Welcome to Episode 117 of Special Situation Investing.

Before we start, I’d like to throw out a few disclaimers about today’s topic.

The St. Joe Company is much more widely followed than the typical micro-cap stocks discussed on the podcast. While it’s no Amazon or Nvidia, you can still find great summaries of the business on Seeking Alpha, Value Investors Club and other go to value investor websites. Next, our typical ten minute, weekly podcast format isn’t long enough to cover everything required in order to gain a solid grasp of the company’s history, financials and future prospects. Given that the company is widely covered in other write-ups, and that it’s too diverse to cover completely in our short weekly reports, I will attempt to offer just enough of an introduction to act as a starting point for your own research and to provide a slightly different take on the engine behind it’s recent growth than that taken by other investors.

Now with those disclaimers out of the way, let’s jump into the topic at hand.

Company History

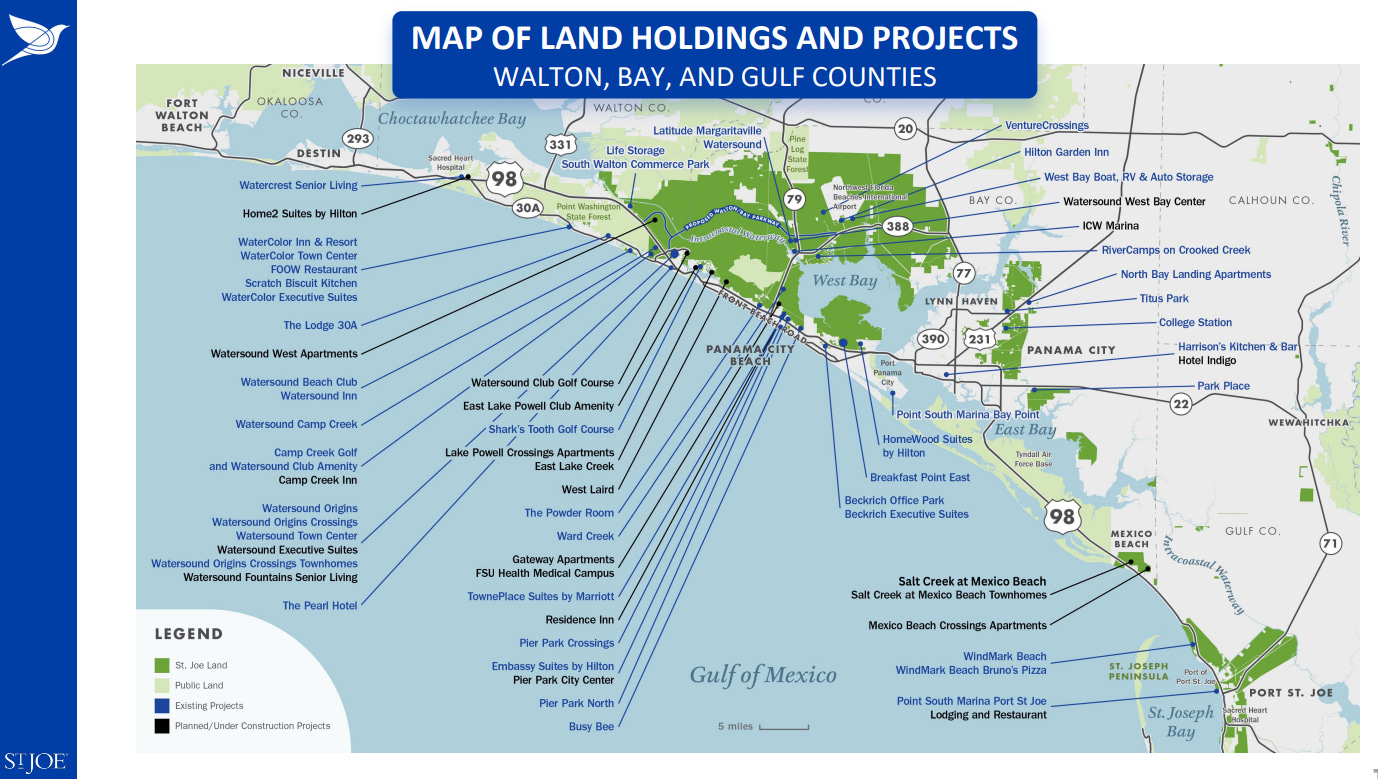

Founded in 1936 by Alfred DuPont, The St. Joe Company went through multiple iterations over the ensuing nine decades, including: a paper mill, sugar producer and timber sales. At its founding, the company held over a million acres of land and was the second largest landholder in the state of Florida. Today, the company holds close to 170,000 acres of land between Tallahassee and Destin, with 71% of the land located with 15 miles of the Gulf Coast.

Today, St. Joe engages primarily in real estate development, selling limited parcels of land only when it supports the company’s broader objectives. Rather it focuses primarily on creating recurring revenue through their existing land holdings. Even though real estate development would have been a logical strategy in years past, the company only fully committed to that strategy following the appointment of Jorge Gonzalez as CEO in 2015. Between the company’s paper mill, sugar production and timber sale years and its recent transition to real estate development the company generated most of its revenue from direct land sales.

Perhaps the most famous past example of a St. Joe’s missed property development opportunity came in the 1960s when, as the story goes, Walt Disney himself approached then CEO Edward Ball with a proposal to develop his Disney World theme park on St. Joe’s land. According to legend Ball kept Mr. Disney waiting outside his office for several hours only to have his secretary hand Disney a note at the end of the day which read “we don’t deal with carnival people.” Whether truth or fiction the story does typify St. Joe’s poor approach to land development prior to Mr. Gonzalez appointment as CEO.

