You can enjoy the Special Situation Investing Podcast on Fountain or wherever you listen.

“Some of the best situations arise when you can find a General where you can make a significant investment of your own but some other investor is doing the work to improve management’s decision making.” - Jeremy Miller (Warren Buffett’s Ground Rules)

Welcome to Episode 62 of Special Situation Investing.

If you search the web for www.ielp.com you’ll find a very underwhelming website. It has no flashy pictures; no in-your-face, single-word mission statements, no ESG banner displayed front-and-center; but just a few tabs containing information pertinent to investors in a simple blue and white color scheme. We find it an encouraging sign when a company we are researching has what could be considered a terrible, or at least extremely basic, website. It shows that the priority is elsewhere and not on creating an awe-inspiring presence on the web. In the case of this website, we expect nothing less from one of the world’s greatest investors, Carl C. Icahn and his partnership, Icahn Enterprises L.P. (ticker IEP).

While the partnership’s basic website might be an often overlooked plus, the partnership’s massive out performance of the market is legendary.

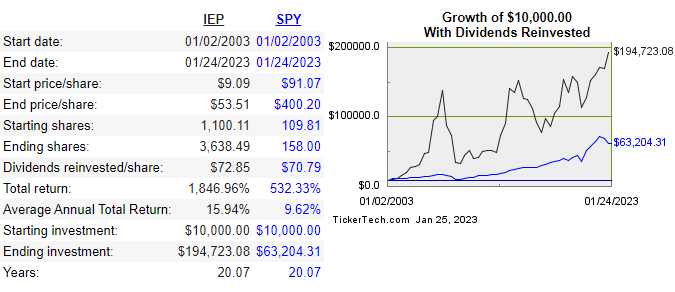

At first glance, just looking at the stock price over time, IEP’s performance appears to be nothing extraordinary. In fact, considering price alone, the stock has lost 15% over the last ten years, massively underperforming the price of the S&P500. But its a different story when considering total returns, including dividends, over a more extended time horizon.

Looking back ten years, for example, with dividends reinvested, IEP has kept pace with the markets, averaging a return of 12.44% vs the market’s 12.60%. These results are shown in the chart below.

The next chart shows that over a longer time horizon of twenty years, while much more volatile, IEP has clearly outperformed the market. It trounced the market’s 9.62% with an impressive 15.94% average annual return.

Icahn and his partnership

Carl Icahn is often compared to Buffett in terms of investment success, and while some can argue whether his skill is comparable to Buffett’s, few can argue that the two men have similar strategies. While Buffett often buys controlling stakes in companies and early on he did use his control to affect management’s decisions, Buffett isn’t considered an activist investor. He prefers to take a more passive role, investing with management he respects, and only flexing his control in extreme circumstances. In contrast, Icahn is known for his skill as an activist investor and often a very aggressive one. In its SEC filings, the Icahn’s partnership explains its strategy in the following way.

[Our] approach focuses on exploiting market dislocations or misjudgments that may result from market euphoria, litigation, complex contingent liabilities, corporate malfeasance and weak corporate governance, general economic conditions or market cycles and complex and inappropriate capital structures. The Investment Funds often act as activist investors ready to take the steps necessary to seek to unlock value, including through tender offers, proxy contests and demands for management accountability.

So what exactly is Icahn Enterprises L.P.?

First off, it’s master limited partnership and it was formed in February of 1987.

According to Investopedia, a master limited partnership (MLP) is a “business venture in the form of a publicly-traded limited partnership. It combines the tax benefits of a private partnership with the liquidity of a publicly-traded company.” As an MLP, IEP does not pay federal income taxes which has implications for any interested investors. So make sure to be well versed in the tax particulars prior to purchasing any MLP security.

Today, IEP is a diversified holding company with subsidiaries engaged in the following seven diversified reporting segments: Investment, Energy, Automotive, Food Packaging, Real Estate, Home Fashion and Pharma. While the Investment and the Real Estate segments each hold many high quality investments, the other sections hold specific companies and investments in which IEP holds a controlling interest. Under Energy there’s CVR Energy; Automotive has, among others, PEPBOYS, AutoPlus, and AAMCO; Food Packaging has Viskase; Home Fashion has WestPoint Home; and Pharma has Vivus. The various segments in the partnership are shown in the diagram below.

Why we’re interested

So, given that brief background into Icahn Enterprises, now let’s talk about why we think it might provide an opportunity for value creation. For full disclosure, neither hosts of this show currently own IEP or either of the two other securities we are going to mention. And honestly, this is not a full recommendation on any of these securities but instead an initial dive into a situation we find interesting.

So what do we find interesting about IEP?

Icahn Enterprises first caught our interest when we found it held in three separate funds run by one of the investment managers we most respect. Not only that, but it was a concentrated holding in one of the funds. Naturally that caught our interest. So perhaps more than coattailing Carl Icahn, we are coattailing this other investor for whom we have so much respect. While blindly buying anything because someone else owns it is foolish, paying attention when someone you follow and respect acts with conviction is just plain common sense.

