Oil Ain't Toast

Macro look at global energy consumption as it pertains to oil and gas producers

Welcome to Episode 31 of Special Situation Investing.

Back in episode sixteen and again in our latest episode, we discussed Texas Pacific Land Corporation (TPL). In those episodes we explained TPL’s business model and how it forms a strong moat around the company, and also laid out arguments for why TPL is a major holding within our portfolios.

If you haven’t listened to those episodes, I highly recommend you do.

But, one unavoidable fact about TPL is that the bulk of its revenue is derived from oil and gas royalties that it collects off of its acres in western Texas. Given our culture’s trend toward renewable energy and the current distain for anything oil, gas, or hydrocarbon-related, one might wonder how we can have so much confidence in a company within a supposedly declining sector. Every day, headlines remind us that although oil built the past, renewables will build the future.

Well for one, as discussed in our last episode, TPL does much more than simply rake in millions from oil and gas royalties. It has a very profitable business selling water to oil operators. It also receives payments for roads, pipelines, solar and wind farms, and other infrastructure built on its property. And most recently, it is exploring ventures within the crypto and carbon sequestration sectors. But in addition to all that, we have a far less gloomy view on the future of oil and gas than our mainstream media friends. We believe the data predicts a healthy demand for oil and gas for many decades into the future. Today’s episode is about some of our observations on the long-term, macro prospects of oil and gas that support our bullish thesis on TPL.

Let’s begin by jumping into the macro data by considering global energy consumption. (And by the way, in this podcast I will be referencing multiple graphs. If you’d like to view the data yourself, or follow links to their sources, you can do so by visiting our substack page where we have begun to post the transcripts to our episodes. The link is: specialsituationinvesting@substack.com Alright, back to our first data point, global energy consumption.

Ourworldindata.org has some amazing interactive graphs on a host of economic topics. One of their charts, depicts total global energy consumption from the year 1800 all the way up to 2019. The graph shows how humanity transitioned from primarily relying on traditional biomass, i.e. wood and animal dung, to now using coal, oil, gas, nuclear, hydropower, wind, solar, other renewables and modern biofuels. What’s interesting is, even though we tapped into newer and better sources of fuel over the centuries, we still use more traditional biomass globally today than we did back in 1800. The same goes for coal and every other fuel source as well. In fact that’s the trend: even as humanity taps into new sources of fuel, the demand for older fuel sources generally remains constant or continues growing.

So those who argue that renewable energy sources will replace hydrocarbon fuels, instead of being used in conjunction with, are arguing contrary to the multi-century trend. It could happen, anything could happen. But it would require a break in a very long historical trend.

This trend makes sense in light of, and is closely related to, humanity’s population growth. As the population has grown, more energy has been required. Or seen another way, you could say that humans tapping into more diverse and more efficient sources of energy has allowed the population to grow. More energy made it possible for the globe to support more people.

Okay, so even as vast resources are invested into renewable energy, this historical trend could lead us to conclude that the amount of oil and gas used globally can be expected to increase, not decrease. And you don’t have to take my or history’s word for it. In its Annual Energy Outlook for 2022, the U.S. Energy Information Administration states this: “petroleum and natural gas remain the most-consumed sources of energy in the United States through 2050, [and they add on] but renewable energy is the fastest growing.” Further, a graph in that same report shows that not only do oil and gas remain the most consumed sources of energy, but the total amount used in the US continues to rise through 2050. Their chart shows an increase from approximately 37 to 40 quadrillion BTUs for oil and a rise from 32 to 35 quadrillion BTUs for natural gas.

Consuming more oil and gas is a trend unlikely to be limited to the US, but instead a global phenomenon. And most dramatic in developing countries. Our World In Data provides another fascinating chart that tracks access to clean fuels for cooking in countries around the world. (Clean cooking fuels being natural gas, ethanol, and electricity technologies as opposed to unclean cooking fuels such as wood, animal dung, and other biomass.) Their data spans the years 2000 through 2016, and over that time period the trend is clear: countries are transitioning to clean cooking fuels.

The chart tracks dozens of countries, but I highlighted three in my screenshot shown below; the US, China, and India. While 100% of the US population had access to clean cooking fuel for the entire period, that’s not the case for the majority for the world. India and China are two examples. Important examples though because, together, the two countries contain approximately 40% of the world’s population. The percentage of China’s population with access to clean cooking fuel increased from approximately 48% to 60%, and in India the increase was from approximately 22% to 42%.

This trend illustrates how many countries are maturing from less developed to more developed, and as they do so, are transitioning from biomass to cleaner, more efficient fuels. This means that the percentage of the global population using these fuels, particularly natural gas, is likely to continue to rise even as more developed countries have turned their focus to renewable energy sources.

