two years before Keweenaw would receive any royalties.

Two recent developments give hope that construction at Copperwood might finally get under way. First, the State of Michigan just awarded Highland a $50 million grant to support the Copperwood Project. This both provides part of the required capital and signals the state’s blessing on the project.

Secondly, the rise in the price of copper should incentivize those involved with Copperwood to get the project off the ground as quickly as possible. With a price of copper above $5/lb, Copperwood’s payback timeframe is less than two years.

So how does this situation affect Keweenaw?

Today, besides the 200k to 400k the company receives as lease payments, it has no effect at all. In fact, Keweenaw’s management repeatedly states the plan is to run the business as if Copperwood will never come online. Clearly, this is not the hope but only the mindset.

But for us, let’s look at what Copperwood coming online could mean for Keweenaw as an investment.

Highland’s 2023 feasibility study projects that Copperwood would produce 30,000 tons of copper per year. Keweenaw holds the minerals rights to 80% of the Copperwood project and owns a 2-4% sliding scale royalty via its agreements. At a copper price of $4, the scale adjusts to its high range of 4%.

Let’s say that Copperwood does in fact produce 30k tons which means Keweenaw’s share would be approximately 24k tons. Assuming a copper price of $4 and a 4% royalty, we see that Keweenaw could collect $7.7 million in royalties. If 100% became free cashflow, it would be a yield of 24% on a $32 million market cap. This is a clearly a best case scenario with regard to Copperwood royalties, but doesn’t take into account other income streams, and other ways Keweenaw’s management may choose to deployed its cash.

Conclusion

All in all, Keweenaw Land Association is a fascinating situation to watch but didn’t warrant us deploying cash. Especially since the hurdle rate from our top ideas discussed in other episodes is so high. But who knows, the situation could change, and that’s why we’ll continue to track Keweenaw and provide updates as they arrive.

With that we’ve wrapped up yet an another episode of the show. Thank you so much for showing your continued support though your comments, emails, and by liking and sharing our Substack articles. Thank you and we’ll see you again in two weeks with the next episode.

Share this post