Welcome to Episode 95 of Special Situation Investing

Today we’ll provide an overview of CME Group (CME), a U.S.-based derivatives exchange with a storied past and a stellar track record. The company passed easily through our investment filters and sits within the “generals” category as a business with fantastic characteristics that we’d love to own for the long-term. Exchanges, like brokers, royalties and consumer monopolies, are a category of businesses that offer high odds of success to investors seeking above-average returns As an exchange, CME sits at the heart of that thesis.

Advantages of the exchange business model

According to Investopedia, an exchange is defined as:

A marketplace where securities, commodities, derivatives and other financial instruments are traded. The core function of an exchange is to ensure fair and orderly trading and the efficient dissemination of price information for any securities trading on that exchange. Exchanges give companies, governments, and other groups a platform from which to sell securities to the investing public.

When discussing the advantages of exchanges over other business models, it’s important to remember exchanges are not market participants, but rather, are market makers. The distinction is subtle but important, considering that most of us don’t think in market-maker terms but rather as investors within a market.

Thinking from within the market leads investors to ponder questions related to market direction such as, whether the economy will grow or shrink, or what the future holds for a specific company. The market maker is different. The market maker is outside of the market and therefore agnostic as to its direction. Market makers profit when stocks rise and when stocks fall, because their revenue is derived from trading volume not market direction.

Furthermore, in most jurisdictions, exchanges operate as monopolies and oligopolies. While good old-fashion competition is great for economies, generally it’s terrible for individual businesses. The rare breed of businesses that can operate outside of capitalism’s creative destruction warrant special attention from investors.

Past examples of competition-free businesses include stellar performers like Google, Mastercard, and Visa, that, while they claim to compete with other companies, in the final analysis really do not. The benefits of avoiding competition in the world of business are so obvious that they don’t need to be restated here but it should be noted that few investors give enough weight to this factor when hunting for prospective investments.

A further benefit of the exchange business model is their capital-light structure. Here again, companies like Google, Mastercard, and Visa share a low-capex business structure, along with high returns on capital, with that of the exchanges. Relative to their market cap, exchanges have very few employees and can take on loads of new business, in the form of trading activity, using their existing suite of trading technologies. The ability to run orders of magnitude more business through the same computer infrastructure gives exchanges a huge operating margin advantage over standard capital-intensive and employee-intensive business models.

“Cross selling,” or the ability to sell the same thing in multiple ways, is another means by which the exchange business model enhances operating margins. Essentially, the exchange bundles and packages the trading data they already own and re-sells the information as investment research and market data. Put plainly, a single trade earns a commission but the very same transaction is then re-sold to the market as research and market data, thus increasing revenue without incurring additional costs.

Derivatives exchanges vs stock exchanges

Though all exchanges operate in a favored market niche benefiting from the aforementioned business characteristics, particular exchanges like CME Group possess even greater advantages that are unique to the trading platform they’ve created. CME Group’s previous CEO, Craig Donahue, explained this well in a 2009 Bloomberg interview when he said:

Futures markets are entirely different (from capital formation markets and securities) there about hedging risks, transferring risks, they tend to support more wholesale sophisticated financial institutions. We invent our products, there not just traded because the company did an IPO. The distinctions are really very significant, the markets are very different and we have to respect that.

One of the key takeaways from Mr. Donahue’s statement is that CME “invents” its products. Put plainly, an exchange like ICE, which owns the NYSE, monetizes the trades and data of public companies listed on their platform but if no companies chose to list themselves on the NYSE then the exchange would have no revenue. ICE, relies on third party listings in order to generate revenue. In CME’s case, however, third party listings are not required. By gauging customer demand for new products, CME is able to create products that never before existed and which can be marketed without third party participation.

CME Groups weather derivative products are an instructive example of the exchange’s ability to create new product offerings independent of third party participation:

Weather-related risk is broad in scope and spans across many industries and sectors. One sector that is particularly susceptible to temperature-based impacts on earnings and profitability is the electric utility sector. Utility firms expect to market a certain quantity of energy for a given season based on historical results and forecast data. Still, the quantity of energy they ultimately sell over a summer or winter season can vary significantly from expectations. This risk is referred to as “volumetric risk:” risk based upon the quantity of energy that might be expected to be marketed throughout the course of a heating or cooling season. As such, firms like electric utilities can use CME Weather futures and options to guard against volumetric risks and smooth out revenue fluctuations that are tied to unanticipated weather conditions.

Essentially, CME identified a market need related to participants demand for a climate hedging product. Utility companies are one obvious customer for this type of product as they must plan their energy purchases well in advance of the summer cooling and winter heating cycles, all the while knowing that their assumptions could be wrong. A utility company that over-purchased energy might need to put that risk to the market where as one that under-purchased energy may need a call option to protect them from higher energy prices mid season.

