Remember you can support the show in the following ways:

To sign up for Strike visit the following link : https://strike.me/en/

To get $10 for you and $10 for me at sign-up use referral code: ZEYDWP

Or contribute to the show directly by visiting: https://buzzsprout.com/1923146

Once on the shows website you can scan the QR code displayed and donate any amount of bitcoin to show your support

Listen to the Special Situation Investing Podcast on Fountain, on Apple Podcasts, on the website, or wherever you listen.

Welcome to Episode 48 of Special Situation Investing, where we bring you real time investment research to help you better analyze your own stock picks.

On Friday we posted a Substack article that shared advice from Mohnish Pabrai who is one of the investors we admire most. Its rare for famous investors to share their investment research process, but that’s exactly what Pabrai did on a recent podcast. As you might expect, Pabrai doesn’t suggest beginning one’s research perusing the hottest stock picks on CNBC, MarketWatch, or even the Wall Street Journal. Surprisingly though, he does suggest a good starting point, the value investment idea site started by Joel Greenblatt - ValueInvestorsClub.com.

A search for the ticker symbol PHX on Value Investors Club reveals two write-ups, one written in 2006 and the other in 2015. While the ticker symbol remained constant, the company’s name changed from Panhandle Royalty at the time of the first writeup to Panhandle Oil & Gas at the time of the second. In 2020, the company changed its name for a third time with the latest change reflecting the company’s plan to reinvent itself once again. The company’s new name is PHX Minerals Inc.

We believe PHX Minerals presents an interesting opportunity for the following reasons: 1) it is transitioning to a lower cap ex business model, 2) the company’s leadership appears competent and transparent, and are large stock holders themselves, 3) the company appears undervalued compared to its peers, 4) the company’s natural gas focus aligns it well for continued future growth.

PHX had its genesis back in 1926 as a co-op for mineral rights ownership known as Panhandle Cooperative Royalty Company. Over fifty years later, after merging into Panhandle Royalty Company, PHX was listed publicly for the first time in 1979. After the merger, instead of paying out the majority of its earnings as dividends, the company began acquiring additional mineral acreage. In the early 2000’s, the company moved away from focusing solely on minerals and royalties and began participating in oil projects via non-operator working interests. This move away from being a pure royalty play pushed the company to rename itself Panhandle Oil and Gas in 2007.

Fast forwarding to September, 2019, the company board decided on a new (or more accurately, old) strategy and made a strategic shift back to being a pure play minerals and royalty company.

This shift is first mentioned by PHX in its 2019 Q2 call. The CEO at the time, Paul Blanchard, stated:

“As we look to maximize the value of our portfolio moving forward, we are strategically shifting away from working interest participation and moving back towards the original roots of the company as a pure play mineral and royalty company.”

By December of that year, Blanchard was replaced as CEO by Chad Stephens. At the time, Stephens had been a PHX board member for two years. He had retired from Range Resources in 2018 as its Senior VP of Corporate Development after thirty years of continuous employment at that company. Stephens was tasked with leading PHX through its strategic transition.

Over the following three years, the PHX team resolutely divested its considerable portfolio of non-operator working interests and employed the proceeds in purchases of new mineral and royalty interests. Their success has resulted in a dramatic shift in the proportion of revenue that PHX collects from royalties as compared to non-operator working interests. For example, revenues for the three months ending 31 December 2019 were split $4.6 million from working interests and $2.9 million from royalties. That’s in stark contrast to the three months ending 30 June 2022, where $7.1 million was from working interests and $12.5 million from royalties. Royalties grew from contributing only 39% of revenues to contributing 65%.

The increase in royalties, both in absolute and proportional terms, is depicted in the following chart.

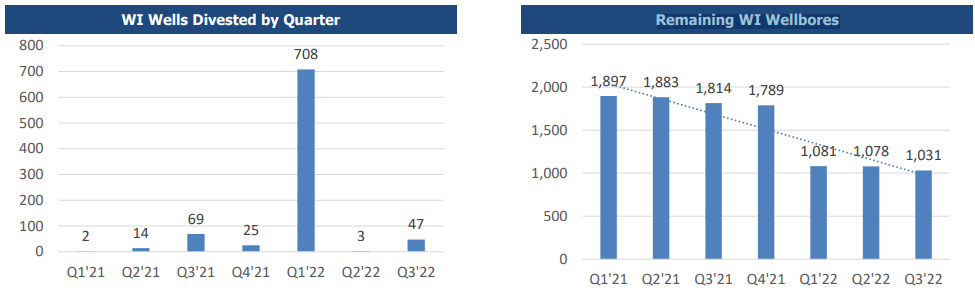

PHX leadership has reiterated over the past three years that this business transition would take time to do correctly. By this they’ve meant that they would be selling off their working interests as they find value-additive deals, and no sooner. Charts from the most recent investor’s presentation show the sales of working interests since Q1 2021. Starting at 1897, the number of working interest wells fell to 1031 by Q3 2022.

Additionally, the company recently announced divestitures of 210 more wells which they sold for $6.1 million in September. PHX simultaneously used those funds, plus a little debt, to purchase 575 net royalty acres for $6.2 million. Thus PHX’s current gross non-operator total is 789; a 58% decrease since Q1 2021. It appears the transition to a pure minerals and royalty company is well under way.