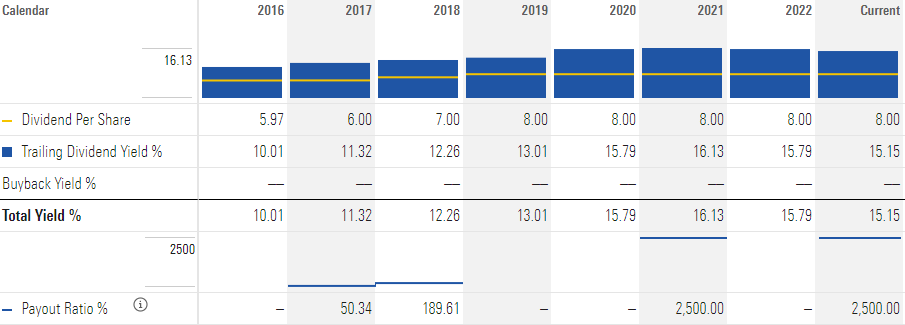

Upon our own initial research into the company, one thing that popped out was IEP’s 15% dividend. While it’s not uncommon to see such a large dividend on some hardly followed, small resource stocks, a dividend of that magnitude on a well known investment holding company was unexpected. We took a look to see if this was a onetime fluke but found that IEP has a history of high dividends for more than ten years and its been over 10% since 2013. This dividend has contributed to much of IEP’s performance. For example, in 2022 when the S&P500 was down nearly 19%, IEP’s stock price was basically flat for the year, but it’s total return was just under 13%.

Source: morningstar That leads us to the third reason IEP caught our attention. As previously mentioned, Icahn Enterprises, over the long-term, has handily outperformed the market. If you need a memory jogger, review the two charts at the beginning of this article.

Our forth reason, is that, similar to Buffett’s current investment portfolio, IEP has a high concentration in energy companies. If you’ve listened to more than a couple of our episodes, you’ve probably picked up on that we’re long-term bullish on natural gas and oil. (For more on that topic check out our episodes: Oil Ain’t Toast, Texas Pacific Land, PHX Minerals, and Chesapeake Granite Wash Trust.) Icahn is invested in CVR Energy, an oil refinery company, Occidental Petroleum, an oil and gas producer, Cheniere Energy, the premier US LNG producer and transporter, and finally, Sandridge Energy, another oil and gas explorer. We don’t know the future but it peaked out interest further seeing high conviction bids in a sector we believe will surprise to the upside in the coming decade.

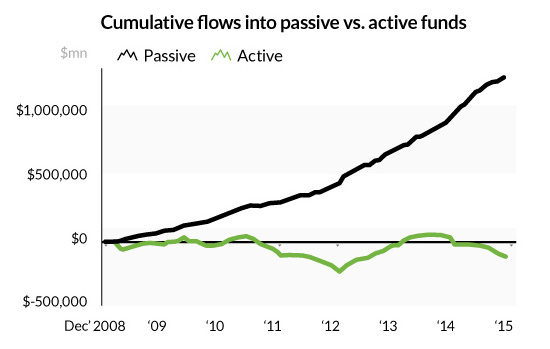

The fifth reason we find an investment in Icahn Enterprises intriguing is another macro trend we believe is likely to play out over the next decade. This is a move away from passive index investing in favor of active investment vehicles. The chart below shows cumulative flows of dollars into active vs passive funds and it shows that, at least since 2008, more and more dollars have been flowing into passive funds and passive investment vehicles at the expense of active managers.

Source: visualcapitalist While not all trends reverse or revert to the mean, we believe the environment responsible for the success of passive investing ended in 2020. Low inflation, ever lower interest rates, increasing globalization, falling corporates tax rates, and decreasing commodity prices, these were all trends that played out over the last forty years and produced the longest bull market in US history. All anyone needed to do was to passively buy the S&P500. It was that simple. All of those trends now seem to have reversed, slowed or stagnated. It’s a sea change.

The renown investor, Stanley Druckenmiller was recently recorded saying: “There’s a high probability in my mind that the market, at best, is going to be kind of flat for 10 years, sort of like this ’66 to ’82 time period.” The interest in active managers is likely to increase if that’s anything close to what the next decade has in store.

Our sixth reason for interest in Icahn Enterprises is that, even over those of other active managers, Icahn’s investment style and skill could prove a huge advantage in a world where it takes more than just dollar-cost averaging into the S&P500 to produce solid returns.

In Episode 60, where we reviewed Jeremy Miller’s book Warren Buffett’s Ground Rules. We discussed how Buffett used Workouts, or what we call special situations, and Controls, which were investments where he owned a controlling stake, to produce outsized returns in sideways and even down markets. In the case of Workouts, returns do not depend on market movements but are created through corporate actions such as spin-offs, mergers and major acquisitions. On the other hand, Controls can often produce returns above the market because the controlling stake can be leveraged to make a special situation happen, forcing value creation.