Understanding the intricacies of weather derivates is not the point of this illustration. Rather, the illustration was intended to demonstrate how CME identified a market demand signal for weather derivatives, created a product, and profited from the market that it created all without increased capital expenditure or third party participation. CME created the product, users are able to manage climate related risk, and the product runs on existing technological rails at CME with very little added cost to the company.

CME’s track record

CME’s advantaged business model is proven by even a cursory review of its track record. The following timeline of achievements is taken directly from the CME website and was shortened so as to give readers a flavor of CME’s history without covering every detail.

1800s

1848 - CBOT creates the world’s first futures exchange, based in Chicago.

1851 - CBOT offers earliest “forward” contract ever recorded; forward contracts begin to gain popularity among merchants and processors.

1865 - CBOT formalizes grain trading with the development of standardized agreements called “futures” contracts, world’s first such agreements CBOT creates world’s first futures clearing operation when it begins requiring performance bonds, called “margin,” to be posted by buyers and sellers in its grain markets.

1898 - Chicago Butter and Egg Board, predecessor of Chicago Mercantile Exchange, opens in Chicago.

1900s

1919 - Chicago Butter and Egg Board becomes Chicago Mercantile Exchange CME Clearing House established.

1936 - CBOT launches soybean contract.

1961 - CME launches first futures contract on frozen, stored meats—frozen pork bellies.

1964 - CME launches first agricultural futures based on non-storable commodities—live cattle

1968 - CBOT begins trading its first non-grain-related commodity, futures on chickens.

1969 - CBOT begins trading its first non-agricultural product, with a silver futures contract.

1972 - CME launches first financial futures contracts, offering contracts on seven foreign currencies.

1975 - CBOT launches first interest rate futures, offering a contract on the Government National Mortgage Association.

1981- CME launches first cash-settled futures contract, Eurodollar futures.

1982 - CME launches first successful stock index futures contract, S&P 500 Index futures CBOT launches first options on futures contract for U.S. Treasury Bond futures.

1999 - CME launches first weather-based futures contracts.

2000s

2006 - CBOT and CME sign an agreement to merge into a single company pending regulatory and shareholder approval CBOT launches electronic agricultural futures trading Launch of NYMEX products on CME Globex CME and Reuters agree to form first centrally cleared global FX platform for OTC market—FXMarketSpace.

2007 - CME and CBOT officially merge to form CME Group Inc., the world’s leading derivatives marketplace.

2008 - CME Group acquires NYMEX, adding energy and metals to its wide array of product offerings.