Valuation Drivers

Before we get too far into St Joe’s history, it’s worth touching on what interested me in the company in the first place and what the main points are that make the company so valuable. I’d heard of the company before and even had a sense that it was a real estate business but I had never been interested enough to do any further work. That changed last week when I listened to Episode 41 of The Richer Wiser Happier Podcast where William Green interviewed Bruce Berkowitz CIO of Fairholme Capital Management. This was the first Berkowitz interview that I’d heard and I was struck by his grounded no-nonsense approach to investing. While he didn’t exactly provide a numbered list of St. Joe’s valuation drivers during the interview, he did hint at the drivers in a roundabout way. Here are some of the drivers that stood out to me both in the interview and in my further reading about the company:

1. Geography and land ownership

2. Property development flywheel

3. Demographic tailwind

4. Leadership

Geography and Land Ownership

Beginning with geography and land ownership, the company owns about 170,000 acres of land with 71% of the acreage located within 15 miles of Florida's Gulf Coast. The land stretches between the towns of Tallahassee and Destin, Florida with the largest concentration in and around Panama City. The beaches themselves are a draw for tourists as they offer clear water and beautiful white sand that contrasts with the less desirable gulf coast beaches of Alabama, Mississippi, Louisiana, and much of the Texas coast. The Mississippi river delta in particular makes for less favorable beach conditions to the west of Florida which, again, reinforces the value of St. Joe’s coastal land.

The elevation of St. Joe’s land is an added benefit to the properties’ location. With Florida itself being the second lowest-lying state in the U.S., any amount of elevation is highly protective against storm surge and other weather-related risks common to coastal areas and perhaps even more important given the eastern United States’ vulnerability to seasonal hurricanes. At 345 feet, Britton Hill, Florida’s highest point, sits about 50 miles north of Destin along the Florida-Alabama border and much of St. Joe’s land is similarly situated in the relatively elevated portion of Florida’s pan handle.

