Welcome to Episode 131 of Special Situation Investing.

My cohost and I have learned much about investing from Mohnish Pabrai. He is an ardent student of Warren Buffet and Charlie Munger and himself a successful value investor. He is also a vocal advocate of cloning.

In 2017, he tweeted: “Shameless cloning. The way to wealth! What could be simpler?”

In the context of investing—as opposed to biology—cloning is the act of making an investing decision because another investor did so. For example, maybe some investors recently cloned Berkshire Hathaway’s decision to buy Ulta Beauty.

The Good the Bad and the Ugly of 13Fs

One common way investors clone ideas is by tracking the buys and sells recorded in 13F filings. These quarterly filings are required by the SEC for institutional investment managers with at least $100 million in assets under management. Such filings provide a snapshot into these investors’ portfolio holdings. Here’s how Investopedia explains 13Fs:

Congress created the 13F requirement in 1975. Its intention was to provide the U.S. public with a view of the holdings of the nation's largest institutional investors. Lawmakers believed this would increase investor confidence in the integrity of the nation's financial markets.

Firms that are considered institutional investment managers include mutual funds, hedge funds, trust companies, pension funds, insurance companies, and registered investment advisors.

Because 13F filings provide investors with a look at the holdings of Wall Street's top stock pickers, many smaller investors have sought to use the filings as a guide for their own investment strategies. Their rationale is that the nation's largest institutional investors are not only presumably the smartest, but their size also gives them the power to move markets. So investing in the same stocks—or selling the same stocks—makes sense as a strategy.

While paying attention to what top investors are doing can be helpful, and perhaps lucrative, it can also be dangerous.

To be fair, that same Investopedia article goes on to list four key issues with 13F filings—unreliable data, time of reporting, herd behavior and an incomplete picture.

Unreliable Data

I don’t have any first-hand experience with this “issue” but it’s always a factor to keep in mind. This is particularly applicable when using aggregators such as dataroma.com. One can always read the 13Fs directly.

Time of Reporting

A commonly known caution about 13Fs is that managers are required to make their filings within forty-five days after the close of each quarter. This means that information contained in the filings could be as much as four months outdated. Many managers chose to report as late as possible and thus when the file drops their portfolio could technically be completely different. This is a caution to any investors who blindly clone.

Herd Behavior

This one is interesting. Given that the holdings of many top investors are made freely available, as you might expect, investors large and small have the tendency to copy. This can lead to a concentration in certain companies and, mostly small retail investors, are usually late to the party. For example, look at the image below from dataroma depicting the top ten most owned stocks among the superinvestors the site follows:

Google, Microsoft, Meta, Amazon, Visa, Berkshire Hathaway, Apple, United Health and Mastercard make up the list. The reasons these investors bought into these companies in mass may not be applicable today or they may have been the best companies with enough available float or they could have been bought for a reason that is totally different from any other investor. Blindly joining the herd can be dangerous.

An Incomplete Picture

This issue with 13Fs is related to the previous. In addition to only providing a snapshot-in-time picture of an investor’s holdings, these filings also might not be the entirety of their investments. Case in point is Mohnish Pabrai himself. While his current 13F only displays ownerships in a handful of coal producers, he has a large percentage of his portfolio outside the U.S., invested in Turkish companies. So, if one were to simply clone his U.S. holdings, they would in fact own a very different portfolio than the hero they are copying.

I was reminded of these four issues while perusing the latest quarterly 13F filings that dropped over the last couple weeks. Most of my perusing occurred on dataroma.com which is a site that aggregates the 13F filings of the top value-oriented investors in an easy-to-consume format. But even with all those cautions, such perusing is often worth the time because 13Fs still offer interesting insights and can be a productive place to hunt for new investing ideas—if used correctly.

A Worthy Example

Mohnish Pabrai offers a great example of how investors should approach using 13Fs.

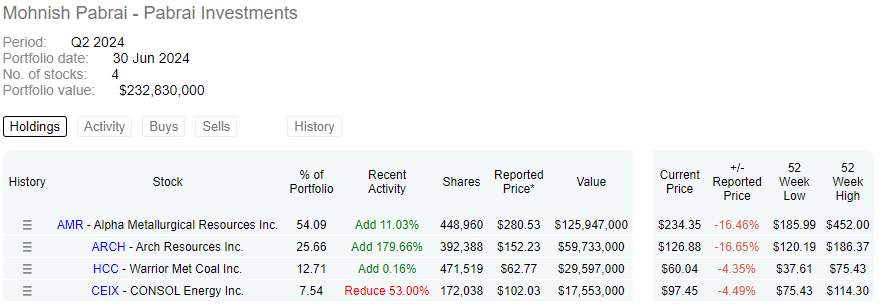

As previously mentioned, Pabrai’s current 13F filing contains only coal producer stocks—Alpha Metallurgical Resources, Arch Resources, Warrior Met Coal and CONSOL Energy.

On recent podcasts, Pabrai clearly enjoys telling the story of how he got interested in coal stocks. He says it began with a prompt from a Tweet which caused him to looked up the 13F of David Einhorn, CEO of Greenlight Capital. At that time, Einhorn’s second largest investment was in the coal producer CONSOL Energy. With his curiosity peaked, Pabrai dove headlong into researching CONSOL and the coal sector broadly, all in an effort to answer why Einhorn would put so much into a dirty coal company. What he discovered got him more interested and he went deeper, visiting multiple companies and even touring their mines. His research resulted in him selling all his other U.S. holdings and buying coal companies.

