Remember you can support the show in the following ways:

Consider switching to Fountain for all of your podcast listening. Fountain sources its content from the podcast index and allows users to receive and stream bitcoin micro payments between fans and content creators. Get payed just to listen to your favorite show and use our affiliate link to download the app: https://fountain.fm/user7318803752755346?code=6a82e4d49e

To sign up for Strike visit the following link : https://strike.me/en/

To get $10 for you and $10 for me at sign-up use referral code: ZEYDWP

Or contribute to the show directly by visiting: https://buzzsprout.com/1923146

Once on the shows website you can scan the QR code displayed and donate any amount of bitcoin to show your support

Listen to the Special Situation Investing Podcast on Fountain, on Apple Podcasts, on the website, or wherever you listen.

Welcome to Episode 43 of Special Situation Investing.

It’s been almost six months since our last episode on Mesabi Trust (ticker: MSB). Back in February on Episode 13, we introduced the trust, its royalty business model, as well as its ongoing dispute with the operator that mines the trust’s lands. And then a month later, on Episode 17, we delved a bit deeper into Mesabi’s iron ore reserves and what we believe to be the trust’s intrinsic advantages.

As a quick reminder on the background of the company (and to quote our earlier episode):

Mesabi Trust is an iron ore royalty stream. The trust was created in 1961 to hold the interests of the Mesabi Iron Company in the Mesabi Iron Range, which includes the Peters Lease, Cloquet Lease and Mesabi Lease. The properties are clustered together in the Mesabi Range of Minnesota and linked to a port in Silver Bay Minnesota via a 47 mile rail line. The rail line, processing plants, and port are all owned and controlled by Northshore Mining, which is a fully owned subsidiary of Cleveland Cliffs Company.

As a hard asset, low capex investment, our view is that Mesabi Trust offers solid inflation protected cashflows and is set up to do so for decades into the future. For more details and background, please check out Episodes 13 and 17. We hold this view is in spite of the current idling of the mines by Cleveland Cliffs as it protests its agreement with Mesabi Trust. (For full disclosure, both producers of this podcast own securities of Mesabi Trust.)

Alright, with that intro behind us, let’s take a look at what has transpired for Mesabi Trust since our last update in March.

First off, in July, the Trust paid out a $0.84 quarterly dividend, which equals 12.5% annualized at the price when announced. The trust was able to distribute this dividend because of its large cash reserves at the time. This was in spite of Cleveland Cliffs’ idling the mines this spring. At the time the idling, Cleveland Cliffs stated that it would continue through at least the fall of 2022.

The consequence of the idling was revealed in recent filings. In Q2, Cleveland Cliffs credited Mesabi Trust with just under 200,000 (198,495) tons of iron ore shipped, as compared to approximately 1.4M (1,393,902) tons shipped during Q2 of 2021. That is an 86% decrease, year over year. This demonstrates that the mine’s idling is having a very large negative effect on Cleveland Cliff’s iron ore production. And since Mesabi Trust receives the vast majority of its revenue from the quantity of iron ore Cleveland Cliffs ships, we can expect Mesabi’s earnings and dividends to decrease.

And finally, on July 22, 2022, Cleveland Cliffs announced that it was extending the ongoing idling at least through April of 2023.

So with all of those updates, we should conclude that it is likely that Cleveland Cliffs iron ore shipments will be near zero through at least April of next year. This will greatly reduce Mesabi’s revenue…to put it nicely.

But, due to the the royalty agreement between the two companies, regardless of whether any production or shipment of iron ore pellets has occurred, Cleveland Cliffs is obligated to pay Mesabi Trust a minimum advance royalty. Each year, the amount of the minimum advance royalty is adjusted based on the CPI. For a little history, the minimum advance royalty was $964,659 for calendar year 2020. It was $976,765 for calendar year 2021 and is $1,034,237 for calendar year 2022. If Cliffs shipped zero tons of iron ore, Mesabi’s revenue would be somewhere in the $1M range. This is obviously a huge drop from the $43M average revenue over the past three years.

