Welcome to Episode 114 of Special Situation Investing.

Sometimes research leads to an exciting opportunity…and then there’s the majority of the time. As we know, the preponderance of an investor’s time is spent saying no to opportunities that aren’t fat pitches or an obvious yes.

When we started Special Situation Investing, my cohost and I debated whether to only share ideas we were excited about or to share everything we research regardless of our eventual opinion of the investment merits. We decided to share the entire spectrum of research—our favorite ideas as well as situations and/or companies we research but ultimately don’t meet our standards.

Our take is incapsulated in how Anthony Deden responded when asked if hours spent learning about a company, sector, or market is ever wasted. He said:

No, it's not wasted at all. What happens is that you…spend three, four, or five days understanding how oil is extracted in, say, Canada, and how it's refined, and how it goes here and there, and the cost components and the capital structures of companies…you acquire something. You may do nothing about it. But it's filed [in your brain]. So next time the situation comes, you have tools with which to think.

Today’s topic is not a fat pitch but we still learned from researching it and we hope you pick up a tool or two as well.

The Company

With uranium in a hot bull market, finding overlooked value in a uranium stock is unlikely. Still, we couldn’t help sniffing around the sector. Because of our affinity for the royalty-base business model, Uranium Royalty Corp was were we spent most of our time.

Based in Canada and established on April 21, 2017, Uranium Royalty Corp is the only pure uranium royalty company in the market. In this piece, I’ll refer to the company as URC and all amounts are in Canadian dollars unless otherwise noted. The company is listed on the Toronto Stock Exchange (URC) last year and on the NASDAQ (UROY) in the United States.

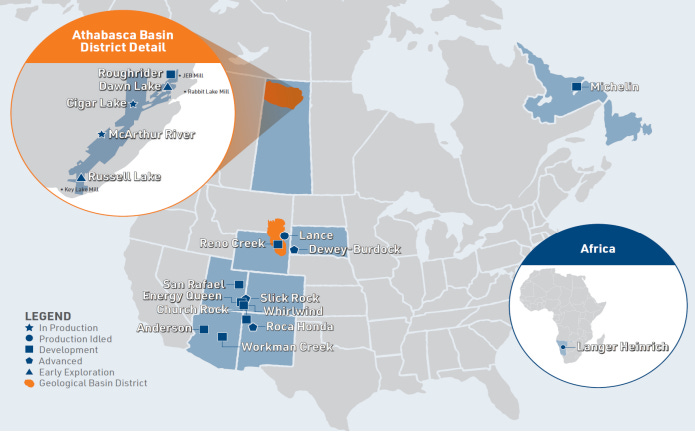

Its business model has three legs: 1) building a portfolio of purely uranium royalties, 2) investing in uranium-based companies and 3) trading physical uranium. The long-term strategy is to focus on the first leg with the other two legs supporting as opportunities present themselves. As of December 2023, URC owned twenty royalty interests on eighteen uranium projects ranging from the developmental to the producing stage. Other than one royalty in Africa, all of URC’s royalty interests are located in either the United States or Canada.

Out of the eighteen royalty interests, only two are on projects currently in production. Both of these mines are in the Athabasca Basin in Saskatchewan, Canada. The first, McArthur River mine, is a joint venture between Cameco and Orano, and URC owns a 1% GORR on 9% of the production. The other project in production is Cigar Lake/Waterbury. It’s a joint venture between Cameco, Orano, and TEPCO Resources Inc, and URC owns a 20% NPI royalty on a 3.75% share.

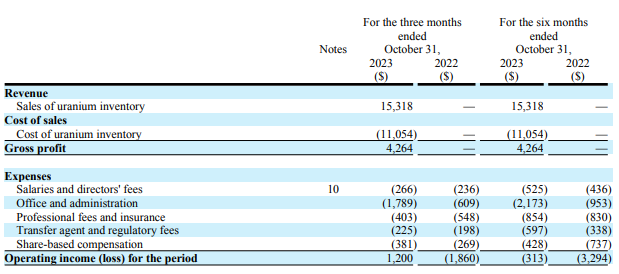

Even with interests on two producing mines, URC’s latest filing records no revenue from royalty interests. The only line item under Revenue is “Sales of uranium inventory,” as shown below.

But this doesn’t tell the whole story because URC receives its royalty payments from the McArthur River mine via physical uranium. According to its most recent report:

The Company recorded a depletion of $86 and $231 on the McArthur River royalty and an increase in inventory by the same amount during the three and six months ended October 31, 2023, respectively. On August 31, 2023, Orano settled the royalty payments related to the production from the McArthur River mine for calendar year 2022 by delivering 1,038 pounds U3O8 to the Company's storage account at Blind River in Canada.

So, the royalty payments from the McArthur mine, although small, do exist, but show up under inventory not revenue.

The Cigar Lake/Waterbury mine, on the other hand, has not contributed any royalties to URC. This is due to the nature the royalty being a Net Profit Interest (NPI). As opposed to a Gross Overriding Royalty like it has with McArthur where it receives a percentage of the revenue, with a Net Profit Interest, URC receives a percentage of the revenue only after its been reduced by certain cost and expenses. Since Cigar Lake/Waterbury is investing in mine development, its capex is currently zeroing out net profits.