But even in developed countries such as the US and Europe, our base case is that the transition to renewable energy sources will take longer, and prove less of a panacea, than its current hype suggests. This is for a litany of reasons. One is the lack of investment into mining the metals and materials that are required for solar panels and wind turbines over the last decade. This could make those materials prohibitively expensive.

Another reason is that hydrocarbons are actually required at nearly every stage of producing, maintaining, and disposing of, renewable energy infrastructure.

A third reason, and one of the most interesting, is that in seeking to transition economies from fossil fuels to renewable energy sources, countries are fighting against that multi-century long trend we mentioned at the beginning of this podcast in yet another way.

In addition to showing us that humanity continues using the same amount or more of every fuel source it taps into, the global energy consumption graph shows humanity has always developed and transitioned to using more energy-dense fuel sources. More energy dense simply means you get more bang for your buck. Coal, for example, is more energy dense than traditional biomass. Oil and natural gas are more energy dense than coal. And so on, you get the point. That trend is broken with renewable energy. In particular, with energy from wind turbines and solar panels, you get less bang for your buck.

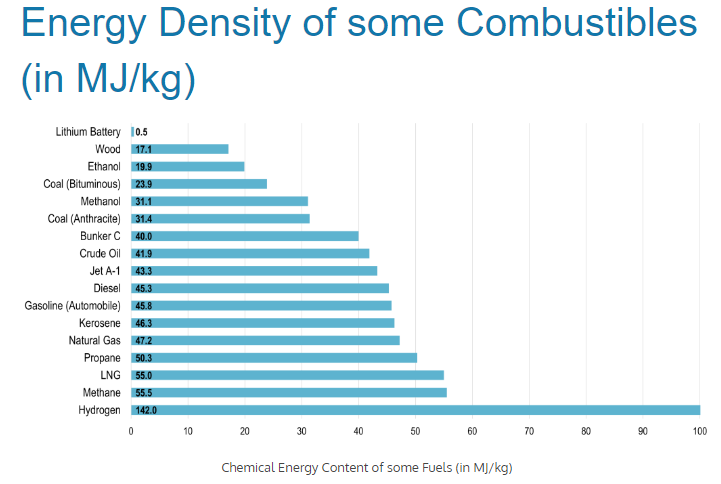

This trend and fact is supported by a chart provided by transportgeography.org. It depicts the energy density of a list of common combustibles including a wood, coal, crude oil, natural gas, and hydrogen. The density is listed in megajoules per kg, which for most of us means…nothing. So, I scoured the internet in order to make mega joules pet kilogram relatable for an average dude like me.

I found that one mega joule is approximately the energy it takes to run a large TV for one hour. I was once again reminded that one kg is roughly equal to two pounds. And I also learned that the average episode of the infamous television series, The Office, was 30 minutes long. With some fancy math that I dusted of from my high school days, I came up with the rough estimate that this chart is actually telling us how many episodes of The Office we can watch given one pound of each energy source. Your welcome.

Now that it’s relatable, what does the chart tell us? Well, with one unit of wood you could watch 17 episodes of Michael and his friends. Next, with one unit of coal, you could watch 31 episodes. That’s better. With crude oil it jumps up to 42 episodes and natural gas gives you 47. Pretty good, definitely beats wood’s 17 episodes. This comparison illustrates how over human history there’s been a progression from each primary fuel source to one that’s more energy dense. This has allowed humans to work and live more efficiently, driving up standards of living across the globe.

Now where does renewable energy place on this chart? The only renewable energy related fuel source the chart lists is a lithium battery. Clearly lithium batteries are not the only aspect to renewables, so although its not a perfect comparison, the sheer magnitude of the difference gets the point across. With one comparable unit of a lithium battery you could watch half of an episode of The Office. You probably wouldn’t even be able to get to the good part of the show.

This reduction in energy density will force humanity to make trade offs.

Exxon Mobile’s website front page states that one of the three drivers of energy demand is consumer preferences. So far, many citizens and policy leaders of developed countries are supportive of renewable sources. But the verdict is still out on how those preferences may change if standards of living are negatively affected. Perhaps Europe will be the vanguard on this issue as it doubles down on it’s renewable energy goals.

To wrap it up, these are just a few big picture reasons we believe that, like it or not, the world is going to want and need a lot more oil and gas than many people are projecting. If oil and gas demand increases, stays constant, or even slightly declines, we believe TPL is well positioned to capitalize on the energy trends of the future.

Well, that concludes Episode 31 of Special Situation Investing, we hope you enjoyed it and found at least some part of it insightful. We look forward to bringing you another episode next week.