Welcome to Special Situation Investing Episode 76.

It’ll come as no surprise that, like many of you, we closely follow the 13F filings of top investors. Seeing what some of the most respected names in the field own, have bought, and have sold, proves time and again an effective way to generate ideas for stocks and sectors to research deeper.

It was while scouring the Q1 2023 changes to David Einhorn’s holdings that our interest was peaked when we saw his high concentration in energy, specifically oil, gas and coal. Einhorn displayed a contrarian confidence bucking the woke trend and adding to his holdings of CONSOL Energy, Teck Resources, Southwestern Energy, Civitas Resources, and he made an initial investment into Gulfport Energy.

One of Einhorn’s positions stood out to us because it was simultaneously listed on magicformulainvesting.com. Created by Joel Greenblatt, and made free to the public, the site attempts to create a list of cheap, high quality stocks. While there’s no magic about it, we use the site to generate ideas and we particularly look for industry trends across the list of stocks.

Similar to Einhorn’s portfolio, this curated list contained a high concentration of coal, oil and gas stocks, including one common to both — Southwestern Energy.

Without diving deep into the specifics on Southwestern (which may be the topic for a follow-up piece in the near future), let’s keep it high-level and consider a potential macro reason why we believe Southwestern came to be in Einhorn’s portfolio in the first place.

While our interest was peaked when we saw Southwestern pop up in both Einhorn’s portfolio and the magic formula, we didn’t begin putting the pieces of this thesis together until we listened to a recent interview with Einhorn on The Long and Short of Investing podcast. In the episode, Einhorn explained a recent shift in his investing thought process that gives insight into why his portfolio is stacked with energy names. He explained it in the following way:

The problem now is if you buy that thing…if it started at 11x earnings, in two years it’s very likely, instead of being at 15x earnings…it's going to be at 7x earnings. We're basically at the same price with earnings up 40% over a couple of years. You're not really going to make any money because there's nobody who is appreciating what is going on and analyzing it. It just gets lumped into a bucket.

So we need to have that story combined with, well, instead of paying 11x earnings, we're going to pay 4x earnings. And we're going to pay 4x earnings, and there's going to be a 20% buyback going on…and we can do that because there's really nobody paying attention.

There actually are companies that are that cheap in unpopular areas that don't even necessarily have bad businesses. And I think we're going to earn our returns off of buying things at much, much lower values and holding them until the capital has been fully returned.

What Einhorn seems to be saying is while he used to focus on finding cheap companies and buying them before the market noticed them, that strategy doesn’t work anymore. Today, solid, cheap companies can remain cheap, or get cheaper, for no other reason than, as Einhorn says, there’s no one paying attention to the companies’ quality and they simply get lumped into a bucket. If we had to guess, we’d say that two of the most common buckets into which such discarded investments are thrown could be labeled “non-ESG” and “non-index.” Einhorn goes on to explain that his new strategy is buying companies that can give him a high return on capital all on their own through dividends and share buybacks.

Coal producers are a clear example of this strategy. CONSOL Energy, a coal producer that makes up eight percent of Einhorn’s portfolio, currently trades at 4.5 times earnings and has a 7.5% dividend. Teck Resources, while bid up 40% from its recent lows on takeover hype, still only trades at a PE of 8. And while not in Einhorn’s portfolio, Peabody Energy is a perfect example of how this strategy could play out as it trades at PE of 2 and recently announced a new share repurchase program of up to $1 billion in common stock on a $3.5 billion market cap.

But in addition to buying uber cheap and banking on returns though buybacks and dividends, there appears to be a second prong to Einhorn’s strategy. He alludes to it in the same interview, saying:

Look, there's an off chance that I'm wrong and that other people will figure it out. There's also what happened to a couple of our companies last year, which is private equity comes in and pays a big premium.

So for stocks that can’t appreciate because of intentional neglect, another method of obtaining returns is through being bought out at a premium. Einhorn mentions private equity, which makes sense because such entities are less driven and shackled by public sentiment, but what he left out, and what we think is even more likely, is massive M&A coming from the oil majors.

Another podcast, this time it was Erik Townsend’s interview with Larry McDonald on MacroVoices, helped us understand why the majors may be on the verge of a massive M&A buying spree, and also why specific companies like Southwestern Energy are particularly enticing targets. The reason, as McDonald argues it, is that the majors have dwindling reserves and are prevented from restocking them through E&P because of political and cultural pressures. At the same time, small to mid cap O&G producers are very cheap on a per reserves basis. Erik Townsend asks his guest the following question:

So do I understand correctly that what you're doing now as a strategy is buying up companies for which the market is paying a relatively small premium per unit of reserves. And the arbitrage is essentially get reserves on the cheap because you know those companies are going to be acquired.

McDonald replies:

Yes, exactly. Get the reserves on the cheap. David Einhorn, at Greenlight Capital, he's been very public. A number of hedge funds are looking at this kind of relationship between reserves and market cap.

Let's say, you’re Chesapeake, you’re Range Resources, you’re Southwestern Energy. [In terms of] reserves of the smaller companies versus their market caps, the company's have much better value than they've ever had before on the smaller side. Think of the majors versus the minors, right? So the amount of natural gas and oil that the smaller companies have in reserves relative to their market cap is much greater than previous cycles. And then you take on the fact that from the regulatory point of view, how difficult it is to explore and find new assets, new reserves.

If you're Chevron and Exxon, five years ago together, you had maybe 6 billion of cash, right? Now you've got 40 to 50 billion between Exxon and Chevron, you got a lot of cash. And you see all of these assets around the world, your Southwestern Energy, your Chesapeake, your Range Resources, your Pioneers, all these, Murphy Oil, all these companies have tremendous reserves relative to their equity market cap. And so what this is setting up is one of the most impressive, most historic regime changes where the oil majors that are generating tons of free cash flow, because of all the legal constraints…we're setting up for a massive consolidation in the energy space that is setting up an incredible opportunity for our listeners and our investors.

