Welcome to Episode 88 of Special Situation Investing.

My cohost and I talk about a lot about hard asset companies. Companies such as PrairieSky Royalty, Texas Pacific Land, High Arctic Energy Services, Mesabi Trust, PHX Minerals and National Resource Partners frequent the spotlight in our previous pieces. We want to begin today by explaining the rationale for this focus before discussing yet another hard asset company.

We’ll kick off the discussion with a quote by Seth Klarman from a recent episode of the Capital Allocator’s podcast. Explaining why Ben Graham’s book, The Intelligent Investor, is still relevant nearly a century after it was first published, Klarman said:

What’s still applicable is, that despite all the changes, the general principles, which are essentially dependent on humans and their psychological tendencies to get overly exuberant and overly depressed and to have constraints on humans, you must buy a highly rated bond, you can only own a stock that pays a dividend, you can’t own a stock below a certain market cap, or below a certain share price, and those kinds of rules and constraints can lead to inefficiencies. So while the nature of the exact inefficiencies may have changed a lot in eighty-nine years, the certainty that there will be those [inefficiencies] remains high.

Unless your investing style is limited to buying the S&P 500 or some other index, you, like Klarman, are likely looking to exploit inefficiencies in the market to realize market-beating returns. That’s certainly our goal.

Later in the same interview, Klarman stated he and his company search miles wide to find inefficiencies, and after one is found, they dig miles deep.

That’s also our general approach. We fight to keep an open mind and avoid limiting ourselves unnecessarily. We slowly expand our circle of competence by following rabbit holes of curiosity, all the while keeping our eyes peeled for valuable opportunities. This freedom is a small investor advantage of which we take full advantage.

The situation

Our mile-wide search led us to identifying hard asset companies as perhaps the area of greatest inefficiency in the current market.

As we’ve drilled deeper, the most glaring inefficiencies appear to occur in oil, gas, and coal companies. Even though these companies produce commodities still needed by the world, and are churning out record free cashflow, many asset managers in the US and other Western countries are prevented from buying these companies’ stock simply because it goes against the ruling ideology of the day. This is highly irrational and creates a situation where rational investors can profit.

For an example of a rational investor, consider Warren Buffett.

Over the last year, Buffett added to his position in Occidental Petroleum (OXY) with surprising consistency. What’s surprising is he wasn’t priced out by copycat institutional investors causing the price to rise out of his purchasing range. Today, the stock price is less than 10% higher than it was when he made his first purchases back in Q1 2022. Buffett now owns over 25% of OXY. For more detail on OXY, and what Buffett likely sees in the company, we recommend you read the piece recently written by Eagle Point Capital.

As you likely know, OXY isn’t Buffett’s only large investment in the energy sector. He also owns a stake in Chevron and added to his holdings as recently as Q3 2022. While the position was reduced slightly over the last two quarters, Chevron is still Buffett’s fifth largest position, totaling over $21 billion. Kingswell, another Substack we recommend, posted a stellar piece discussing possible reasons behind what he terms Buffett’s “bet on old energy.”

Buffett’s most recent “old energy” bet is particularly interesting and inspired today’s piece.

Earlier this month, Berkshire Hathaway announced its intention to purchase a 50% stake in the Cove Point LNG export terminal from Dominion Energy. If the transaction goes through, this will increase Berkshire’s existing 25% interest to 75%. Given Buffett’s affinity for what he calls “toll bridge businesses,” it makes perfect sense that he wants to own a controlling stake in one of the few “bridges” that connects the United States’ bourgeoning LNG export industry with the energy-hungry world.

The Cove Point LNG facility is one of seven LNG export terminals in the United States. It was originally built in 1972 for the purpose of importing LNG from Algeria. Years of disuse resulted after the Algerians demanded higher prices for their gas but were rebuffed. The facility got a second chance at life in the mid 1990s when a liquification unit was installed and the facility was transformed into a storage facility for domestic natural gas. In 2003, Dominion Energy bought the facility and in 2011 the company received authorization to enter into contracts to export LNG. Cove Point was renovated to allow both the export and import of LNG. The first international deliveries were executed in 2018.

