Remember you can support the show in the following ways:

To sign up for Strike visit the following link : https://strike.me/en/

To get $10 for you and $10 for me at sign-up use referral code: ZEYDWP

Or contribute to the show directly by visiting: https://buzzsprout.com/1923146

Once on the shows website you can scan the QR code displayed and donate any amount of bitcoin to show your support

Listen to the Special Situation Investing Podcast on Fountain, on Apple Podcasts, on the website, or wherever you listen.

Welcome to Episode 50 of Special Situation Investing, where we bring you real-time investment research to help you better analyze your own investments.

Today we are taking a look at Worthington Industries (ticker WOR) and the recently announced spin-off of its steel processing business. The goal of today’s write-up is to layout the background of the parent company and specific details pertaining to the spin-off and its possible rationale.

Incorporated in June of 1955, Worthington Industries Inc (then called Worthington Steel Company) was founded by John H. McConnell to fill a niche in the steel market for custom steel processing. McConnell initially operated the company out of his home basement and actually took out a $600 loan against his car to finance his first deal. Profitability came quickly, in its first year in fact, and the company grew rapidly. In 1977 it began to diversify and renamed itself Worthington Industries. Much of its diversification since has been in the niche of creating cylinders, both out of steel and an array of other materials for a myriad of purposes, as we’ll see later.

One defining characteristics of the company’s founder, and one he instilled into the company’s written ethos, is treating customers by the Golden Rule. After more than a half a century, the company is still run much in the vane of its founder—people first. Upon John H. McConnell’s retirement from the business, his son, John P. McConnell, was CEO for many years and still currently serves as chairman of the board.

With that, let’s delve into the current makeup of Worthington. According to its annual report, Worthington is an:

“industrial manufacturing company, focused on value-added steel processing and manufactured consumer, building and sustainable mobility products.”

Worthington, with a $2.6 billion market cap, has four reportable segments. They are: steel processing, consumer products, building products and sustainable energy solutions. Here’s a brief encapsulation of each segment.

First, “steel processing” serves customers in a number of industries including automotive, aerospace, agricultural, appliance, construction, energy, hardware, heavy-truck, HVAC, lawn and garden, leisure and recreation, office furniture and equipment. Its largest customers by far are in the automotive industry.

Moving on to “consumer products,” this segment consists of products in the tools and outdoor living end markets. The products manufactured for these markets include propane-filled cylinders for torches, camping stoves and other applications, liquid petroleum gas cylinders, handheld torches, helium filled balloon kits, specialized hand tools and instruments, and drywall tools.

Next, “building products'“ sells refrigerant and LPG cylinders, well water and expansion tanks, and other specialty products, which are generally sold to gas producers and distributors.

And finally, “sustainable energy solutions” includes onboard fueling systems and services, as well as gas containment solutions and services for storage, transport and distribution of industrial gases.

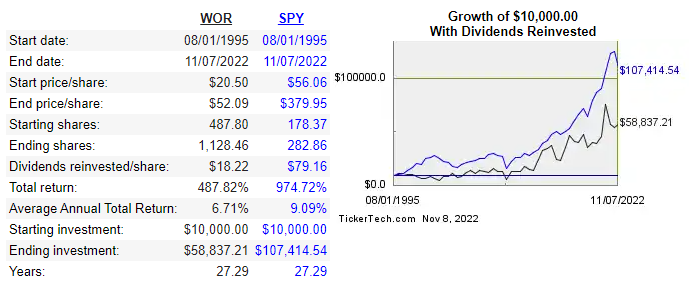

Worthington’s leadership states that (like most public companies) its top priority is producing strong returns for its shareholders. Well, how has it done? One quick measure of success, as we talked about in Episode 46, is high return on invested capital (ROIC). This metric tells how efficiently a company reinvests its capital. Worthington’s averaged ROIC record over the last five years is a modest 18.0%. While in line with its industry, that track record is well below many other companies we’ve discussed on this podcast (check out OTCM, TPL and ICE, as examples). The results can be seen in the graph below showing Worthington’s underperformance against the S&P since 1995. While the S&P averaged an annual return of 9.09%, Worthington averaged only 6.71%.

While Worthington itself may not compare well to other companies we like as a long-term compounders, or as we call them, “general investments,” perhaps it would make sense as a “workout” by playing the spin-off situation. So let’s consider the information that is currently available on the spin-off.

On September 29th, Worthington announced its intention to separate its steel processing segment into its own publicly listed company — currently being called Worthington Steel. The remaining company — currently being referred to as New Worthington — would be comprised of the three remaining segments: consumer products, building products and sustainable energy solutions.

Worthington Industries plans to complete the spin-off via a distribution of stock of the steel processing business. It is expected to be a tax-free distribution to shareholders for U.S. federal income tax purposes and the separation is expected to be completed by early 2024.

Similar to other spin-offs we’ve covered this year, Worthington’s rationale for the spin-off is likely the desire to jettison a segment of the company that is: 1) considered less environmentally friendly and thus less investable in today’s culture (similar to MDU’s spin-off of Knife River and Jefferies Financial’s spin-off of Vitesse Energy), and 2) a segment that has low margins compared to the rest of the company. This second reason is reminiscent of Fortune Brands’ rationale for the spin-off of its cabinets business. The end goal likely being the rerating higher of New Worthington’s valuation.