So where does this leave us in regard to the merits of Mesabi Trust as an investment? Is it a disaster? Or is any near-term downside in the stock an opportunity? With so much negative news and near-term downside it could be easy to get focused on the near term and resort to first level thinking.

In this case, we find some comments from the CEO of FRMO Corp, Murray Stahl, during the company’s recent annual meeting, insightful. Murray’s thought process that comes across in his comments is a lesson in and of itself.

Here’s Murray’s insightful response to a question regarding the company’s investment in Mesabi Trust and how one should think about the extension of the mines’ idling. He said:

Let’s just put it this way. I’m not so sure that’s such a bad thing… Matter of fact, I just had this conversation with someone just a few days ago, and they didn’t ask the exactly same question, but they asked almost the same question. They phrased it this way, ‘you want to have the cashflow to be maximized every quarter, you want this thing to be producing, so what happens if it’s producing less, maybe even producing nothing? So what does that do to the value?’ I’m not so sure it doesn’t increase the value. So why do I want my asset to be sold right now? Maybe it’s worth more to me if you leave it in the ground and mine it next year, or in two years, or even five years from now. …Why am I in such a rush to dig out every ounce of this commodity and put it on the market at today’s prices. Maybe the prices in the future will be a lot better.

Later in the conference call, Murray shares an anecdote that leads him to believe leaving the mines idle for a long period is not in the best interest of Cleveland Cliffs. Referring to Cliff’s mines on Mesabi land, he explains:

So it’s an open pit mine, and without getting into all the engineering about it, its a big hole in the ground. So if you were looking into this hole, what would you see? You would see along the periphery of the hole a big spiral. It’s like a road way. So if you stop mining, for more than a brief period of time, well what happens in Minnesota? The same thing that happens everywhere else, it rains, it snows, its windy, and the structural supports of the roadway will rapidly erode. And you will have to rebuild all that. And depending on how much damage that is, that could be a hundred or two hundred million dollar undertaking for the mine operator. So I don’t worry much about it because I think time is on our side.”

Like Murray, we also think time is on our side, and sooner rather than later Cleveland Cliffs will choose to restart mining Mesabi’s land or sell the mines to another third operator. With the first option much more likely than the second.

With that said, another risk weighing on Mesabi’s stock price is the risk of global recession. As iron ore is a commodity whose demand closely tracks economic activity, any major recession could be an increasingly heavy weight on the price of the security. One possible counter weight to the risk of recession is the domestic movement to source more commodities from within US boarders. In the current environment of strained international relations, Mesabi’s domestic supply of low-cost iron ore could become a key national resource in high demand.

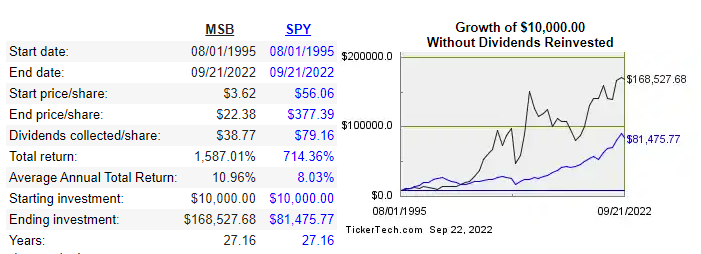

A look at Mesabi’s record vs the S&P500 shows that, while far more volatile, Mesabi far outperformed the S&P500 over the long term.

As can be seen from the chart above, a $10k investment in Mesabi, starting in 1995, would have outperformed the S&P500 up 16x vs the S&P500 up only 8x. With dividends reinvested, the outperformance is even more extreme.

Including reinvested dividends, Mesabi is up 77x vs the S&P500’s 10x. (To view these charts, please visit our Substack at specialsituationinvesting.substack.com or go to substack.com and enter Special Situation Investing in the search bar.)

So in conclusion, despite the current headwinds facing Mesabi Trust, we still maintain a positive, long-term outlook on this investment.

With that, we wrap up another episode of the Special Situation Investing show. We hope you found it informative and educational.

SUBSTACK ONLY BONUS

Murray Stahl is a brilliant investor and a fascinating mind. You can access one of our favorite interviews with Stahl here.

Share this post