Part of our research on PHX consisted of reading every quarterly call transcript. Among other insights, these transcripts chronicled the leadership’s level-headed actions in reaction to the COVID crash and unusual commodity markets since. In Q2 2020, PHX’s dividend was cut from $0.04 to $0.01, headcount was reduced 20% and the company set a goal of reducing its debt/EBITDA ratio from 2.0 to approximately 1.0 and keeping it there. The company stuck to its plan and reached debt/EBITDA of 1.1 in Q4 2021. Since then the ratio has increased slightly to 1.3 (due to debt acquired to finance acquisitions) but arguably still meets the goal of approximately 1.0. This is another example of PHX’s leadership following through on their stated plans.

Another positive note on the PHX leadership is their ongoing share purchases. Looking back two years, the CEO, CFO, a handful of board members and a 10% share holder, Edenbrook Capital, have all consistently added to their shares of PHX as recently as September 27th. Big picture, this both highlights that company leadership’s interests are aligned with common shareholders, and it points to their conviction that the stock is undervalued.

In the most recent earnings call, D’Amico Raphael, PHX’s CFO, had this to say:

“We are happy with where the company is going. The stock price is a mystery to us. We don’t get it. But look, we see value there and [we] just almost every quarter, keep buying stock. So, I think that says a lot about how we feel about it.”

What Raphael probably means by the stock price being “a mystery” can be seen when charting PHX stock price against peer royalty stocks or the S&P 500. While the S&P enjoyed a record run, and many peer royalty companies increased 2x or more, PHX has barely doubled since its lows in October 2020. PHX’s multi-year underperformance is clearly shown in the chart below.

As we know, the price of a stock doesn’t necessarily reflect its value. Stock performance is often appropriate for one reason or another. Therefore it’s necessary to dig deeper and attempt to ascertain the stock’s approximate value, and compare that to the price, in order to see if PHX is a bargain.

One common method of valuing resource stocks, such as miners and oil producers, is the PV-10 method. PV stands for present value and 10 is the rate at which future earnings are discounted to the present day. PHX’s most recent investors presentation gave PV-10 values for their stock based on different commodity price ranges and a variety of estimates for their reserves. Their valuations, compiled in the chart below, show that even the most conservative estimate (SEC pricing and only proved reserves) would indicate a 32% upside is warranted.

One interesting note is that reserves categorized as “probable” share all the same characteristics as proved reserves except that the development timing is uncertain. Because PHX, and other royalty companies, don’t operate the wells within their portfolios, and don’t know their operator’s development timelines, they must categorize certain reserves as probable that might otherwise be considered proved. In fact, these probable reserves may even be listed as proved in the respective operator’s reports.

Considering this information, a more realistic PV-10 might be what’s listed as 2P PV-10 in the chart above. Using the SEC pricing, this calculation would indicate a possible 200% increase is warranted.

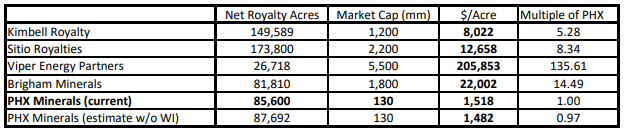

Another way to get a sense for if a stock is fairly priced is to compare it to its peer group. In the table below, a handful of oil and gas royalty companies are compared to PHX on a dollars-to-NRA (net royalty acre) basis. This is a “back of a napkin” type of calculation since many variables affect the value of royalty acreage. But by this simple metric, PHX does appear valued at the extreme bottom of its peer group. PHX is valued at $1518/NRA, while its closest peer in the group is valued 5 times higher, and the highest is valued 136 times higher.

At this point, its prudent to ask what might be the cause of such severe underperformance and such low valuation of PHX’s assets. Is PHX a value trap? Well, it could be. Honestly, we haven’t yet done enough research ourselves to answer that question with a high degree of certainty.

But our initial research leads us to believe that it’s PHX’s small size, and current business model transition that may be at the crux of its under-valuation.

First, as we’ve mentioned in previous podcasts, many large investors and funds cannot invest in small or micro cap companies. Small caps simply don’t have the necessary liquidity. As can be seen in the table above, PHX’s market cap trails its next smallest peer 130 million against 1.2 billion. PHX likely doesn’t even show up on most investors radar. But what is uninvestable for large investors for a mere technical reason could create an opportunity for smaller investors.

The second possible reason for PHX’s lack-luster price action we believe is its on-going business model transition. This is likely a heavy anchor on PHX’s stock price. Investors hate uncertainty and this strategic shift (from primarily working interests to primarily minerals and royalties interests) creates loads of uncertainty. Think about it, the company is selling over half of its assets and buying totally new assets of a different type. A lot could go wrong in such a massive transition. Not only that, but a new CEO was brought on to do the job…bringing more uncertainty.

In conclusion, even after accounting for the uncertainty, we like the setup with PHX. The company is tactfully transitioning out of the higher cap ex business model of non-operator working interests to the royalty business model that we favor in today’s inflationary environment. The PHX team’s results thus far indicate they are up to the task of pulling off this strategic shift. The on-going stock purchases by the company’s leadership is also an encouraging sign. Also, the company appears undervalued compared to its peers due to technical factors and the current business uncertainty. And lastly, PHX’s natural gas and oil gas focus positions it in a sector that we believe will surprise to the upside over the decade ahead (for more details on that, check out Episode 31 - Oil Ain’t Toast). For all these reasons we are putting PHX high on our watch list as we continue to research it further.

That concludes Episode 48 of Special Situation Investing. Remember, the transcripts for every podcast that include the charts, graphs and tables we reference can be found at specialsituationinvesting.substack.com. We appreciate your support and hope you find every episode educational.

SUBSTACK-ONLY BONUS

One of our favorite resources for in-depth oil and gas market commentary is Bison Interests.

Share this post