Welcome to Episode 80 of Special Situation Investing.

Today we’re going to take a second look at a situation introduced back in Episode 76 titled Shadowing David Einhorn.

As a reaction to recent talks from Einhorn and changes in his portfolio, we wrote we believe he’s made a shift in his investment strategy; one worth paying attention to. Moving away from buying cheap stocks expecting the market will eventually catch on and bid the price higher, he now seems focused on two strategies: 1) buying stocks with low PE ratios that can produce high returns via dividends and buybacks alone, and 2) buying stocks that are attractive M&A targets on a reserves-to-market-cap basis.

In that piece, we spent the majority of our time time discussing the cheap-on-a-market-cap basis side of the equation and argued Southwestern Energy is likely an example of a company Einhorn owns for this reason. Our original intent was to follow up with a deeper dive into Southwestern Energy. But as often happens, our curiosity led us down a different rabbit hole, to a company that falls within Einhorn’s first category—cheap companies with large dividends and/or buybacks.

Nine days after Shadowing David Einhorn was posted, Einhorn’s 13F filings dropped. We were interested to see if the position in Southwestern Energy had increased. The results are shown in the image below.

What we found was that the position in Southwestern Energy was roughly unchanged, down less than one percent. But on the flipside, Einhorn’s number two position—CONSOL Energy—had increased by fifty percent and is now 8.6% of his portfolio. This display of high conviction was not lost on us and we decided to research this company instead.

The company

Let’s begin by taking a look at the company’s long and colorful history.

CONSOL was founded in 1860 when several Maryland coal operators decided to combine or “consolidate” their holdings under a single company called the Consolidation Coal Company. To emphasis just how old this company is, consider that although it was founded in 1860, operations of the company were delayed until 1864, commencing upon the end of the Civil War.

In the 1930’s CONSOL, or at that point, Consolidation Coal Company, almost went bankrupted due to the effects of the Great Depression but it was able to survive by restructuring.

After World War Two, a merger caused the company to change its name to the Pittsburgh Consolidation Coal Company.

About twenty years later, and in the wake of the 1973 energy crisis, the company sought to capture a greater share of the growing seaborne steam and metallurgical coal market. To do so, the company built what would become the largest underground mine in North America. This mine remains CONSOL’s prime asset today.

In the 1990’s, CONSOL built a business around the long-standing safety practice of removing coal bed methane from the ground prior to mining. Essentially, CONSOL became a multi-fuel energy producer, producing both coal and natural gas. And to close out the millennium, CONSOL went public in 1999.

CONSOL continued its pursuit of natural gas by creating a separate company, CNX Resources, and by acquiring the exploration and production assets of Dominion Resources Appalachian Basin. In 2017, the two company’s formally split and became separately traded public companies—CONSOL Energy and CNX Resources.

Today, CONSOL Energy possesses some of the highest quality coal assets in the world with the largest underground mining complex in the United States—its Pennsylvania Mining Complex. The complex consists of three individual mines spread out primarily across the Greene and Washington counties of Pennsylvania. As mentioned previously, this complex is CONSOL’s primary asset, producing about 28 million tons per year. Between the three mines within the complex, CONSOL reports coal reserves of 622 million tons.

The Itmann Mine, is a lesser asset compared to the Pennsylvania Mining Complex but important from the standpoint of resiliency and diversification. Development on the this mine began in early 2020 and its reserves are estimated around 28 million tons with an expected annual production rate of about 166 thousand tons. A fact about both mines that we were glad to come across is that both workforces are non-union.

The Baltimore Terminal is CONSOL’s third major asset. This is a seaport terminal strategically located in Baltimore, Maryland. This asset allows CONSOL direct access to seaborn shipping routes to export its coal. The facility has an annual throughput capacity of 18 to 20 million tons. All of the coal from CONSOL’s complex passes through this terminal. Additionally, due to also processing third-party coal, the complex has maintain over $40 million in EBITDA over the last five years.

Hopefully that bare-bones summary of CONSOL’s history and current assets is enough to provide context as we dive into CONSOL’s current state and why we believe it’s a situation worth exploring further.

The situation

As alluded to earlier, we believe CONSOL Energy fits into the category of a cheap company able to provide outsized returns simply via dividends and/or buybacks.

The current situation is summarized by CONSOL’s CEO, Jimmy Brock, in the press release announcing the company’s first quarter results. We’ll read his quote and then break it down. He said:

During the first quarter of 2023, we delivered a very strong performance, producing more than 7.1 million tons and generating over $220 million in free cash flow. Due to this strong free cash flow generation, we were able to retire nearly $100 million of our outstanding debt, while returning $104 million of cash to our shareholders. The majority of our shareholder returns in the quarter were deployed towards repurchasing our common stock at what we believe to be very attractive prices. As such, we are pleased to announce that we are increasing our planned capital allocation percentage for shareholder returns to approximately 75% of quarterly free cash flows with the intention of pivoting the program toward share repurchases and away from dividends moving forward.

So to begin, by basically any measure used to calculate cheapness, CONSOL does appear cheap.

A simple look at the PE reveals a ratio of 2.88 which is consistent with the trend across the coal sector. Calculating a free cashflow yield using the FCF from the trailing four quarters gives a yield of 31%, while annualizing the most recent quarter’s FCF of $220 million gives a yield of 45%. In it’s latest investor presentation, CONSOL displayed a chart showing that the company ranked in the top 98th percentile among the Russell 2000 in terms of FCF yield.

