Welcome to Episode 106 of Special Situation Investing.

It’s incredible how quickly time passes. Each moment that ticks by makes the current one more precious. In one of our pieces, titled Wealth is the Control of Time, we argued that time is the scarcest resource and thus the control of one’s time is the measure of true wealth. After all, for each of us, time is not only scarce, it is increasingly finite. Thus the question we must answer on a daily basis is how to use our limited time.

This oddly philosophical introduction was prompted by the recent passing of a dear friend, a friend we all know—Charlie Munger. Although my cohost and I never met Munger personally, his death stung both of us as if he were a close friend or relative. In a way he was. I’m sure you can relate.

Munger gave us all so much. Not least of which was a vivid example of a life well lived. Thanks, Charlie.

The Updates

Speaking of time passing, it’s been almost three months since we published a “portfolio update” piece. We use these pieces to summarize updates from quarterly reports and earnings calls of some of the highest conviction companies in our portfolios. The goal is to record highlights from multiple companies in a succinct format that acts as a journal, capturing our thoughts on these companies’ progress for future reflection. We hope you find these updates valuable.

With the Q3 earnings season in the rearview mirror, it’s time to review some highlights. Let’s dive in.

Natural Resource Partners

NRP’s Q3 earnings call had no questions from analysts. Zero. Either the company’s results and future plans are predictable or no one is paying attention. We’d argue both are true.

We were happy with the company’s results. NRP produced $80 million of FCF in Q3 resulting in $304 million FCF over the TTM. Fifty million was allocated toward retiring the company’s outstanding 12% preferred shares, leaving only $72 million left to redeem. This makes $178 million total preferred shares retired year-to-date which will save the company $20 million in preferred distributions over the coming year. Additionally, 1.46 million warrants were retired for $56 million and now only 1.54 million warrants remain outstanding.

All told, quarter-over-quarter, total debt obligations were reduced $60 million. The current total stands at $325 million.

The chart above shows debt increased slightly over the quarter but total obligations continued to decline. This is because the company used lower interest rate debt to pay off some of its 12% preferred shares.

Looking ahead, at the current rate of $60 million per quarter, the company could reach its goal of zero obligations in less than six quarters. The company is seeing the light at the end of the tunnel of what has been a nine-year process to deleverage and derisk the company’s balance sheet. As management reminds us every quarter:

The goal is to pay off all permanent debt, redeem all preferred equity and settle all warrants in order to maximize long term free cash flow available for common unitholders.

We continue to believe the market is missing the NRP’s potential.

NRP has two levers for value creation over the next eighteen months. The first is continued debt reduction. For a primer on how this creates value, listen to how Stephen Bregman of Horizon Kinetics explains it in the following quote:

Debt reduction in a leveraged company is a phenomenon that has enriched many real estate and leveraged buyout devotees. The idea is that the enterprise value of a public entity, which is the sum of both its stock market value and its debt, is settled upon by the market. Let’s say that the market determines that a certain company’s enterprise value, in light of its level of operating income and degree of leverage, should be about $1 billion. Of that $1 billion, let’s say that debt is $650 million and the market cap is $350 million.

What happens if the company uses its earnings one year to pay down $65 million of the debt, which is about 10% of it? Well, if there are no other changes, then the enterprise value is $65 million, or 6.5% lower. Which means that the company just got cheaper, as if it were being penalized for reducing its leverage and financial risk, and even though its earnings improved via reduced interest expense. What should happen is that the equity market value rises by a comparable $65 million, in which case the enterprise value remains constant. There’s an academic term for this phenomenon, which describes what should happen in principle, and of course it also happens in practice.

Importantly, though, in this case the $65 million increase in equity market value occurs on a stock market cap of only $350 million, whereas the debt was $650 million. That would be a counterbalancing 19% increase in the stock market value of such a company for a 10% reduction in the debt. That can be a very powerful engine of share price return over a period of years, irrespective of any increase in revenues or other sources of earnings growth and irrespective of a higher valuation perhaps accruing to the stock.

So the simple reduction of debt will create value for NRP’s unit holders.

The other lever that will play out over the next year and a half is an increase in distributions. Remember, management’s end goal is to maximize cash flow available to unit holders. Currently the company pays out only $39 million to its unit holders, or $0.75 per unit per quarter. Consider a simple example where in 18 months, NRP’s free cash flow has fallen 33% to $195 million but the company is debt free. The company could still payout a distribution that’s five times what it pays today. Hypothetically, this could lead to a corresponding 5x in the stock price.

Before we leave the topic of coal companies, we wanted to share this quote from Mohnish Pabrai about his recent investments in coal. After an in-depth discussion about his successful investments in the country of Turkey, Pabrai conclude by saying:

My take is that if I look at our allocations today, probably half, maybe more than half is sitting in Turkey. Then we have another 20% or more, maybe 25% now sitting in coal. Coal is a four-letter word in the US. We will make more on coal than we made in Turkey because people are stupid. What I'm saying is I'm looking for no-brainers. I'm looking for places where there is a lot of irrational hatred and irrational behavior. Then we hone in on things that I can explain in three sentences. So that's what we do.

