Welcome to Episode 90 of Special Situation Investing.

To kickoff today’s piece, we have a quote by Stephen Bregman. As one of the cofounders of both Horizon Kinetics LLC and FRMO Corp, Bregman made the following statement about spin-offs during one of FRMO’s conference calls almost a decade ago. He said:

There’s a new phenomenon in the world of spin-offs that differs significantly from the typical approach that we’ve seen in the past. Every spin-off is a divestiture. Historically, in a spin-off transaction, the parent company would spin-off a division or an asset that wasn’t recognized by the market, that wasn’t well understood by the market, or that might even have been tangential to the basic thrust of the parent company. Now, the thematic structure—if you could say that it has a theme—in the spin-off arena is that the business being spun off is not necessarily tangential, undervalued, or misunderstood; it’s just that it happens to have a meaningfully lower margin than the parent business.

Think of it this way: imagine a university classroom with 10 students. Somebody’s going to be the worst student. If you expel that student from the class, the average grade goes up, but is the average grade really higher? Mathematically, it is, but it’s not as if the average student learned more; it’s just a different way of calculating. This is really what’s happening in the world of spin-offs.

What was a phenomenon in 2015, seems to be commonplace today. In more than a few episodes, we highlighted companies that appeared to be pursuing a spin-off for just the reason Bregman noted—jettisoning lower-margin segments and subsidiaries to boost the margins of the parent company.

One area of the market this plays out regularly is in regulated energy space. The motivation for these companies in particular is often twofold: 1) increasing margins of the parent company by cutting loose a lower-margin segment, and 2) removing the unpredictability of an unregulated business so the parent company can earn a higher multiple in the market. A few recent examples are Exelon Corporation spinning off its nuclear energy segment, Constellation Energy; MDU Resources spinning off its construction services segment, Knife River; and Southwestern Gas spinning off its infrastructure services subsidiary, Centuri Group.

Last September, in Episode 40, we discussed MDU Resources (MDU) and its then proposed spin-off of its subsidiary Knife River (KNF). Today’s piece looks at the results of the completed Knife River spin-off and introduces the recently announced separation of MDU’s Construction Services Group segment.

MDU Resources background

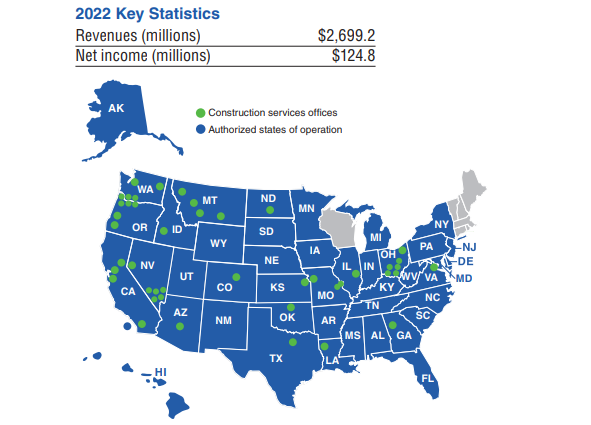

As it sits today, MDU Resources Group is a conglomerate with operations in all fifty US states that employs approximately 15,000 people. The company is comprised of three distinct segments: electric and natural gas utilities, natural gas pipelines, and construction services.

If anyone wants further background on MDU prior to diving into the two special situations, check out our previous piece, the company’s website, or its latest annual report.

Given that MDU was comprised of four distinct segments, two regulated and two unregulated, it was a prime candidate for spin-offs. It’s a case where the potential for both higher margins and a higher multiple for the parent company applies. In fact, back in late 2022, MDU’s management clearly stated its goal was to become “a pure-play regulated energy delivery business.” With the recent spin-off of the Knife River, the goal is halfway complete.

The Knife River spin-off

On May 31st, Knife River Corporation successfully completed its separation from MDU Resources Group. The new company traded on the NYSE for the first time on June 1st under the ticker KNF. The separation occurred through a pro rata distribution of approximately 90% of the outstanding shares of Knife River common stock to MDU Resources shareholders. The parent company owns the remaining 10% stake. MDU Resources shareholders retained their shares of MDU common stock and received one share of KNF common stock for every four shares of MDU common stock held as of May 22, 2023.