In 2019, Dominion sold a 25% stake in the facility to Brookfield. A year later in 2020, Dominion sold another 25% this time to Berkshire Hathaway and Berkshire Energy’s subsidiary BHE GT&S became the facility’s operator. The sale announced this month, makes sense for both involved parties as it allows Dominion Energy to continue the process of divesting its non-state regulated, non-core, assets. This is a trend we’ve seen across energy service companies such as Exelon, MDU Resources, and Southwestern Energy as these companies sell or spin-off their unregulated segments. While for Berkshire, it gives it a controlling stake in a facility the company has intimate knowledge of from operating it for three years, at a time when natural gas prices are relatively low and the sector’s out of favor, and LNG global demand is projected to rise for decades.

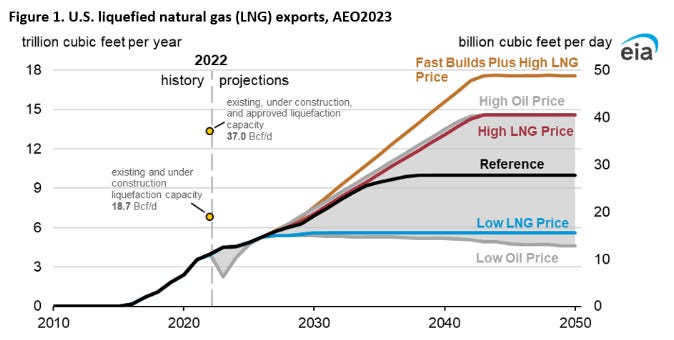

We noted in last week’s piece how the IEA and other such authorities in the energy space consistently underestimate the demand for fossil fuels. Year after year, predicted declines in demand for these commodities failed to materialize. It’s interesting that for LNG it’s a different story. As the chart above shows, in all but one hypothetical scenario, the IEA is actually predicting that US LNG exports will remain steady or increase through 2050.

If LNG is going to play an important role as a fuel of the future, and perhaps a growing role, it makes sense that Buffett would want to own one of only seven export terminals in the United States. There are currently more than a dozen export facilities in some stage of development, but for now, export terminals are a rare commodity.

According to the 2023 annual report of the International Group of Liquified Natural Gas Importers, here’s a list of the other six terminals and the companies that own them:

Sabine Pass LNG Export Terminal, Louisiana: Owned by Cheniere via its subsidiary Cheniere Energy Partners.

Corpus Christi LNG Export Terminal, Texas: Owned by Cheniere via Corpus Christi Liquefaction LLC.

Freeport LNG Export Terminal, Texas: Owned by Freeport LNG Liquefaction, LLC.

Calcasieu Pass LNG Export Terminal, Louisiana: Owned by Venture Global Calcasieu Pass.

Cameron LNG Export Terminal, Louisiana: Sempra 50.2%, TotalEnergies 16.6%, Mitsui 16.6%, Japan LNG Investment 16.6%.

Elba Island LNG Export Terminal, Georgia: Owned by Kinder Morgan.

So as we watched Buffett’s latest moves, we wondered: if one was so inclined to shadow Berkshire’s move into LNG, what are the possible avenues (i.e. companies) and which is the most direct play to the potential upside in LNG terminals?

Right off the bat, we excluded companies building new terminals and looked at companies that own operational terminals. This left us with the companies identified in the list above.

Narrowing the field further to companies that are publicly traded and can be easily owned by US investors, we produced the following list: Cheniere Energy, Cheniere Energy Partners, TotalEnergies, and Kinder Morgan. While Cheniere Energy came in a close second with its interests in both Sabine Pass LNG and Corpus Christi LNG, we believe the most direct and concentrated investment in LNG terminals is through Cheniere Energy Partners, traded on the NYSE under the ticker CQP. So our interest was peaked and we did a bit further digging.

Here’s what we found on our initial, and admittedly very shallow, dive into the company. Let’s not even call it a dive, but just an introduction.

The company

Cheniere Energy Partners LP is a limited partnership established by its parent company, Cheniere Energy, in 2006. The partnership was created to own the Sabine Pass LNG terminal near Cameron Parish, Louisiana, and is one of the largest LNG production facilities in the world. Sabine Pass was the first LNG export facility approved in the lower 48 United States and was again the first to export LNG, which it first did in 2016.

Today, it has six operational trains, with its sixth being completed in February of 2022. The term train simply refers to the liquefication unit that produces the LNG.

The facility is capable of a total operational production capacity of approximately 30 mtpa (million tones per year) of LNG. One mtpa equals 48.7 Bcf/year which means the terminal can process approximately 1.5 Tcf/year. It has operational regasification capacity of approximately 4 Bcf/d and aggregate LNG storage capacity of approximately 17 Bcfe.