I say relatively elevated knowing full well the ire that statement might draw from readers but here me out. Significant portions of humans enjoy living in coastal areas and any casual review of real estate valuations will testify to that fact. Furthermore, all coastal properties are susceptible to damage from erosion, weather, salt, flooding, tidal waves, and the list goes on. Yet people continue to live in these places. So any amount of elevation or other protective attributes inherent to a property are beneficial to the owners even if you can argue that it’s safer to build a house in Ohio. Those who want to live on the beach will do so even when they’re fully aware of the risks and property prices, as well as insurance premiums, testify to that fact. The strong desire of some people to live near the ocean is a tailwind to St. Joe especially considering the topography of its Florida properties.

Property Development Flywheel

Next up we have the company’s property development flywheel. In 2007, St. Joe donated 4,000 acres of land to the state to partner in the construction of the Northwest Florida Beaches International Airport. The larger, modernized airport draws more people to the area with each passing year which increases demand for hotels and the broader hospitality industry. A growing hospitality industry, along with other industry development, draws even more people in and creates demand for new homes and apartments. The growing population generates demand for retail and entertainment venues and the new services in turn attract new tourists and permanent residents. As the flywheel turns the value of the underlying property as well as the rents charged compounds far beyond the value of the outright land sales conducted in the past.

Shifting from a property-sales business model to flywheel-generated recurring revenue in 2015 allowed the company to achieve its second highest revenue year in 2022 second only to its previous record in 2014 but the difference in how the revenue was generated is striking. In 2014, most of the company’s revenue came form a single large and unrepeatable 383,834 acre timber land sale, while in 2022, only 283 acres of the company’s land was sold.

In 2022, the majority of revenue had shifted from outright land sales to recurring revenue streams like commercial leases and club memberships. The earnings driver for today’s St. Joe is rooted in the ever-increasing value density of the land. A beachside shopping center surrounded by upscale apartments, homes, and clubs generates more revenue than could the outright sale of vast empty acres of Florida pine forest. As new amenities, industries, homes, and medical facilities are added to the land the value of future revenues will also rise commensurately.

Demographic Tailwind

Demographic tailwinds also play a role in the value of St. Joe’s land. The lockdowns of 2020 and 2021 fueled an already existing trend for Americans to relocate to Texas and Florida. Both states offer low cost of living, no personal income tax, and an open business-friendly environment which appeals to a broad swath of the U.S. population. The rise of remote work further enabled this transition by enabling geographic arbitrage to segments of the population that previously couldn’t relocate due to in-person work constraints.

Some argue that inflows of people to Florida is a temporary trend but there are reasons to believe the shift may be longer-lasting. If tax and governance issues are driving factors behind some peoples decision to move, then the trend will likely persist for some time as broad-based governance factors tend to remain stable across time especially when those factors are key engines to a state’s economic success.

Furthermore, development itself can be a driver to further development. When would-be Floridians see new infrastructure, new homes, and new industry flowing into an area it tends to draw in even more people who drive more demand for the very same type of growth. With California and New York seeing net outflows to states like Texas and Florida, you can see that just the opposite of Florida’s development is happening in those areas. Infrastructure is aging, companies are moving out, public services are declining in quality and those states are in some ways watching their flywheel run in reverse. All of these demographic tale winds play in favor of St. Joe’s development plans.

Leadership

Leadership is the final driver to St. Joe’s success. Starting off with Bruce Berkowitz founder and CIO of Fairholme Capital Management. I was impressed by the grounded approach he brings to value investing. When asked to comment on other great investors like Bill Ackman, Berkowitz responded that “when it comes to macro and other similar topics he doesn’t really understand what they do, that he sees value investing as figuring out how much cash is in the business and how to pay as little as possible for it.” Certainly there is more to his approach than this oversimplified statement would have us believe but I was struck by the clarity and simplicity he brought to the subject matter that is so often over complicated by others.

Berkowitz Fairholme Fund is over 80% invested in The St. Joe Company, a concentration that generated credulity from multiple interviewers. In defense of this concentration, Berkowitz offers several explanations. The first of which is that he has steadily sold the position for years in an attempt to reduce the fund’s concentration in it but that the stock itself has performed well enough that it continues to dominate their holdings.