Pabrai is fun and educational to listen to, so we suggest you check out the entire interview.

Natural Resource Partners is an ignored and hated no-brainer. We are happy with its continued progress and bullish on its future.

Mesabi Trust

Another company that made substantial progress in Q3 is Mesabi Trust. Our last quarterly portfolio update shared how iron ore production on Mesabi’s land was ramping up to a normal rate after a year-long protest had stopped all production. The numbers for Q2 showed iron ore production 77% below its average. We hypothecated that Mesabi Trust would distribute a dividend in the Q3, the first time in over a year.

That’s exactly what happen. The trust distributed a dividend of $0.35 per unit on 20 November. In addition, the amount of iron ore produced on Mesabi’s land crossed the six-year quarterly average—approximately 1 million tons—with the total tonnage coming in at 1,049,281 tons.

The chart above plots production on Mesabi’s land and its quarterly dividends. While volatile, MSB’s average quarterly dividend over the past six years is $0.70, nearly twice the Q3 dividend it just distributed. So we are happy with reinstated dividend and we believe there is further upside to come, at least in the dividend. We remain bullish short-term on this company and even more so long-term.

As a reminder, check out Mesabi’s strong performance, with dividends reinvested, vs the S&P 500 over the last twenty-nine years.

Permian Basin Trust

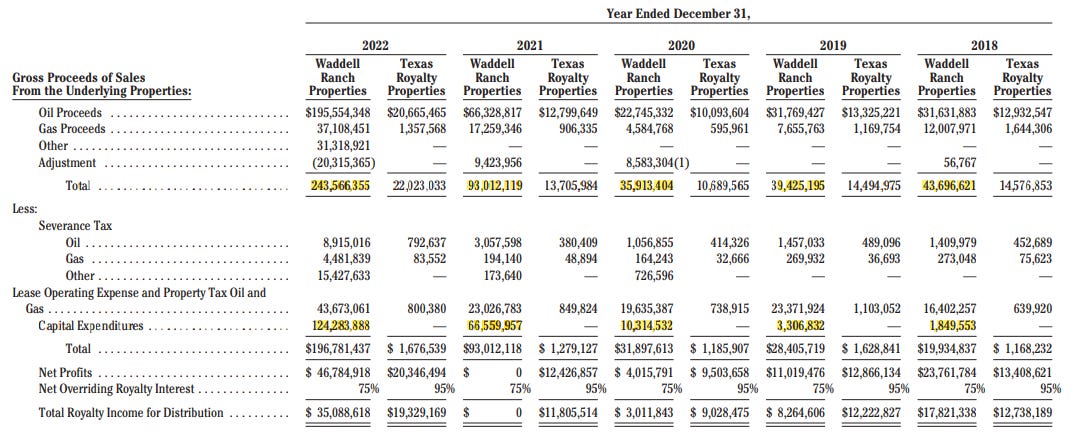

For the quarter ended September 30, 2023, royalty income received by the Permian Basin Trust was $3,317,431 compared to royalty income of $27,323,759 from the third quarter of 2022. At first glance, things don’t look great. An initial thought might be to chalk up the decrease to lower oil and natural gas prices, but that would only be partially correct. The bigger story remains the extensive expansion project at the Trust’s Waddell Ranch property. Check out our piece dedicated to this company for background if desired.

As it has for the past few years, the Trust continued to pour millions of dollars into capex to increase the property’s production. To grasp the scale of this capex and the massive impact it’s having on production, check out the highlighted sections in the table below.

From 2018 to 2022, gross proceeds from gas and oil sales out of the Waddell Ranch, specifically, increased 5.6x from $43 million to $243 million. This massive growth in production occurred as a result of an increase in capex from $1.8 million to $124 million over the same period, up an incredible 67x. Compiling data from the last three quarterly reports, year-to-date, the Trust allocated $96.7 million to capital expenditures at the Waddell Ranch. At this rate, the company will likely match last year’s $124 million in capex for the entire year.

It’s still our conviction that, firstly, capex investments will continue to increase production out of the Waddell Ranch and, secondly, that in the next couple years, capex will decrease dramatically. As this occurs, FCF available for distribution to unit holders will rise sharply. Consider that with a current market cap of $785 million and an trailing dividend slightly over 3%, PBT only distributed about $25 million this past year. If it didn’t have capex requirements, it could have distributed 6x that amount, or about 19% of its market cap.

Given that we are long-term investors and we consider a couple years a short time horizon, we are excited to keep adding to this position.

Conclusion

With that, we wrap up another weekly episode of the show. Thank you all for your continued support and interest. We particularly want to thank

of Base Hit Investing and Aaron Pek of Value Investing Substack for recommending our Substack to their readers. Between the two of them, they’ve sent hundreds of new readers our way. Thank you, gents. If you enjoy our work and find it valuable, and have a Substack of your own, we’d be honored if you’d consider recommending our work to your readers as well. Thanks!We’ll see you all next Saturday on the next episode.

Share this post