The terminal has three total marine berths where transport ships dock to get filled. One berth can accommodate vessels with 200,000 cubic meters and the other two can accommodate vessels up to 266,000 cubic meters.

Like much of the rest of the energy transportation industry, CQP’s business model operates with long-term contracts creating a somewhat stable, predictable business. Most of their contracts require the customers to pay a fixed fee regardless of whether they elect to receive the LNG or not. In its 2022 annual report, CQP stated it has contracted approximately 85% of its production capacity with an average contract life of 15 years. The five customers that make up more than 10% of CQP’s revenue are shown in the table below.

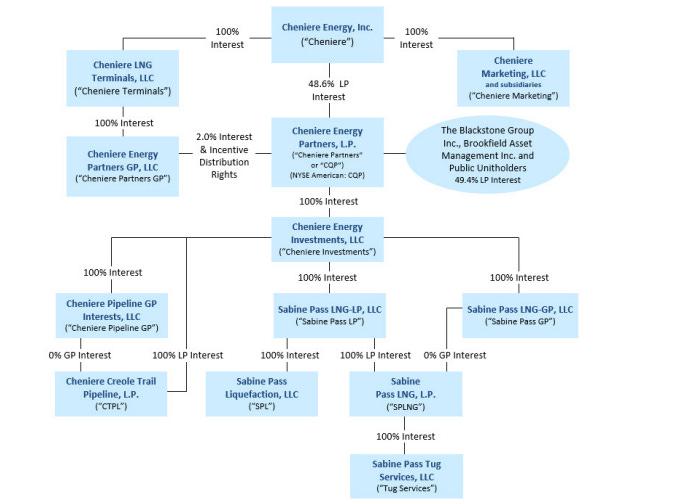

While CQP’s filings states it has zero direct employees, its subsidiaries employ a force of 517 who directly support the Sabine Pass LNG Terminal operations. As the diagram below shows, at its base layer, the actual work at the terminal is done by CQP’s subsidiaries Cheniere Creole Trail Pipeline, L.P.; Sabine Pass Liquification, LLC; Sabine Pass LNG, L.P.; and Sabine Pass Tug Services, LLC.

The same diagram indicates that roughly 2% of CQP is owned by Cheniere Energy Partners GP, 49% is owned by Cheniere Energy, and the last 49% is owned by public unit holders including a 21% stake by The Blackstone Group and a 20% stake by Brookfield Asset Management.

As an investment, Chenier Energy Partner’s history is checkered. On a time frame of 1995 to present, with dividends reinvested, CQP has outpaced the S&P500 with an annualize return of 14.6% to the index’s 9.35%. While without dividends reinvested, it essentially kept pace with the index.

Another aspect we look for in an investment is high insider ownership. In this case, CQP comes up seriously short. As of February of 2023, the directors and executive officers of the company owned only 49,649 common units which amounts to less than 1%.

Against a market cap of $25 billion and total assets of $18.8 billion, CQP has current liabilities of $1.3 billion and total long-term debt of $16.1 billion. Although these types of numbers are expected given the nature of the midstream and energy transportation business, they are not the type of number we are looking for in our investments.

With that we’ll warp up the discussion on Cheniere Energy Partners.

The wrap up

Ultimately, we’ll continue to watch CQP. If nothing else, it’s a useful gage for keeping tabs on the LNG sector. But it doesn’t meet our criteria for investing at this time.

We are looking for hard asset, asset-light businesses with little to no debt and that have invested management.

Many of the companies we mentioned at the start of this piece meet all of those criteria. And we hold positions in many of them.

One company in particular, also in the natural gas sector, that could prove a better alternative to CQP, is PHX Minerals. Feel free to check out our previous two write-ups on that company in the links below:

Because it may seem odd do write up on a company that ends without a recommendation, perhaps this is a good place to remind all readers and listeners that our goal with sharing our research is to, well, do just that…share our research. We hope that by putting our research out there for others to enjoy and critique, it proves useful to others as a jumping off point in their own research. We also believe writing is one of the best tools for refining your thoughts. We hope we will become better investors ourselves by adding skin-in-the-game and having others hold our feet to the fire.

With that, we hope you enjoyed this edition of Special Situation Investing. Thank you to all our new subscribers and to everyone who supported us with a like, comment, or a share. It’s honestly very encouraging. So thank you.

We’ll see you all on the next episode.

Share this post