As with most spin-offs, there were two ways to play a bullish thesis on Knife River; buy MDU before the spin or KNF after the spin. While we came up short of an outright recommendation, in our earlier piece, we indicated the combined MDU and KNF would likely trade at a higher total valuation than MDU did prior to the spin. Part of the reasoning behind this conviction was we didn’t foresee Knife River experiencing the indiscriminate selling that some spin-offs do.

One reason a spin-off can experience indiscriminate selling is when its market cap is much smaller, usually orders of magnitude smaller, than that of its parent. When this is the case, certain investors may be forced to sell if the spin-off falls below a minimum market cap requirement. This was not likely the case with KNF as MDU’s market cap was about $6 billion and KNF was spun-out with a market cap of about $2 billion.

Another common cause of indiscriminate selling of a spin-off is when the parent company is in an index but the spin-off doesn’t meet the inclusion criteria. Most often this is also caused by differences in market capitalization. But regardless of the specific reason for exclusion, any investors holding the parent company simply because it was in the index would be forced sellers of the spin-off. Once again, this did not apply in Knife River’s case because, immediately upon separation, Knife River joined MDU as a member of the S&P MidCap 400.

A third reason spin-offs often experience selling pressure is when it is simply unwanted for any myriad of reasons. Some reasons we’ve seen in the past include: the spin-off is in a hated sector such as oil and gas or firearms, the spin-off is loaded with the parent company’s debt, and lastly, the spin-off is in a totally different sector than the parent company. As none of these reasons really applied, and there were no other warning signs of indiscriminate selling, we were inclined to think KNF had a good chance of trading flat to up immediately after separation.

Therefore, for these reasons and others, buying MDU before the spin was thought to be the preferred way to play the situation. So how has it worked out? A look at the charts of both MDU and Knife River’s market caps is instructive.

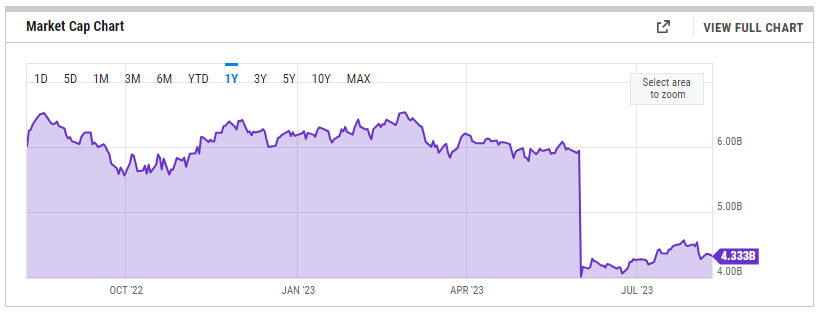

The chart below shows a drop in MDU’s market cap when Knife River was separated. From just under $6 billion it fell to approximately $4 billion. This is perfectly normal as MDU adjusted to losing $2 billion in value ascribed to Knife River. In the weeks that followed, MDU didn’t sell off but increased slightly to a market cap of about $4.3 billion.

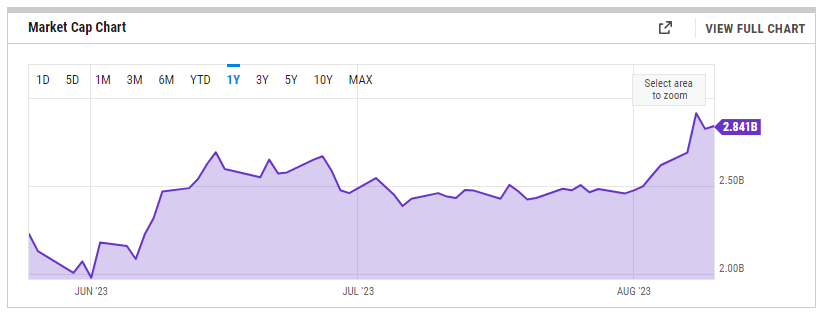

What’s more interesting, is to see what happened to KNF as shown in the next chart. This chart shows, that post spin-off, KNF increase from a market cap of $1.8 billion to $2.8 billion as of this writing. Definitely no sell off there. The combination of the separated companies is trading at a valuation of $7.1 billion, which is higher than MDU’s $6 billion prior to the spin-off.