So even though Pabrai’s quote from the beginning of this piece says cloning is easy, the work Pabrai put into cloning Einhorn tells a different tale. Clearly, from the master cloner himself, an immense amount of work should backup any act of cloning.

With that cautionary tale behind us, here are a few insights I took away from the latest drop of 13Fs.

Filings of Interest

Berkshire Hathaway

Let’s start with the Oracle of Omaha. Two things. First, there was great excitement over “Buffett’s” purchase of Ulta Beauty. Given I’d always considered ULTA a quality company, its addition to Berkshire’s portfolio was not a shocker. I was not the least interested in looking at ULTA. Number one, because it’s outside my circle of competence and I have no desire at the moment to work to bring it in.

And, number two, I had the words of John Huber from Base Hit Investing in the back of my mind. In a recent article, John worked though an exercise where he estimates that, out of all the US stocks, Berkshire is limited to investing in thirty to forty. This is simply because of Berkshire’s size. So, just because Berkshire bought ULTA doesn’t mean it’s a great opportunity for investors with small amounts of capital to employ.

The second thing I found useful as a data point from Berkshire’s filing was that it continues to buy more Occidental Petroleum. I don’t personally own OXY, but I own two companies of which OXY is a customer, Texas Pacific Land and Natural Resource Partners. A strong OXY is good for both of those investments.

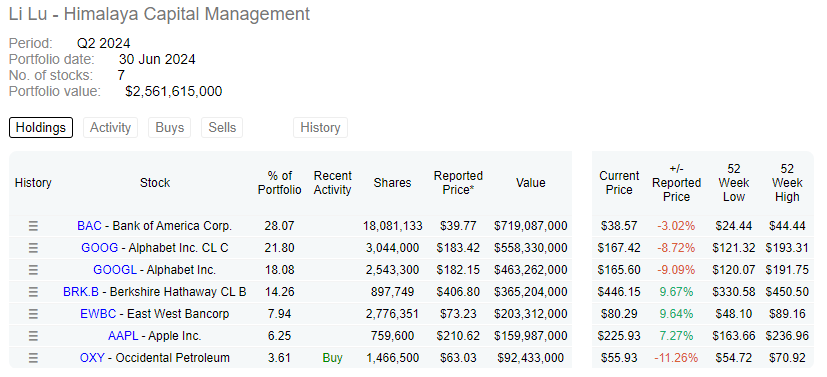

Himalaya Capital Management

Berkshire wasn’t the only purchaser of OXY. Li Lu of Himalaya Capital Management, a long-term oriented, value investor and friend of the late Charlie Munger also bought the company.

Li Lu manages a very low turnover portfolio, so this purchase was note worthy.

Aquamarine Capital

Mohnish Pabrai’s portfolio changes were highlighted early in the piece, so I won’t duplicate it here. Suffice it to say, it’s still only coal stocks and he bought more.

But he wasn’t the only buyer of coal stocks, Pabrai seemed to have rubbed off on Guy Spier of Aquamarine Capital who also initiated positions in Alpha Metallurgical Resources and Arch Resources. More attention on the coal space but still not anywhere concerning levels.

Scion Asset Management

Michael Burry and Scion Asset Management’s 13F was an example of a cautionary tale. In the previous quarter, Burry had bought Safe Bulkers, Vital Energy, Star Bulk Carriers, BP and Sprott Physical Gold Trust. These reflect an investment theme that I would generally espouse, specifically, hard assets. Had I blindly cloned Burry out of confirmation bias, I would have been dismayed when this latest 13 F filing revealed Burry sold 100% of these positions.

Oakcliff Capital

The filing by Bryan Lawrence and Oakcliff Capital particularly caught my attention because he sold 100% of Hallador Energy, a company I had highlighted in my recent piece, Rabbit Holes of Curiosity, and he instead bought Natural Resource Partners (NRP).

Over the past few months, I enjoyed listening and reading up on Lawrence and his investing style. His recent interview on the Wiser Richer Happier Podcast is the best and where I’d suggest anyone interested start.

Lawrence’s purchase of NRP is encouraging because he runs a concentrated, low turnover portfolio and he invests largely with the mindset to hold for years or longer.

It’s also encouraging because I know what he looks for in a company. Here’s how he explains it:

I really like studying businesses. I like trying to understand what’s happening in the world, and I like placing infrequent bets, investing in infrequent ideas.

We’re trying to answer six questions. Is this a business we understand? Is it a good business in the way that I just described? Is it run by a management team that thinks like shareholders, that will treat us like partners? Is it cheap, demonstrably relative to its expected cash flows? Is it trading in an attractive valuation with an attractive IRR, internal rate of return of owning it from here? Why is it cheap? Okay, can we identify the reason why we are right and the market is wrong? What’s the variant perception?

While Lawrences purchase of NRP is encouraging, we clearly own the company entirely backed up by our own research. That said, I’m glad to be a co-owner with the likes of Bryan Lawrence. If you’re curious how we would answer each of Lawrence’s six questions, check out our other pieces on Natural Resource Partners.

On a closing note, as the chart below shows, met coal prices have fallen slightly over the past month or so and NRP’s price dropped a bit. I couldn’t be happier.

Conclusion

With that, we’ve wrapped up this latest edition of Special Situation Investing. As always, thank you for tuning in and reading. We hope our feeble attempts at learning and sharing are useful in your own investing journeys. We’ll see you all again in two weeks with yet another write-up.

Share this post