Bruce also highlights that he learned a key lesson from his ownership in Sears Holdings. Essentially, in Sears he built up a large position with a simple thesis but did not have control of the investment itself. This left him open to the divergent management perspective of others and ultimately resulted in a less-than-satisfactory investment. With St. Joe, Berkowitz did not repeat the mistake but rather slowly increased his influence within the company and ultimately oversaw the selection of Jorge Gonzalez as CEO in November of 2015.

Reading through St. Joe’s annual reports, and specifically the CEO letters to shareholders, you’re struck with the contrast between Mr. Gonzalez and previous leadership. Prior to Mr. Gonzalez’s first letter, the St. Joe reports read like so many blasé financial documents. No clear sense of the company’s purpose or future plans is conveyed by the document but rather platitudes about macro head winds and other challenges are offered up in place of results. The tone changes, however, as soon as Mr. Gonzalez takes over. Shareholders are now referred to as fellow owners and the company is refocused on compounding shareholder value and thinking like owners.

Of course talk alone is no substitute for results and the company’s stock would likely still be moving sideways today had Mr. Gonzalez not backed his talk up with action. Under his leadership from 2016-2023 revenue grew at an annual rate of 28%. What’s more the company’s corporate and other operating expenses as a percentage of revenue decreased from 24% in 2016 to 9% in 2022 highlighting his focus on keeping costs down and thinking like an owner.

Further demonstrating his commitment to increasing shareholder value, he led the company to repurchase 29.5% of their stock over the last three years knowing that development for developments sake can help a CEO build his empire but may not always be value additive for owners and when further development is not value-additive, its best to return capital through dividends or repurchases.

One additional thing that demonstrated the priorities of management to me was the striking absence of an ESG boilerplate on the opening pages of the annual report and investor presentations. There is nothing wrong per se with ESG statements themselves but they have become for CEOs what Air Jordan shoes were in my junior high days. Nobody really needed them and they didn’t change anything about what you did but you were just a lot cooler if you had them. Open up any report today from an oil company to a drug manufacturer and you’re hit with the obligatory zero carbon emission global equity statement. I may be alone in saying this, but I really enjoyed reading a report from St. Joe’s where management stated clearly what they’re actually doing. They’re trying to build an upscale community near the beach for people to enjoy for generations to come and that’s probably a big enough challenge for any CEO. No need to complicate things by trying to solve the world most intractable environmental, social and governance challenges.

Conclusion

To revisit my opening statement, this company warrants far more analysis than can be obtained from this short write-up. On the surface it doesn’t appear to be undervalued at 40 times earnings, especially when compared to other land-based companies we’ve covered, some of which trade at less than ten times normalized earnings. On the other hand, however, the company does derive most of its current revenue from just 2% of its total land holdings and has years of, as yet undeveloped, home sites pre approved by the state in its development pipeline. Even if the company isn’t undervalued today, we know that knowledge in investing is cumulative. We can apply what we’ve learned about one company to another, or once we’ve familiarized ourselves with a stock, can keep an eye on it and be ready to back the truck up when another buying opportunity comes around.

With that we hope you’ve enjoyed today’s overview of The St. Joe Company. Again we encourage you to read the extensive write-ups on Value Investors Club, Seeking Alpha and others for a more detailed look into the company’s financials. Even if you choose not to invest in the company, the last 15 years of annual reports are worth reviewing if only to see how much difference leadership can make in a company’s direction. Under one management team the company’s asset base shrank year after year with no significant benefit to shareholders while under another management team, the land ownership has remained stable while recurring revenue from that land now generates income that will soon eclipse any past earnings records. There are several great investing lessons one can draw from St. Joe’s recent history and we hope you enjoy exploring the topic further on your own. As always we look forward to bringing you another investment write up next week.

Share this post