To calculate the returns for an investor who bought MDU prior to the spin-off requires a bit of simple math. There are two ways of going about this calculation, one using market caps and the other using the stock prices. Here’s the method using the stock prices:

For illustrative purposes, suppose four shares of MDU were bought on the date of record, 22 May, at a price of $29.85 for a total cost of $119.40. As of this writing, MDU’s shares trade at $21.19, so those four shares would now be worth $84.76. But in addition, one would also now own one share of KNF worth $50.16. Today’s total combined value is $134.92, 13% higher than the initial investment.

On the other hand, if one was only interested in owning Knife River and had bought it on its first trading day, that investment would be up 43%.

The above calculations show that although buying before and after the spin-off could have both proved lucrative investments, so far, Knife River alone was the better play. Of course results will vary depending on purchase date and price and time will also change the results. One factor supporting the long-term prospects of an investment in MDU is its recent announcement that it plans to separate yet another of its segments.

The Construction Services separation

MDU issued a press release on July 10th which announced its decision to pursue a tax-advantaged separation of its other non-regulated segment—Construction Services Group. In order to meet its goal to become a “pure-play regulated energy delivery business” it makes sense that MDU would have to get rid of its remaining non-regulated segment. So, this latest move was not surprising. In fact, back in September of last year we said:

The potential for additional spin-offs exists as MDU will still be composed of three independent segments. The most likely spin-off candidate is its unregulated Construction Services segment.

Although we were spot-on about the possibility of the Construction Services Group (CSG for short) being next on the chopping block, we were a bit forward-leaning in predicting it would be a spin-off. In the press release announcing the separation and in the most recent conference call, management reiterates that both the timeline and exact method of separation are still to be determined. But regardless of the exact how and when, Construction Services Group’s days as a part of MDU are clearly numbered.

So what exactly is Construction Services Group? Here’s how MDU summarizes it in its annual report:

MDU Construction Services Group provides a full spectrum of construction services through its electrical and mechanical and transmission and distribution specialty contracting services across the United States. These specialty contracting services are provided to utility, manufacturing, transportation, commercial, industrial, institutional, renewable and governmental customers. Its electrical and mechanical contracting services include construction and maintenance of electrical and communication wiring and infrastructure, fire suppression systems, and mechanical piping and services. Its transmission and distribution contracting services include construction and maintenance of overhead and underground electrical, gas and communication infrastructure, as well as manufacturing and distribution of transmission line construction equipment and tools.

One thing worth highlighting about CSG is its recently been bringing in record revenues. In its separation announcement, MDU says it “expects additional project opportunities to result from the federal Infrastructure Investment and Jobs Act and the energy transition underway in the U.S.” As one of the largest construction services in the country, CSG currently can’t keep up with all its projects as it is. As of this last quarter, the segment was sitting on $1.94 billion of projects backlog.

As it was when we initially wrote up the Knife River spin-off, there’s a lot of information about this new separation yet to be determined and distributed. As always we’ll keep our eyes on it and send out updates as required.

A fascinating development

Before wrapping up, we wanted to share an unrelated development we found quite fascinating.

As we’re sure many of you do, we closely follow the 13F filings of of our most admired investors. One individual who sits near the top of our favorites list is Mohnish Pabrai. So we were pleasantly surprised when his latest filings released on Friday showed that he had allocated over $70 million between two coal producer companies. In fact, he had also sold out of all his other U.S. stock positions, and now the only US stocks he holds are Alpha Metallurgical Resources (AMR) and CONSOL Energy (CEIX).

This development was encouraging because we have been writing a lot about coal and companies within that industry. We believe they offer great potential returns. While we won’t reiterate our bullish thesis again here, you can find all of our coal related pieces in the list below (from most to least recent). Happy reading!

Coal’s Resilient Future (LINK)

The Cannibal Coal Company—CONSOL Energy (LINK)

Another Look at National Resource Partners (LINK)

A Coal Royalty Company—Natural Resource Partners (LINK)

With that we’ll wrap up this edition of Special Situation Investing. As always we want to thank you all for your involvement through your comments, shares and likes. We particularly enjoy the increased interaction with more you in the comments. Please keep this up and let us know where we’re wrong or, on the off chance, where you found our research helpful. With that, thanks for reading and listening and we’ll be back in seven days with the next episode.

Top content from last week

This was an incredible interview with Doomberg. Check it out!

Share this post