This hypothesis is supported by statements within the press release announcing the spin-off. It stated:

“The new company’s high margins and asset-light focus is expected to enable strong free cash flow generation and returns for shareholders. Further, New Worthington’s value will no longer be highly correlated to the price of steel, providing the opportunity for premium sector multiples.”

In contrast, when explaining the advantages of the spin-off, the press release explained:

“Worthington Steel will have a unique capability set and sophisticated supply chain and pricing solutions to serve its blue chip customers, grow market share and increase margins.”

The picture this paints is that Worthington Steel is a drag on New Worthington’s margins and valuations.

The numbers back this up.

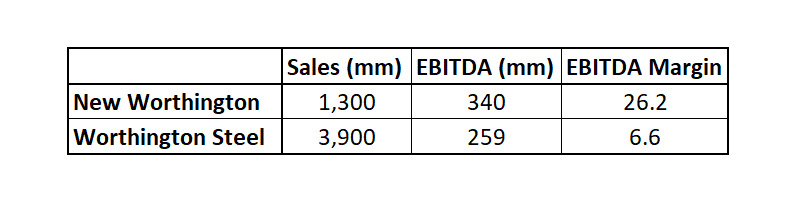

The same press release listed the total sales and EBITDA for each projected company. It reveals a stark contrast in EBITDA margin—26.2% for New Worthington and 6.6% for Worthington Steel.

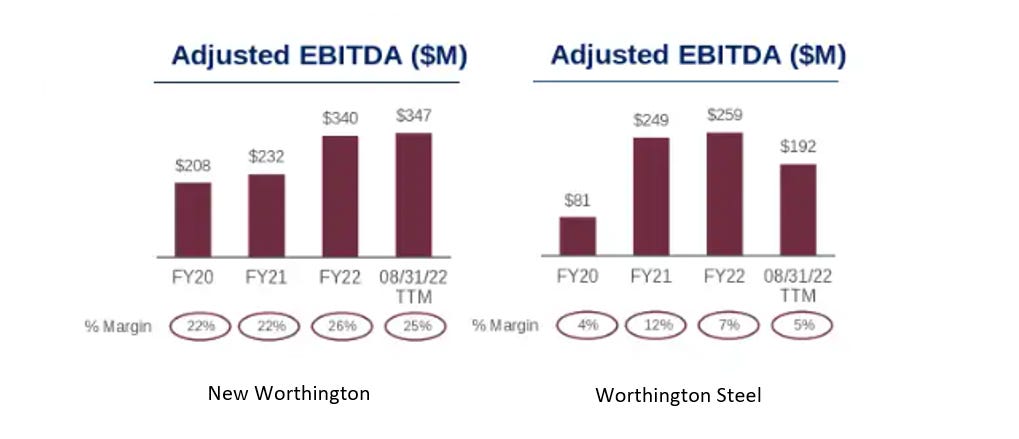

Current day Worthington’s EBITDA margins are a rough average of the two future companies. Data on Morningstar shows the current EBITDA margin is 10.0% and its five year average of 14.8%, with three out of the five years producing margins less than 10%.

In Worthington’s latest investor presentation this contrast is prominently displayed with graphs depicting the EBITDA margins of the two projected companies over the last for years.

So this leads us to ask: if the two companies were separated, would value be created?

One way to answer this question is to use data from comparison companies and calculate a potential market cap for the future companies. That way we can compare those estimates against Worthington Industrial’s market cap today.

In running this exercise, the comparison companies for the future Worthington Steel—the spin-off— we used are TimkenSteel Corporation and Reliance Steel & Aluminum Company.

TimkenSteel Corporation has a price/sales ratio of 0.71 and Reliance Steel’s is 0.74. Using the average of the price/sales ratios of these two comparison companies and the sales data provide in the table above, we can estimate Worthington Steel’s market cap could be in the ballpark of $2.8 billion. That’s half of the answer.

Moving on to comparison companies for New Worthington. Companies that operate within the same niche were harder to find, but we did the next best thing and used two companies that are similar industrial conglomerates—Gibraltar Industries and Valmont Industries.

Gibraltar Industries designs products for the agtech, renewable energy, infrastructure and residential sectors and has a price/sales of 1.19. Valmont Industries provides services and products for infrastructure development, irrigation and agriculture and has a price/sales of 1.67. So the first insight that appears is that industrial conglomerates tend to have better ratios compared to steel processors. The average of those two price/sale ratios is 1.43. Using that ratio with New Worthington’s 1.3 billion projected sales, give a estimated market cap of $1.9 billion.

Adding the two estimated market caps for the future companies gives a rough $4.7 billion. This is compared to Worthington’s market cap to day of $2.8 billion. Clearly these are rough calculations, but the magnitude of the difference does suggest that the spin-off could allow at least one, if not both companies, to be rerated higher once they are sperate and more focused companies.

And with that, we’ve concluded another episode of Special Situation Investing. We hope that, as always, you’ve found this write-up educational and helpful in your own investment journey. Remember, you can find all the transcripts to these episodes, as well as some Substack-only material, at specialsituationinvesting.substack.com.

SUBSTACK-ONLY BONUS

Nick Sleep is one of the most private mega investors out there. With his fund, Nomad Investment Partnership, he achieved a stunning total return of 921% versus 117% for the world index during the fund’s tenure from 2001 to 2014. With no interviews out there, one of the best ways to learn from Sleep is to read his annual partnership letters. They are a wealth of investment wisdom. Access the letter HERE.

Luke Gromen’s interview on RealVision is an interesting listen:

Share this post