The second leg of URC’s business is partial ownership of other uranium-based companies through common share ownership. In its latest quarterly report, URC owned ordinary shares of Yellow Cake and Queens Road Capital Ltd. Filed under the category of “short term investments,” they seem to be short term indeed and, in fact, are almost entirely gone. The report states:

As at October 31, 2023, the fair value of the Company's investment in Yellow Cake plc ("Yellow Cake") and Queen's Road Capital Investment Ltd. ("QRC") is $11,096 and $6,535, respectively….During the six months ended October 31, 2023, the Company sold a portion of its shares in Yellow Cake for proceeds of $34,020, of which $30,070 had been received by the Company as at October 31, 2023. The Company realized a gain of $15,341 which had already been included in accumulated other comprehensive income…Subsequent to October 31, 2023, the Company disposed all of the remaining Yellow Cake ordinary shares for gross proceeds of approximately $11.4 million.

If URC hasn’t bought or sold any securities since this filing, it appears this leg of the business amounts to a mere six or seven thousand dollar investment in Queen’s Road Capital Investment.

The Interesting Part

With little revenue from royalties, and having sold almost all of its shares of other uranium companies, the most consequential part of URC’s business (currently) is its ownership of physical uranium—referred to as “trading physical uranium” in the company’s reports.

A press release from October 2023 reveals how actively URC buys and sells physical uranium and how lucrative it can prove in a bull market. The press release states:

[URC] is pleased to announce that it has secured additional fixed-price uranium purchase commitments totaling 1 million pounds U3O8 in the current quarter. Deliveries will occur at Cameco Corporation’s Blind River facility in Ontario, Canada during the fourth quarter of 2023. The weighted average purchase price for such commitments is US$70.44 per pound…which is expected to be satisfied through cash on hand and other liquid assets.

The Company is also pleased to announce it has received the first delivery of 300,000 pounds U3O8 under its purchase agreement with CGN Global Uranium Ltd. dated November 17, 2021. This agreement provides URC with exposure to an aggregate 500,000 pounds U3O8 from 2023 through 2025 at a weighted average price of US$47.71 per pound. The delivery of the remaining 200,000 pounds is expected to be completed in June 2024 and April 2025.

These purchases will increase URC’s physical uranium inventory to approximately 2.65 million pounds U3O8 at weighted average cost of approximately US$54.08 per pound.

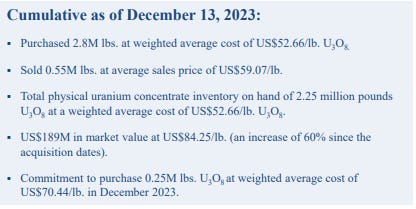

Since URC purchases and sells physical uranium so often, it’s hard to pin down the exact current state of its inventories. The most recent information available online is from its investor presentation and is current as of December 13, 2023. These details are shown in the image below.

The latest information suggests URC has a physical uranium inventory of 2.5 million lbs purchased for an average price of US$54.44. Add in the commitment to purchase 200,000 lbs by April 2025, and in a year’s time URC could own 2.7 million lbs purchased at an average price of US$53.94.

If inventories are 2.5 million lbs, at today’s spot price of US$100 per lbs, its inventories are worth US$250 million. This is 66% of the company’s US$381 million market cap.

That said, paying US$131 million (the company’s market cap minus its current inventories) for a company currently producing very little revenue, seems expensive.

Where this gets interesting is if the price of uranium continues to climb. At an uranium spot price of US$152, URC’s current inventory will appreciate to 100% of its current market cap. One would essentially have the portfolio of royalties and any ownership in other companies for free. A lot of ifs, but an interesting thought experiment.

To facilitate more trading, URC has a strategic agreement with Yellow Cake with an “option to acquire at market between US$2.5 million and US$10 million of triuranium octoxide ("U3O8") per year between January 1, 2019 and January 1, 2028, up to a maximum aggregate amount of US$21.25 million worth of U3O8 as at October 31, 2023.”

Management has communicated that it plans to continue trading physical uranium with the goal of converting profits into more uranium royalty interests. Royalties, in turn, will become the core of the company’s revenue over the long term.

The big negative is that much of its inventory purchases to date have been funded with share issuances. For example, through an at-the-market program announced in August of 2023, the company raised $3.5 million by issuing 870,910 through the end of October 2023. Also, that same month, the Company completed a public offering of 10,205,000 shares for gross proceeds of $40.9 million. The chart below shows the company has increased its share count every year since 2020.

Conclusion

Uranium Royalty Corp is clearly still in early-stage growth mode as it waits for its royalties to materially contribute to its revenue and cashflows. Incorporating at the beginning of an uranium bull market and its success trading physical uranium speaks to the management’s sector prowess. But share dilution funding keeping the company afloat and the uncertainty of the timing of new royalties coming online are large negatives. Currently, the company is essentially an expensive spot uranium fund with future potential upside from its royalty business. For us, the company is far from an easy yes.

With that, we hope you got something out of this piece and are enjoying and learning from the content we continue to release each week. Thankyou for all your support via comments, emails, shares, and boosts on the Fountain app. We will see you all again next Saturday.

Share this post