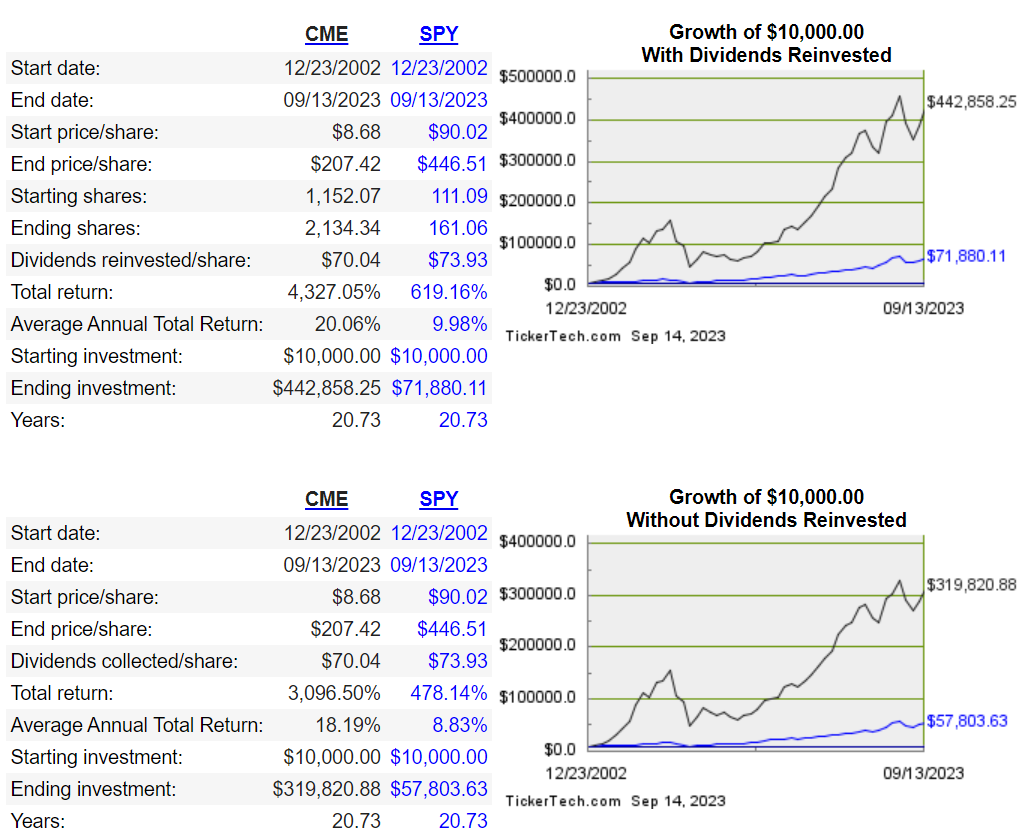

Further illustrating CME’s advantaged business model, the company’s stock price performance has been nothing short of mind blowing since it went public in 2002. With a $10k initial investment in CME returning $442,858 dollars compared to just $71,880 for the S&P 500 with dividends reinvested. This outperformance represents a 20.06% CAGR on CME’s part compared to just 9.98% for the index with dividends reinvested.

Global exchanges’ track record

Publicly traded US exchanges such as NYSE (ICE), and NASDAQ (NDAQ) have posted similar S&P 500 beating performances over the last two decades with CAGR’s in the high teens compared to around 9% for the S&P 500. Non-U.S. exchanges, however, have experienced more mixed results.

The Japan Exchange Group (JPXGY) underperformed the S&P 500 by nearly 10% per year from 2015 through today. London Stock Exchange Group (LNSTY) eked out a slight outperformance over the S&P 500 from the time of its listing in 2018 through today, but it was nowhere near the trouncing delivered by U.S.-based exchanges. Since its public listing in the U.S. in February of 2010, Deutsche Börse (DBOEY) lagged the S&P by just over a 2% CAGR which while respectable, again, doesn’t put its performance in the same league as the U.S. exchanges.

Verifying a performance disparity between U.S.-based exchanges and those domiciled in other countries is beyond the scope of this short article, as would be prognostications on why such disparities exist, but upon first inspection a difference does seem to be present. With that said, caveat emptor, to all of our readers and we encourage you to dig in and do your own analysis prior to making an investment decision.

If I were forced to speculate on the performance difference, however, I’d look into impacts of the Cantillon Effect on exchanges. It seems plausible that a trading volume based business, co-domiciled with the world’s reserve currency, could ride a money printing wave with commensurate increased trading volume that’s not available to foreign competitors. On the other hand, regulatory differences, or any number of other explanations, could also be the reason behind the performance differential. If indeed, the difference is tied to reserve currency status and co-location with the world’s largest capital markets then one has to wonder what effect the global de-dollarization trend will have on U.S.-based exchanges going forward.

Future market opportunities

Given CME Group’s past outperformance and current P/E ratio that puts it squarely in the category of “not cheap,” what are investors to make of its future prospects? It would seem that “the future” as Yogi Berra once put it “ain’t what it used to be.” In my opinion, however, this future of limited possibilities says more about our lack of creativity than it does about CME’s business prospects.

Consider for a moment what your own views on cryptocurrency and bitcoin were back in 2017. For a minority of our audience this exercise brings back warm memories of stacking bitcoin for $800 per coin and watching it 30x over the ensuing years. For others, we recall cheering for Charlie Munger as he touted the very same asset as “rat poison.”

This little exercise is not meant to pour salt in old wounds but rather to highlight that very few of us were creating futures based product around crypto currency in 2017 or could have imagined that market growing from nothing to over 175,000 contracts per day in 2022. CME did just that. The fact that CME Group was responding to customer demand and innovating in new markets and that they are able to innovate in a capital light manner is exactly why their future remains bright.

If the past is any guide to the future, CME’s next market opportunity sits in an area that none of has yet conceived of. It is the advantaged nature of their business model itself rather than external market conditions that will pave the road to continued success in the future.

Conclusion

In conclusion, we believe that exchanges, like royalties, brokers, and some consumer monopolies are areas of the market that offer investors a high probability of success. While it may seem that we hold countless unrelated companies in our portfolio the truth is really the opposite. Take all of our high-conviction ideas from the categories already mentioned and add them up and you have less than twenty stocks total. Pushing things a little bit might get you as high as 30 stocks, but even still, that would represent what most consider to be a concentrated portfolio. We still love special situation investing and invest in those “workouts” when we can, but we’re value agnostic and happen to be finding great value in asset-light businesses these days.

Much like Buffett and Munger, we believe in shooting fish in a barrel rather than casting a line into the ocean and especially like it when we can first drain the water from the barrel. Royalty companies, exchanges, brokers, and a few others represent a small part of the market with an outsized promise of free cash flow to investors and so we follow the money wherever it leads.

With that we hope you enjoyed another episode of the show. As always we appreciate your questions, support and your boosts on the Fountain podcasting app. We will see you again next week with another short but actionable investment write-up.

Share this post