So McDonald claims that a number of investors, himself and David Einhorn included, are building positions in smaller oil and gas companies with the expectation that the majors will employ their record billions in free cashflow by buying up these smaller companies in order to bulk up their dwindling reserves.

We believe this is likely Einhorn’s strategy with his current position in Southwestern Energy.

The core of the thesis is based on just how difficult it is for the majors to participate in E&P in today’s anti-hydrocarbon political environment. But in order to remain a viable company, reserves will need to be replenished one way or another. And investments in E&P have been neglected for so long that even if the majors were free to invest in unlimited E&P today, there wouldn’t be enough time to avoid a massive reduction in production over the next few years. This will drive the majors toward M&A out of necessity.

This last point was recently expounded on by Murray Stahl during his company’s latest conference call where he highlighted the approaching deficit of reserves in both the metal mining sector and the O&G sector. He said:

In the world of gold, you could make the assertion that something in like two years from now the way mining executives describe it is as a hole in production. What does that really mean? That means that unless something is done, roughly two years from now, production is going to drop. Why is it going to drop? Because as an industry we really haven’t been investing in the way historically the industry has invested. So two years is not enough time to start projects and bring them to production levels. So that explains the merger and acquisition activity.

Oil is the same thing with one singular difference. That difference is, there’s a geopolitical dimension to oil that doesn’t really exist in the world of gold.

You can tell what the investment in oil is by just looking at the rig count, the global rig count and the United States rig count, we’ve got an issue in the world of oil. So there’s not enough time to make the investment that needs to be made if indeed they could even be made given the hostility to the energy industry. So the next logical thing to do is to engage in merger and acquisition activity. If the food industry historically became and oligopoly, and if the communications industry became an oligopoly, if the information technology industry became an oligopoly…why would people think the world of metals and mining wouldn’t be an oligopoly and why wouldn’t people think that the world of petroleum wouldn’t become an oligopoly especially since, going back a century, that’s exactly what it was.

So as you can tell, for us, this was one of those times where, through broad listening and reading of multiple sources, an idea or thesis took shape. Stated clearly, we believe there is a special situation on a sector level forming in the small to mid cap O&G companies.

Below is a bullet point summary of the thesis:

Small and mid cap O&G companies are cheap on a reserves to market cap basis.

Oil majors are flush with billions in cash and prevented from investing in E&P.

As reserves approach critical levels, majors will be forced to replenish them via M&A.

Consolidation through M&A is the natural course of industry sectors with historical precedent making it even more likely in the O&G sector.

So, if one wanted to act on this thesis, what is the best way?

For full disclosure, at the time of this writing, neither host of this show has acted on this thesis, but we’re researching one involved company - Southwestern Energy. Why Southwestern? While it’s encouraging the company showed up both on the magic formula and in Einhorn’s portfolio, those are just bonuses. The real reason we believe it may be the best way to play this thesis is because of all the comparison companies in the sector we looked at, Southwestern is the cheapest on a reserves to market cap basis.

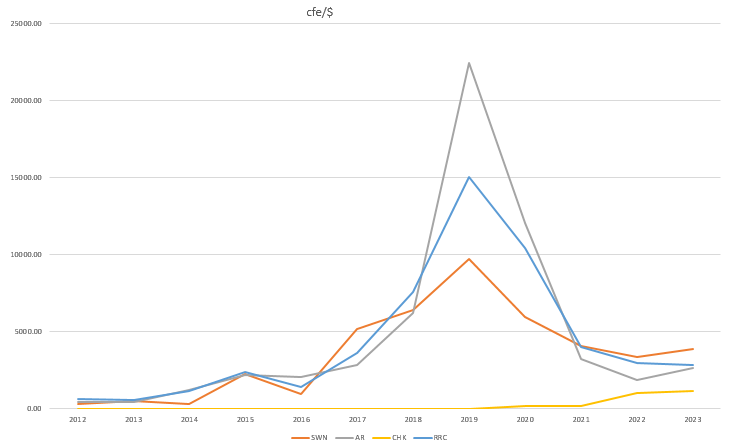

Take a look at the chart we created and included below. With help from Y Charts and the companies’ annual reports, we charted reserves divided by market cap for the past ten years of four companies in the sector. What it shows is how much reserves you get (measured in cubic feet equivalent) for each dollar in market cap. Basically, the higher the line, the more reserves you would get for each dollar spent.

A few points stand out from the chart: 1) these companies got extremely cheap by this measure from 2017 though 2021, 2) one can get more bang for their buck now than they could at any time besides the previously mentioned time period, 3) Southwestern Energy is currently the best value based on this one metric.

The catalyst for this thesis playing out will obviously be majors beginning to buyout these smaller companies. What may be less obvious is one won’t necessarily have to wait for a specific company they own to get bought out. Once the majors begin acquisitions, all similar companies will likely rerate to higher based off of the sale prices of the comparison companies.

As far as timing goes, well no one knows. But we do know the majors can’t wait long to fix the hole in production headed their way.

So with that we wrap up the latest episode of Special Situation Investing. We hope you are learning and growing from the content we put out. Thank you for showing your support for the time we invest into each of these episodes every week. We highly appreciate seeing all the new free Substack subscribers and also receiving bitcoin boosts from you guys using the Fountain app.

We’ll see you all next week on the next episode.

SUBSTACK-ONLY BONUS

Check out our favorite listens over the past week below. Enjoy!

Share this post