With all this cashflow, the company has been deploying cash left and right. The chart below shows the trends in how cash has been allocated since 2018. Debt reduction has been the obvious priority. In fact, from the beginning of 2018 to present, total indebtedness was reduced from about $900 million to $200 million. As the chart shows, most of that reduction came during 2022 when the company was benefiting from record high coal prices.

The chart also shows for two years, starting in the second half of 2020, the company allocated cash solely to debt reduction. Then in Q3 of 2022 the company began paying a dividend and a quarter later began buying back stock. According to the company, buybacks are going to be the priority going forward.

In the above quote, the CEO stated that management and the board believe the company is undervalued and that the best way to allocate capital is through buybacks instead of dividends. We agree with this assessment. With this reasoning in mind, CONSOL recently increased the target percentage of free cashflow to return to shareholders from 30-50% to a whopping 75% and increased the authorized repurchase program from $600 million to $1 billion. As of the beginning of May, approximately $705 million of the $1 billion remained for repurchases. Given that executive long-term incentive compensation is tied to free cashflow generation per share, we fully expect the company to meet its targets regarding buybacks.

So here’s a quick back-of-the-napkin calculation for the potential returns on the basis of the company allocating 75% of its FCF to buybacks.

The calculation

To consider a range of outcomes, let’s project that over the next four quarters CONSOL’s free cashflow is somewhere between what it was over the trailing twelve months and what this last quarter would be annualized. So that gives us a range of $603 to $880 million. If CONSOL allocates fully 75% of this FCF to buybacks that means they would allocate between $450 and $660 million. As such, all else remaining constant (which is admittedly an egregious simplification), they could buyback somewhere between 23% and 34% of the company’s market cap over the next year. This in turn, again all else remaining constant, could lead to a return of 30% to 51%.

So as we can see, CONSOL is set up to potentially literally force a solid return simply by allocating its strong FCF to share buybacks.

While there are definitely times when buying back shares is not a good use of capital, this situation highlights the powerful return generator it can be if used wisely. If you’re interested in more reading on buybacks, we highly recommend you check out the piece by

titled Cannibal Stocks. In the piece, he shares a table that he took from one of Mohnish Pabrai’s presentations showing the estimated returns given a certain percentage of shares bought back. It’s quiet eye-opening so we shared it below.

A top objection to this thesis is likely the argument that coal companies are benefiting from temporarily high prices caused by supply chain issues and that the overarching trend is a decline for entire the sector as coal is cast aside due to its negative effect on the environment.

Firstly, we’d reply by pointing out that CONSOL’s high revenues and cashflows are not entirely due to coal price increases. Volumes have also played a role as exemplified by CONSOL setting a record high throughput of 4.6 million tons at its Baltimore Marine Terminal.

Secondly, we believe that while coal use in the United States and Europe, well, Europe minus Germany, will likely to continue to decline, the rest of the world is unlikely to follow suit. We addressed this topic in Episode 64, where we discussed another coal-related company. We wrote:

[W]hile many in the world would love to breakup with coal once and for all, in 2022 the globe set a new record for coal consumption. And these levels are expected to remain elevated for years as growing demand in emerging economies make up for cutbacks in advanced economies. One has only to look at recent increases in coal sourced power production in India and Germany to sense just how badly the world still needs coal to sustain itself. While coal may not be chemically addictive, the increase in standard of living its cheap energy provides certainly is.

(For a comprehensive write-up on this topic, check out this article written by

.)So whether good or bad, we believe the world, particularly outside of the United States, will require more coal for much longer than the consensus of Western investors believe. Additionally, there’s also an argument to be made in support of higher demand in metallurgical coal which is used for industrial uses, over thermal coal used to produce electricity in power plants.

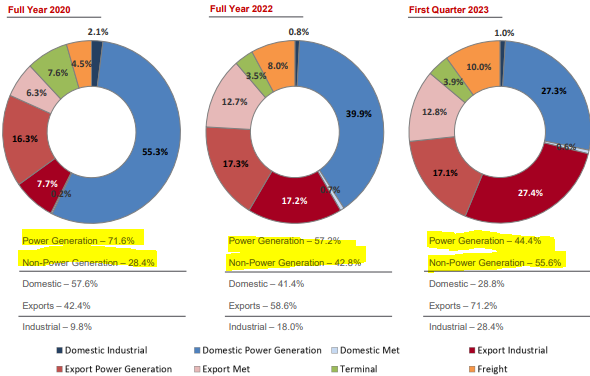

As such, we were encouraged to see CONSOL shifting both toward exports over domestic markets and toward non-power generation over power generation customers. This trend is show in the chart below.

So we’ll wrap up this episode, by reminding everyone that this isn’t a recommendation to buy CONSOL; it can’t even be considered a deep-dive. But for full disclosure, at the time of this writing, one of the show’s hosts has a very small long position in CONSOL Energy.

It’s also worth mentioning that while we like the setup in the coal sector and the tailwinds behind CONSOL particularly, we prefer building high-conviction long positions in asset-light companies due to our view that they will perform better in higher inflationary times. For such a company that both hosts are long, check out Episode 64 and Episode 68. If you’re interested in more coal company investing content we highly recommend you subscribe to

substack.Also, one note before we conclude. An astute reader commented on our last episode and caught an error we had made in our thought process. So please check out the comments from Episode 79 to get those details.

With that we’ve wrapped up another episode of Special Situation Investing. As always, thanks for listening and reading, and for giving us your support each and every week. See you all on the next episode.

This week’s top interviews

Share this post