Carl Icahn is known for being an aggressive and highly successful activist investor. As quoted above, through IEP, Icahn and his team “act as activist investors ready to take the steps necessary to seek to unlock value, including through tender offers, proxy contests and demands for management accountability.” So even in sideways and down markets, Icahn’s investing repertoire can produce solid returns. Returns for which people pivoting from passive investments could be hunting.

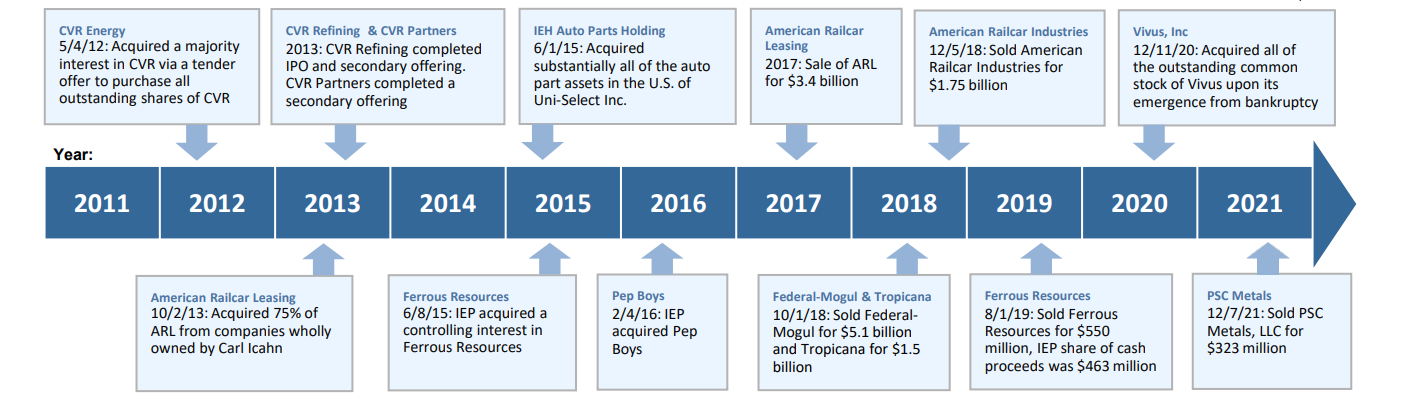

Just as an example of Icahn’s value-unlocking tactics, take a look at the he chart below. It lists the acquisitions and divestitures within IEP from 2011 to 2021 and demonstrates his success in acquiring undervalued assets and improving them before ultimately selling them for a profit. In 2017, American Railcar Leasing was sold for a $1.7 billion profit. In 2018 Federal-Mogul was sold for a $251 million profit and American railcar Industries was sold for a gain of $400 million. And finally, IEP sold Ferrous Resources in 2019 for a gain of $252 million and PSC Metals in 2021 for a profit of $163 million.

Source: ielp.com And as a more current example, if you go to insidearbitrage.com, which is one of the three websites we use to track upcoming spin-offs (view our Reading tab on the homepage of our Substack for links to all three websites), you’ll see that two of IEP’s investments, Southwest Gas Holdings and CVR Energy have recently announced spin-offs. It’s likely that given his stakes in both companies, Icahn is a diving force behind these corporate, value-creating events.

Conclusion

So those are our seven reasons why it might pay off to coattail Carl Icahn. There are currently three possible ways to invest in the thesis if so inclined. The first is buying IEP directly, the other two ways are by participating in the spin-offs of either Southwest Gas Holdings or CVR Energy. Once again a word of caution, since IEP is a master limited partnership, its cash distributions are not considered qualified dividends and there would be tax implications to take into account. The same holds true for the company that is potentially going to be spun out of CVR Energy—CVR Energy Partners. As always, be sure to fully understand what you are buying before you buy it.

With that, we’ve wrapped up another episode of Special Situation Investing. Thanks for all the support and feedback you all have been sending our way. Thanks for using the Fountain app to listen to the show and for sending us bitcoin boosts through that platform. Your support is much appreciated and confirms that the effort we put into creating these episodes is enjoyable and educational for you, our audience.

Another way you can show your support is by going over to Substack and becoming one of our free Subscribers.

Alright, we hope you all are learning as much from these episodes as we are by creating them. We’ll be back again next week.

SUBSTACK-ONLY BONUS

Back in Episode 37 we took a look at Jefferies Group’s up-coming spin-off of Vitesse Energy. On January 17, the spin-off was completed. Our main interest in the spin-off was the potential for forced selling since the company is much smaller than Jefferies and it is in the oil and gas sector. So far there is no evidence of forced selling. For a great review of the situation, take visit the Yet Another Value Blog Substack article linked below.

Share this post